Jens Nordvig, one of the hottest prognosticators in finance, will sell anyone his secret sauce for winning trades for $30,000 a year.

But if you want unfettered access to his best ideas and personal touch—the kind that the deep-pocketed hedge funds covet—be prepared to shell out about 20 times more.

That two-pronged approach to research, off-limits (at least officially) at Wall Street banks, captures one of the most striking shifts in finance today: the rise of a class system where entire businesses cater to only the highest-paying clients. Of course, haves and have-nots have long existed in the world of finance. But the widening gap within Wall Street itself, between what the privileged few and most others get, is creating a new financial elite—what amounts to the 1 percent of the 1 percent.

And if you’re not part of the 0.01 percent, the next best thing is to sell to it.

“Investors either get personalized advice from someone they really trust, or it’s the data tools, good robots—and the price of those two things are different,” the 42-year-old Dane explained from his WeWork office in Manhattan’s Flatiron district one recent afternoon.

For Nordvig, who left Nomura Holdings Inc. in January after five years as Wall Street’s top-ranked currency strategist, it meant leveraging that standing to build his firm, Exante Data, around a rarefied group of the brightest hedge-fund names— and the money they dole out.

Exante counts Key Square, founded by George Soros protege Scott Bessent, and Adam Levinson’s Graticule, a Singapore-based firm spun out of Fortress Investment Group, among its clients, according to conversations with investors and people familiar with the matter. Graticule didn’t reply to requests for comment.

Nordvig declined to identify specific firms, but says there are just “five to seven” large institutions, whose fees covered most of his startup costs. And by design, he isn’t accepting any new business. That’s because while Exante’s six employees are focused on its analytics rollout, Nordvig devotes the majority of his time advising his marquee customers.

He’s in touch with them on an almost daily basis and is just a phone call or instant message away—any time, 24/7. His research is tailor-made to suit each one’s needs and Nordvig says he’ll often spend hours at a time with a single firm debating macroeconomic policy and trade strategies.

In late July, Nordvig was up until midnight defending his high-stakes call to a hedge-fund client in Asia that the Bank of Japan would stand pat, rather than announce a new set of aggressive stimulus measures as everyone expected. (He dissuaded the firm from shorting the yen, which proved to be prescient as the Japanese currency surged following the non-event.)

“At banks, it’s mass production. It’s Target versus Hermès.”

So far, his backers like what they see.

“Jens is one of the great thinkers in the market,” said Key Square’s Bessent, who oversaw Soros’ personal fortune before starting his own billion-dollar macro fund this year. “Part of what we did was we got him to control his number of clients. At banks, it’s mass production. It’s Target versus Hermès.”

Nordvig isn’t shy about what he brings to the table. Prior to his years at Nomura, he spent almost a decade at Goldman Sachs Group Inc., where he rose to become co-head of global currency research and made his name with bold calls and savvy analysis. In between, he did a brief stint at Ray Dalio’s Bridgewater Associates. And Nordvig brushes off the perception among both admirers and critics that he can, at times, be just a bit too brazen in promoting himself. To him, it’s just part of the cutthroat nature of finance.

“I have a track record of being quite detail-oriented, precise in my analysis and also able to develop new frameworks for thinking about things, and at the same time being quite pragmatic,” he said. “I’ve set up the advisory business so that the people I deal with are some of the biggest macro investors in the world, and I know their interests fit with how I think.”

Whatever the case, there is little doubt the appetite for bespoke research like Nordvig’s is growing. Banks are slashing costs, cutting jobs and abandoning their ambitions to be all things to all customers in the face of a slew of regulations over issues like selective access and excessive risk-taking. An industry-wide slump in revenue since the financial crisis has also prompted bank executives to rethink the value of the commission-based model, where investment research is offered for free in return for trade orders.

Many firms have eliminated analysts as they scale back research spending—making personalized service and attention all the more valuable. Some like Citigroup Inc. and Morgan Stanley have drawn up preferred client lists with code names such as “Focus Five” and “supercore” for top clients.

“It’s a changing landscape,” said Matthew Feldmann, a consultant at Scepter Partners, a multi-family office, and a former money manager at Citadel and Brevan Howard. “People like Jens have found a niche area where all you need is a few wealthy individual customers.”

Perhaps just as important is the proliferation of automated trading strategies and machine-driven data mining, which has replaced many traditional roles that used to exist on Wall Street (not to mention made it harder for hedge funds to outperform as technology makes financial data almost ubiquitous).

Nordvig’s old job at Goldman Sachs exemplified that bygone era. As recently as 2007, he’d stand in the middle of the trading floor with mic in hand on the first Friday of every month, just before the 8:30 a.m. payrolls report. His task? Shout out his immediate take. If the U.S. added more jobs than expected, he’d cry “buy dollar-yen!” and within seconds, Goldman Sachs’s traders would hit the button on their keyboards to put in the order.

“We used to be able to make so much money by just being fast,” he said. Yet today, it’s all done by robots.

Amid the upheaval, Nordvig is confident his experience and smarts will ensure his high-priced advice remains in demand. But he’s not taking any chances.

After years of lackluster returns and faced with the biggest withdrawals since the financial crisis, hedge funds are looking for any edge they can find. These days, that often comes from the world of quantitative analysis. Even legendary names like Paul Tudor Jones, who made their fortunes the old-fashioned way, are hiring a bevy of programmers and mathematicians to build out more sophisticated, computer-driven strategies.

But not everybody has the research budgets to hire scores of Ph.D.s or pay for Nordvig’s white-glove service. That’s where the “data” in Exante Data comes in (Exante is derived from “ex ante,” Latin for “before the event”). Plenty of research superstars have decamped from Wall Street to set up boutique advisory firms, but Exante’s two-tier model is rare. Once the data business is fully up and running, Nordvig promises to give mere mortals on Wall Street the same type of data-mining tools once available only to the biggest quant shops.

Nordvig says he has one overriding advantage: he simply understands markets better.

Yet competition on the data front is heating up. Scores of startups are already scraping data and turning the information into actionable ideas. Goldman Sachs is the biggest investor in Kensho Technologies Inc., which analyzes historical trading patterns to predict how assets react to events like policy meetings and economic releases. An outfit called SpaceKnow Inc. uses satellite images of factories to gauge economic activity in export-oriented countries like China.

Nordvig, in his typical cocksure manner, says he has one overriding advantage: he simply understands markets better.

In coming months, Exante will launch its first data product for the masses. According to Nordvig, his data scientists have come up with a complex algorithm that precisely estimates how much the yuan exchange rate is influenced by China’s buying or selling of dollars, on a daily basis.

There’s nothing publicly available that comes close to measuring intervention in such detail. But Nordvig says his algo succeeds because it can capture anomalies in yuan trading, like a sudden widening in bid-ask spreads, and then compare the data against freely-traded markets in big financial centers.

While the tool can’t yet gauge intervention in offshore yuan and currency forwards, his backtested results show it closely tracks less frequently released official figures. And knowing beforehand can make a huge difference. Case in point: In August 2015, the People’s Bank of China unexpectedly engineered a weakening of the yuan, which blindsided investors and sent financial markets worldwide into a tailspin.

“This is about knowing what topics are important to the clients you serve,” Nordvig said.

http://www.bloomberg.com/news/features/2016-09-15/wall-street-s-0-01-the-guru-who-only-talks-to-hedge-fund-elite

Thursday, September 15, 2016

Wednesday, September 14, 2016

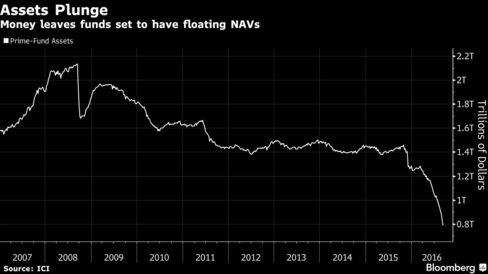

There’s a $300 Billion Exodus From Money Markets Ahead

With a seismic overhaul of the $2.6 trillion money-market industry weeks away from kicking in, money managers are bracing for a last-minute exodus of as much as $300 billion from funds in regulators’ cross hairs.

Prime funds, which seek higher yields by buying securities like commercial paper, are at the center of the upheaval. Their assets have already plunged by almost $700 billion since the start of 2015, to $789 billion, Investment Company Institute data show. The outflow has rippled across financial markets, shattering demand for banks’ and other companies’ short-term debt and raising their funding costs.

The transformation of the money-fund industry, where investors turn to park cash, is a result of regulators’ efforts to make the financial system safer in the aftermath of the credit crisis. The key date is Oct. 14, when rules take effect mandating that institutional prime and tax-exempt funds end an over-30-year tradition of fixing shares at $1. Funds that hold only government debt will be able to maintain that level. Companies such as Federated Investors Inc. and Fidelity Investments, which have already reduced or altered prime offerings, are preparing in case investors yank more money as the new era approaches.

“All managers, like ourselves, are positioning around the uncertainty of the exact magnitude of the outflows,” said Peter Yi, director of short-term fixed income at Chicago-based Northern Trust Corp., which manages $906 billion.

$300 Billion

While Yi sees the additional outflow from prime-fund investors potentially reaching $200 billion in the next 30 days, TD Securities predicted in a Sept. 7 note that it may tally as much as $300 billion.

Yi is preparing by shortening his funds’ weighted average maturity and avoiding short-term debt that matures beyond September. He’s not alone. For the biggest institutional prime funds tracked by Crane Data LLC, the weighted average maturity of holdings fell to an unprecedented 10 days as of Sept. 12. It’s not just floating net-asset values that investors are avoiding. Prime funds can also impose restrictions such as redemption fees.

Amid the tumult, money-fund assets have held steady because most of the cash leaving prime and tax-exempt funds has streamed into less risky offerings focusing on Treasuries and other government-related debt, such as agency securities and repurchase agreements. These funds are exempt from the new rules, which the U.S. Securities and Exchange Commission issued in 2014.

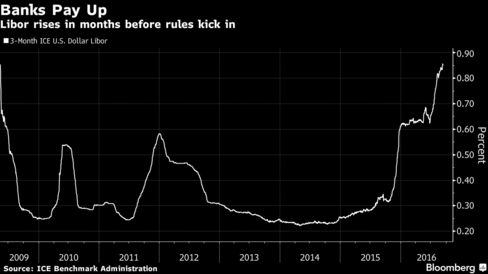

A major repercussion of the flight from prime funds is that there’s less money flowing into commercial paper and certificates of deposit, which banks depend on for funding. As a result, banks’ unsecured lending rates, such as the dollar London interbank offered rate, have soared. Three-month Libor was about 0.85 percent Wednesday, close to the highest since 2009.

Libor may stabilize after mid-October because prime funds may begin to increase purchases of bank IOUs, although the risk of a Federal Reserve interest-rate hike by year-end will keep it elevated, said Seth Roman, who helps oversee five funds with a combined $3.2 billion at Pioneer Investments in Boston.

“You could picture a scenario where Libor ticks down a bit,” Roman said. But “you have to keep in mind that the Fed is in play still.”

Financial firms paying higher rates to attract investors to their IOUs will push three-month Libor to about 0.95 percent by the end of September, according to JPMorgan Chase & Co.

Although bank funding costs are rising, it isn’t a signal of financial strain as in 2008, said Jerome Schneider, head of short-term portfolio management at Newport Beach, California-based Pacific Investment Management Co., which oversees about $1.5 trillion.

“This is not a credit stress event, it’s a credit repricing due to systemic and structural changes,” he said.

The market for commercial paper has shrunk about 50 percent from its $2.2 trillion peak in 2007, pushing financial firms to diversify funding sources -- choosing longer-term debt and loans in foreign currencies.

At least $269 billion in commercial paper and certificates of deposits held by prime funds will come due before Oct. 14 and most issuers of that debt will need to find financing outside the money-fund industry, JPMorgan predicts.

The hubbub in money markets has its roots in a crucial episode of the financial crisis -- the demise of the $62.5 billion Reserve Fund, which became just the second money fund to lose money, or “break the buck.” The event contributed to the global freeze in credit markets and pushed the Treasury Department to temporarily backstop almost all U.S. money funds.

With the Fed’s target rate still not far from zero, money-fund investors looking to pad returns may overcome their aversion to prime funds. Institutional prime funds’ seven-day yield was 0.24 percent as of Sept. 12, compared with 0.17 percent for government funds, according to Crane Data.

“You’ll see the prime-fund space continue to shrink until we hit mid-October,” said Tracy Hopkins, chief operating officer in New York at BNY Mellon Cash Investment Strategies, a division of Dreyfus Corp.

“After that,” she said, “I would not be surprised to see assets return, once customers get accustomed to the floating NAVs and want to earn incremental yield over government money-market funds.”

EES: Splitting Pennies One Day Sale

Today only, get Splitting Pennies on Kindle for .99 on Amazon!

Click here to get Splitting Pennies for .99 while it lasts

Click here to get Splitting Pennies for .99 while it lasts

- Gift it to a friend

- Gift it to your employees who need to learn about Forex

- Buy it for your family

All you need is their email - you can send it to anyone with an Amazon account. No Kindle needed! It's free to sign up for an Amazon account if they don't have.

What is Splitting Pennies all about?

Splitting Pennies - Understanding Forex is a book about our global financial system and its direct impact on every human being on this planet Earth. Every day, our money is worth less and less. Splitting Pennies explores why, through the prism of its mechanism; Forex. Forex is the largest business in the world and the least understood. This is not taught in school - start your journey, and just read. Splitting Pennies displays practical examples of how many have profited in Forex, the history of Forex, and practical examples of strategies to use for your portfolio. Readers of the book will know more than a Harvard MBA about Forex, and can consider themselves Sophisticated Forex Investors (SFI). Complex topics such as currency swaps are broken down in digestible form, for the average investor or for financial professionals. Splitting Pennies is a must read for those in investment banking, securities, fund management, accounting, banking & finance, and related fields. But it’s written for the layman, the worker, the average investor – the student in us.

Monday, September 12, 2016

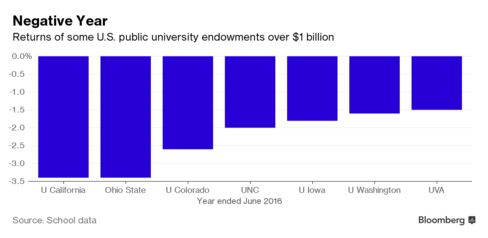

Seven College Endowments Report Annual Losses in Choppy Markets

Seven public U.S. university endowments with assets of more than $1 billion including the University of California reported fiscal 2016 investment losses as lackluster economic growth and volatility drubbed markets.

College endowments are poised to take the worst slide in performance since the 2009 recession. Funds with more than $500 million lost a median 0.73 percent in the year through June 30, according to the Wilshire Trust Universe Comparison Service. The Wilshire data, from fund custodians, excludes fees while most schools report returns net of fees.

“It was a bit of a bloodbath,” as swings in the markets challenged stock pickers, Jagdeep Bachher, chief investment officer at the University of California system, said at an investment committee meeting on Sept. 9, according to a webcast of the meeting. “Last year was a bad year for active managers all around.”

Ohio State University and California had the largest declines through June 30 among the seven at 3.4 percent each while the University of Virginia fell 1.5 percent. It’s shaping up to be the worst year for endowment returns since 2009, when the richest schools had a loss of 21.8 percent, according to the Wilshire service. For fiscal 2016, a benchmark 60/40 portfolio of the Wilshire 5000 Total Stock Market Index for U.S. equities and the Wilshire Bond Index returned 4.5 percent.

Hedge Funds

The value of the University of California’s endowment rose 2.2 percent to $9.1 billion from the prior year due to inflows from shifting cash from short-term funds to the endowment and royalty payments, Bachher said. The investment losses were driven by poor returns from public equity fund managers and hedge funds, he said.

Market volatility was due to “central bank actions, slow-to-no growth worldwide, the oversupply of oil on a worldwide basis resulting in prices collapsing and the unexpected Brexit vote,” John Lane, chief investment officer at Ohio State’s endowment, said in an e-mail.

Virginia’s best-performing strategies -- private real estate and domestic buyouts -- couldn’t offset losses in its public and growth equity sectors and its resources portfolio, the school said. The fiscal 2016 investment loss follows gains of 7.7 percent and 19 percent in the previous two years, showing how even the best-performing funds are saddled with a new reality of low returns.

The University of Virginia Investment Management Co. is committed to its long-term philosophy, Lawrence Kochard, the chief investment officer, wrote in a report.

‘Significant’ Impact

“We expect a wide variety of investment challenges going forward and believe macro-level factors will continue to have a significant impact on markets,” Kochard wrote.

Kochard said the school is finding “pockets of opportunity” in areas such as non-U.S. equities.

“We also continue to observe an investment community fixated on global macro risks -- including a slowing Chinese economy, the implications of Brexit, the U.S. presidential election and central bank policies -- which provides a good environment in which our global public managers can identify mispriced securities,” Kochard wrote.

The fund has made changes to its asset allocation over time, according to the report. Public equities were increased in fiscal 2016 to 24.6 percent from 20.5 percent in 2012; and marketable alternatives and credit went to 14 percent from 9.3 percent. The management company decreased its allocation to resources to 4.5 percent from 7 percent, and real estate to 6.6 percent from 8.6 percent.

Despite the investment loss, the value of the long-term pool increased to $7.6 billion from $7.5 billion because of contributions in excess of distributions and investment losses.

Global Equities

Ohio State’s biggest loss came from its global equities portfolio. The state’s flagship public school’s 7.2 percent loss in the allocation dragged down a 10.8 percent gain in real assets, according to the school.

The University of Washington’s fund lost 1.6 percent. The drop was led by declines in its “capital appreciation” bucket, which includes a 20 percent asset allocation to emerging markets equity; 38 percent in stocks of developed markets; and 12 percent in private equity, according to the school.

The University of North Carolina at Chapel Hill’s endowment posted a 2 percent decline. The University of Iowa endowment’s investments fell 1.8 percent in fiscal 2016, with global equities leading the decline. The investment loss reflects the portion of the endowment managed by the foundation.

The University of Colorado’s investment fund, which is managed by Perella Weinberg Partners, lost 2.6 percent, according to the school. The value declined to $1.06 billion from $1.09 billion a year ago. About 43 percent of the fund’s holdings are in private capital, real assets and hedge funds, with 6 percent in cash and fixed income, according to a report.

While the annual returns were hurt by Brexit at the end of June, the fund was up almost 3 percent in July, Mike Pritchard, vice president and chief financial officer of the University of Colorado Foundation, said in an interview.

“This is a time for all universities to consider what does the future look like,” Pritchard said. “Endowments are long term. You want to meet the short-term needs -- scholarships, professorship chairs -- and you also want to sustain the long-term spending power. That’s the balance were all looking at right now.”

http://www.bloomberg.com/news/articles/2016-09-12/seven-college-endowments-report-annual-losses-in-choppy-markets

TRADE FOREX - RECOVER YOUR LOSSES FROM STOCKS

Friday, September 9, 2016

Wells Fargo Fires 5,300 For Engaging In Massive Fraud, Creating Over 2 Million Fake Accounts

For years we have wondered why Wells Fargo, America's largest mortgage lender, is also Warren Buffett's favorite bank. Now we know why.

On Thursday, Wells Fargo was fined $185 million, (including a $100 million penalty from the Consumer Financial Protection Bureau, the largest penalty the agency has ever issued) for engaging in pervasive fraud over the years which included opening credit cards secretly without a customer’s consent, creating fake email accounts to sign up customers for online banking services, and forcing customers to accumulate late fees on accounts they never even knew they had. Regulators said such illegal sales practices had been going on since at least 2011.

In all, Wells opened 1.5 million bank accounts and "applied" for 565,000 credit cards that were not authorized by their customers.

Wells Fargo told to CNN that it had fired 5,300 employees related to the shady behavior over the last few years. The firings represent about 1% of its workforce and took place over several years. The fired workers went to far as to create phony PIN numbers and fake email addresses to enroll customers in online banking services, the CFPB said.

How Wells perpetrated fraud is that its employees moved funds from customers' existing accounts into newly-created accounts without their knowledge or consent, regulators say. The CFPB described this practice as "widespread" and led to customers being charged for insufficient funds or overdraft fees, because the money was not in their original accounts. Additionally, Wells Fargo employees also submitted applications for 565,443 credit card accounts without their knowledge or consent, the CFPB said the analysis found. Many customers who had unauthorized credit cards opened in their names were hit by annual fees, interest charges and other fees.

According to the NYT, regulators said the bank’s employees had been motivated to open the unauthorized accounts by compensation policies that rewarded them for drumming up new business. Many current and former Wells employees told regulators they had felt extreme pressure to expand the number of new accounts at the bank.

And, since it is US government policy never to send a banker to prison, they thought that engaging in criminal behavior was not such a bad idea.

Federal banking regulators said the practices reflected serious flaws in the internal culture and oversight at Wells Fargo, one of the nation’s largest banks.

"Today's action should serve notice to the entire industry that financial incentive programs, if not monitored carefully, carry serious risks that can have serious legal consequences," said CFPB Director Richard Cordray. He added that “unchecked incentives can lead to serious consumer harm, and that is what happened here."

"Consumers must be able to trust their banks. They should never be taken advantage of," said Mike Feuer, the Los Angeles City Attorney who joined the settlement.

On its behalf Wells fargo issued a statement saying it “is committed to putting our customers’ interests first 100 percent of the time, and we regret and take responsibility for any instances where customers may have received a product that they did not request,” the bank said in a statement adding that "at Wells Fargo, when we make mistakes, we are open about it, we take responsibility, and we take action."

As the NYT puts it, "this is an ugly moment for Wells Fargo, one of the few large American banks that have managed to produce consistent profit increases since the financial crisis." Now we know one of the reasons why.

As CNN redundantly adds, "the scope of the scandal is shocking."

And since nobody will go to prison, in a few months we will read another such "shocking scandal" perpetrated by another bailed-out bank.

Wednesday, September 7, 2016

EES: Warning to investors - Do Not Invest In Currencies

We see from time to time articles from investment groups talking about how they believe that the US Dollar will be strong for the next 18 months blah blah blah. It's always positive to hear investment managers learning about FX. Unfortunately, as we explain in Splitting Pennies - FX isn't like other markets. Investing in Currencies is an outright gamble. Let's elaborate on this point, the difference between TRADING and INVESTING.

When someone says that the US Dollar will be 'up' in the next 6 months - how do they know there won't be a black swan event, such as an act of terror, a surprise interest rate increase, a coup, or any number of other events that can shake markets?

The proof, or at least a strong argument - Goldman Sachs has lost billions for clients in FX, see this recent example:

Goldman's Robin Brooks has to be a sadist: that is the only way we can explain his ability to crush the greatest number of Goldman clients at every possible opportunity.

Well, if Goldman can't do it - you really think you are smarter than Goldman Sachs? And remember that Forex is a Monopoly, in which Goldman Sachs is a controller. They lose money in a market they 'control.'

Why would an FX outfit warn investors not to invest in Currencies? Because we believe based on statistical evidence that the markets are random. Or to be more static - even if they aren't random, if a strategy can work on random numbers, it can work on any market.

There is however a very profitable way to trade Forex and include it in your portfolio. The solution is - to trade Forex using proven and tested algorithms.

Anything else, is pure investment suicide.

And the benefit to investing in Forex strategies, it is an asset class per se. In fact, investing in a strategy isn't an investment in currencies. Although, most FX strategies will not work on stocks, bonds, commodities, and other instruments. That doesn't mean the strategies are correlated to FX price activity - they're not. Simply, it's possible to create mathematically sound strategies in FX that's not possible in other markets. This is due to a number of reasons but most notably, FX has superior size and liquidity, relatively low volatility, higher activity (tick movement), and a plethora of development tools for strategists.

Unless you're George Soros, trading and investing in FX without the aid of computer models is highly risky! For this reason, hundreds of FX managers across the globe have invested their own funds in the research and development of strategies, mostly algorithmic but almost all quantitative. Here's one just as an example, that didn't have a losing month in 3.5 years. But it is expensive to have such results, it requires massive computing power, and constant optimization.

If you want a quick Forex education, checkout Splitting Pennies - the pocket guide designed to instantly make you a Forex genius!

If you want to get started looking at investing, checkout Fortress Capital Forex

Thursday, September 1, 2016

EES: Half of Corporate America losing BILLIONS in Forex for no reason

Here's the big irony for the markets. As we explain in Splitting Pennies book, Forex is the largest market in the world and the least understood. Corporate America certainly doesn't understand Forex. Well, according to this report, about 50% do:

Forty-eight percent of nonfinancial companies listed on U.S. stock exchanges remained exposed to volatility in foreign exchange rates, commodity prices and interest rates in 2012 because they did not hedge them, according to a new study by Chatham Financial. The interest-rate and currency risk adviser studied a sample of 1,075 companies ranging from $500 million to $20 billion in revenue. The nearly half that did not use financial instruments to hedge their exposures demurred despite the threat the risks posed to both the balance sheets and reported earnings (see chart at bottom). “That was surprising, knowing the pressure senior management teams and treasury feel around identifying ways to reduce risk to factors within their control so business can focus on other areas,”Amol Dhargalkar, managing director for corporate advisory at Chatham, says.

Companies that do business outside of the USA have substantial forex exposure. This exposure can be an asset, if properly managed - but often it is a liability. Recently, the trend in corporate accounting has been to blame "currency headwinds" which can be a good excuse for up to $10 billion in losses. Did these executives ever hear about hedging?

So what does this data mean? It means that half of Corporate America is speculating BIG in Forex. Not hedging, when you have FX positions, is speculating. For example, imagine you're a big US multinational like McDonalds (MCD). McDonalds (MCD) is a great example because they are one of the companies that lives off their FX hedges. Without FX hedging, it's questionable if MCD could survive, because more than 60% of their revenue comes from non-US Dollar (USD). That means their revenue, without FX hedging, would be nearly an exact function of the FX markets (which is the case for these companies that don't hedge). Companies that lose billions of dollars due to 'currency headwinds' - they are losing huge in Forex.

Here's the irony. Pension Funds and many institutions are reluctant to invest in Forex strategies because they are 'risky'. But they invest in the stock of companies that lose billions in Forex! And that's OK. Well, everyone is losing, so why not us too. Heck, I don't want to be singled out as the one state pension fund that's actually MAKING money for our retirees, that might cause me to get promoted, or lose my job.

Why don't these companies hedge you ask? Isn't it their fiduciary duty to their shareholders? Here's one perspective from PWC:

When a publicly held company engaged in a multi-billion dollar investment in an overseas location

recently, the firm considered using a hedge — or swap — contract to reduce the risk that a big currency

swing would impact costs and financial results. The plan was sound financially. Yet, management had

concerns about the reaction of investors to this approach and decided to drop the hedging plan, says

Chris Rhodes, accounting advisory services partner at PricewaterhouseCoopers (PwC). Why? Because the CFO determined that,

although the hedge would protect all the cash

spent in the foreign jurisdiction against currency

exposure, the cost of capital — in this case

borrowing in external markets — “would be

negatively impacted by the inability of some

analysts to understand the reporting issues

involved,” Rhodes explains. “The concern is that,

although many analysts would immediately grasp

the sophisticated currency-hedging procedures

that were key to the plan, others might not.”

So you see, according to this perspective, CFOs understand Forex, but they understand that others such as analysts don't understand, and think that there's a negative perception problem, to closing a big gaping hole in their FX exposure.

One year in the 90's, Intel Corporation made more money on their FX positions than they did selling processors. Not all of Corporate America is completely stupid. There are some savvy FX managers out there, that do a great job. But for the other half, one has to wonder if FX volatility will finally drive these unhedged companies out of business.

Here's what you see on every street corner in Russia:

At least, some humans are prepared for potential financial catastrophe, even if it's as simple as FX volatility.

To learn more about Forex Hedging, checkout Splitting Pennies - your pocket guide designed to make you an instant Forex Genius! Or checkout Fortress Capital Forex Hedging.

Wednesday, August 31, 2016

Deutsche Bank Refuses Delivery Of Physical Gold Upon Demand

While the trading world was focused on the latest news involving Deutsche Bank, namely that the troubled German bank had beencontemplating a merger with Germany's other mega-bank, Commerzbank as part of a strategy to sell all or part of a key business to speed up its flagging overhaul, a more troubling report emerged in a German gold analysis website, according to which Deutsche Bank was unable to satisfy a gold delivery request when asked to do so by a client of Germany's Xetra-Gold service.

But first, what is Xetra-Gold?

According to its website, the publicly traded company "provides investors with an efficient instrument to participate in the performance of the gold market. Xetra-Gold’s combination of features – cost-efficient trading and the right for physical delivery of gold - makes it an attractive product."

Among its highlights, Xetra-Gold lists the following:

Cost-efficient trading: No mark-up fee, no transportation or insurance costs such as those incurred when purchasing physical gold. Only the standard transaction fees that are charged for on-exchange securities trading are payable at the time of acquisition. The spreads that apply to purchase and sale correspond to the standard conditions on the global market and are considerably lower than those for traditional gold-based financial products. Furthermore, management or administration fees relating to Xetra-Gold are not incurred. The investor pays the amount of custody fees which he/she has agreed upon with the depository bank.Physically backed: The issuer uses the proceeds from the issue of Xetra-Gold to purchase gold. The physical gold is held in custody for the issuer in the Frankfurt vaults of Clearstream Banking AG, a wholly-owned subsidiary of Deutsche Börse AG. In order to facilitate the delivery of physical gold, the issuer holds a further limited amount of gold on an unallocated weight account with Umicore AG & Co. KG.Transparent: Xetra-Gold tracks the price of gold on a virtually 1:1 basis, and is always up to date.Tradeable in euros per gram: While in the past, gold was mainly denominated in US dollars per troy ounce, you trade Xetra-Gold in euros per gram.Stable/Constant holdings: The investor’s right to receive delivery of the certificated amount of gold is not reduced by management costs or other fees, unlike other investments in gold. 1,000 units of Xetra-Gold will still represent a kilogram of gold in 30 years' time.

The company makes the following promise:

Redemption for gold: Investors always have the possibility of demanding delivery of the securitised amount of gold per bearer note against the issuer. If the investor is not able to exercise this right due to legal restrictions effective for him/her, he/she can demand the cashing of Xetra-Gold from the issuer. In this case, a settlement fee of EUR 0.02 per Xetra-Gold bond will be charged.Delivery of gold: If an investor asserts his/her right to the delivery of the certificated volume of gold from the issuer, the gold will be transported to the respective point of delivery by Umicore AG & Co. KG, which is responsible for all physical delivery processes. The issuer will also have delivery rights of gold from Umicore AG & Co. KG, as the gold leaf debtor. Investors can find information on delivery and the alternative payment claims that are relevant for investment and insurance companies in the PDF document entitled 'Information on the process for exercising Xetra-Gold'.

And yes, Deutsche Bank is involved, as the fund's Designated Sponsor.

In other words, Xetra-Gold is an Exchange-Traded Commodity which differentiates itself by "representing that every gram of gold purchase electronically is backed by the same amount of physical gold" and its principal bank is none other than Deutsche Bank.

And with Germans recently rushing to buy safes or find sound money alternatives in a country where the interest rate is negative, the ETC, it is not surprising that the population has flocked to its offering.

According to recent report by LeapRate, the gold held in custody by Deutsche Borse Commodities for the purpose of physically backing the Xetra-Gold bond has risen to a new record high of 90.67 tons, an increase of more than 50% since the beginning of the year. "For each Xetra-Gold bond, exactly one gram of gold is deposited in the central vaults for German securities in Frankfurt" the report parrots the company's website.

Among all exchange-traded commodities (ETCs) tradable on Xetra, Xetra-Gold is by far the most successful in terms of turnover. During the first seven months of the year, order book turnover on Xetra stood at approximately €1.5 billion. The assets managed by Xetra-Gold currently amount to €3.5 billion.In September 2015, the German Federal Fiscal Court (Bundesfinanzhof) had ruled that after a minimum holding period, any profits from the sale or redemption of Xetra-Gold are not subject to the capital gains tax. From a fiscal point of view, the purchase, redemption or sale are thus to be treated equal to a direct purchase or sale of physical gold, such as in bullions or coins.

But what is most notable, is that, as noted above, Xetra-Gold investors are entitled to the delivery of the certified amount of physical gold at any time, and adds that "since the introduction of Xetra-Gold in 2007, investors have exercised this right 900 times, with a total of 4.5 tons of gold delivered."

However, something appears to have changed.

As Oliver Baron reports, those who ask for gold delivery at this moment, "could encounter difficulties." The reason is that according to Baron, a reader of GodmodeTrader "sought physical delivery of his holdings of Xetra-Gold. For this he approached, as instructed by the German Borse document, his principal bank, Deutsche Bank."

At that point then he encountered a big surprise: the Deutsche Bank account executive informed the investor that "the service", is no longer offered, namely exercising physical delivery at Xetra-Gold, for "reasons of business policy" and therefore the order form provided by Clearstream Banking AG for exercising Xetra-gold is no longer available.

Baron writes that since Deutsche Bank is no longer serving the physical exercising of delivery request of Xetra-Gold is remarkable, as Deutsche Bank is the "designated sponsor" as well as fiscal, principal and redemption agent of Xetra-Goldaccording to its prospectus, and as the explainer of how to exercise physical delivery also reveals. Even if one is a customer of another bank, Xetra-Gold should - at least on paper- guarantee delivery by way of Deutsche Bank, as the Deutsche Borse Commodities GmbH explains in its "process description for exercising units"

Step-by-step description of exerciseTogether with a representative of his principal bank, the investor creates the transaction and sends it to the principal bank's custodian with the relevant process data described above. The custodian in turn instructs its custodian, stipulating all process-relevant data, until a bank which is a customer of Clearstream Banking is authorised.The customer may use the attached exercise form to instruct the designated sponsor (here Deutsche Bank AG, Frankfurt) to deliver a specified number of gold bars to the point of delivery. The process is similar to that for the delivery of physical certificates.The customer should send the original exercise form to the following address:Deutsche Bank AG

"Ausübung Xetra-Gold" CIB-Global Banking

Trust & Securities Services

Grosse Gallusstrasse 10 – 14

60311 Frankfurt am Main

GermanyTo transfer the required amount of Xetra-Gold units to the blocked account of Deutsche Börse Commodities, the customer should also place an FoP instruction via CASCADE or File Transfer/SWIFT.Delivery will be initiated if Deutsche Bank receives the securities and the application form by 10:00 CET. As a rule it takes one to two weeks to deliver retail gold bars and four days for London Good Delivery gold bars from date of ordering. As soon as the delivered gold arrives at the point of delivery, the Xetra-Gold® units are removed and recovered from the "Ausübungskonto DBCo" (DBCo exercise account).Due to the provisions of the Money Laundering Act (Geldwäschegesetz) only the branch of a bank may be used as point of delivery. Investors expecting a large delivery of gold should contact their principal bank to discuss the transfer of the gold to the point of delivery.

The article goes on to note that it was not clear whether the exercise and physical delivery at other banks is actually still possible. Baron said that Deutsche Borse Commodities advised to transfer the Xetra-Gold shares in a cooperative/Raiffeisenbank since physical delivery is allegedly still possible here. The Deutsche Borse also announced that it is currently working on the "possibility of delivery regardless of bank branch." However, since this process was not described in the prospectus of Xetra-Gold, it would have to be legally tested, which could take considerable time.

The article's conclusion: anyone who wants to easily convert their Xetra-Gold holdings into physical gold - at least for clients of Deutsche Bank - can do so only by selling their shares, and then buying gold coins or bars directly elsewhere. Which leads the author to the logical question: what is the worth of the Xetra-Gold service, which certifies the right to redeem physical gold, if said delivery is no longer possible?

In other words, what was supposedly an ETC which promised physical delivery upon demand, is nothing more than yet another "paper only" play.

We, on the other hand, have a more focused question: is the inability to deliver physical gold an incipient issue with Xetra-Gold, or with the company's "designated sponor" Deutsche Bank, and if the latter is suddenly unable to satisfy even the smallest of delivery requests by retail clients, just how unprecedented is the global physical gold shortage?

Subscribe to:

Posts (Atom)