One of the most persistent myths in America today is that urban areas are innovative and rural areas are not. While it is overwhelmingly clear that innovation and creativity tend to cluster in a small number of cities and metropolitan areas, it’s a big mistake to think that they somehow skip over rural America.

A series of studies from Tim Wojan and his colleagues at the U.S. Department of Agriculture’s Economic Research Service documents the drivers of rural innovation. Their findings draw on a variety of data sets, including a large-scale survey that compares innovation in urban and rural areas called the Rural Establishment Innovation Survey (REIS). This is based on some 11,000 business establishments with at least five paid employees in tradable industries—that is, sectors that produce goods and services that are or could be traded internationally—in rural (or non-metro) and urban (metro) areas.

The survey divides businesses into three main groups. Roughly 30 percent of firms are substantive innovators, launching new products and services, making data-driven decisions, and creating intellectual property worth protecting; another 33 percent are nominal innovators who engage in more incremental improvement of their products and processes; and 38 percent show little or no evidence of innovation, so are considered to be non-innovators.

The first table below charts this breakdown for rural and urban areas. Establishments in urban areas are more innovative, but not by much. Roughly 20 percent of rural firms are substantive innovators, compared to 30 percent of firms in urban areas.

Photo by Data by Tim Wojan and Timothy Parker. Graphic by Madison McVeigh/CityLab

In fact, the urban-rural divide in innovation may be more a product of the relative size of firms than of geography. The next chart shows this: Rural areas actually have a slightly overall higher rate of substantive innovation for large firms (those with 100 employees or more), while urban areas win out in their rate of substantive innovation by small and medium-size firms.

Rural areas also have a slight advantage over their metro counterparts in the rate of substantive innovation by the most innovative firms (those that are patent-intensive). That’s because innovation in rural areas tends to be a product of patent-intensive manufacturing in industries like chemicals, electronics, and automotive or medical equipment, while urban areas have higher rates of innovation in services.

Photo by Data by Tim Wojan and Timothy Parker Graphic by Madison McVeigh/CityLab

Of course, innovation concentrates and clusters in certain rural areas, just as it does in cities and metros. In a 2007 study, Wojan and his collaborators identified 100 or so rural creative havens, such as Woodstock, New York, and the area around Telluride and Silverton, Colorado. These rural creative centers tend to be in relatively close proximity to and have good connections to major metro areas; are home to a major university or college; or have considerable natural amenities which draw people to them.

Whereas arts districts in urban areas are typically in high-density, mixed-use neighborhoods with lots of foot traffic, rural artistic districts tend to crop up around natural, physical, and recreational amenities. According to a 2017 study by the National Endowment for the Arts (NEA), the likelihood that a rural county will contain a performing arts organization is nearly 60 percent higher if the county overlaps with a forest or national park.

The most notable difference between the rural and urban arts districts is the distance one must travel: Rural arts organizations reported that 31 percent of their visitors travel “beyond a reasonable distance” to visit, compared to 19 percent in urban areas.

Photo by Data from NEA. Graphic by Madison McVeigh/CityLab

If anything, the arts may be even more important to rural innovation than they are to urban innovation. While my own research has drawn a connection between the arts and clusters of innovative high-tech startups in urban areas, Wojan and his colleague Bonnie Nichols’ data suggests an even stronger connection between arts and innovation in rural areas. And according to the NEA paper, probability that a rural firm will be a substantive innovator rises from 60 percent in rural counties with no performing arts organizations to nearly 70 percent for those that host two or three, to as high as 85 percent if a rural county hosts four or more.

Furthermore, the share of firms that are highly innovative rises sharply alongside performing arts organizations in rural areas. The probability that a rural business will be highly innovative increases from 17 percent to 44 percent as the number of performing arts organizations in a rural county increases from zero to one. When that number rises to two, the probability that a business will be highly innovative grows to 70 percent or higher.

Photo by Data from NEA. Graphic by Madison McVeigh/CityLab

Ultimately, Wojan and company’s analysis find a strong statistical association between the arts, innovation, and economic dynamism in rural areas. And this leads them to conclude that the arts are a direct force in rural innovation, not just an indirect factor that helps to attract and retain talent.

Artists and creatives in America have long sought out rural places to fuel their creativity, from the Hudson River School painters to Bob Dylan and The Band developing their music in Woodstock. But the arts in rural places are not just a byproduct of the scenery; they play a key role in spurring the innovation that ultimately leads to economic development and rising living standards. The myth that urban areas are creative and rural areas are not is just that: a myth.

John Arrillaga and Richard Peery have made a name for themselves as the "Bill Hewlett and Dave Packard of Silicon Valley real estate," according to Bloomberg. Despite the fact that they are little known outside of the Bay Area, the duo has been helping build Silicon Valley, as the region's premier developers, for decades.

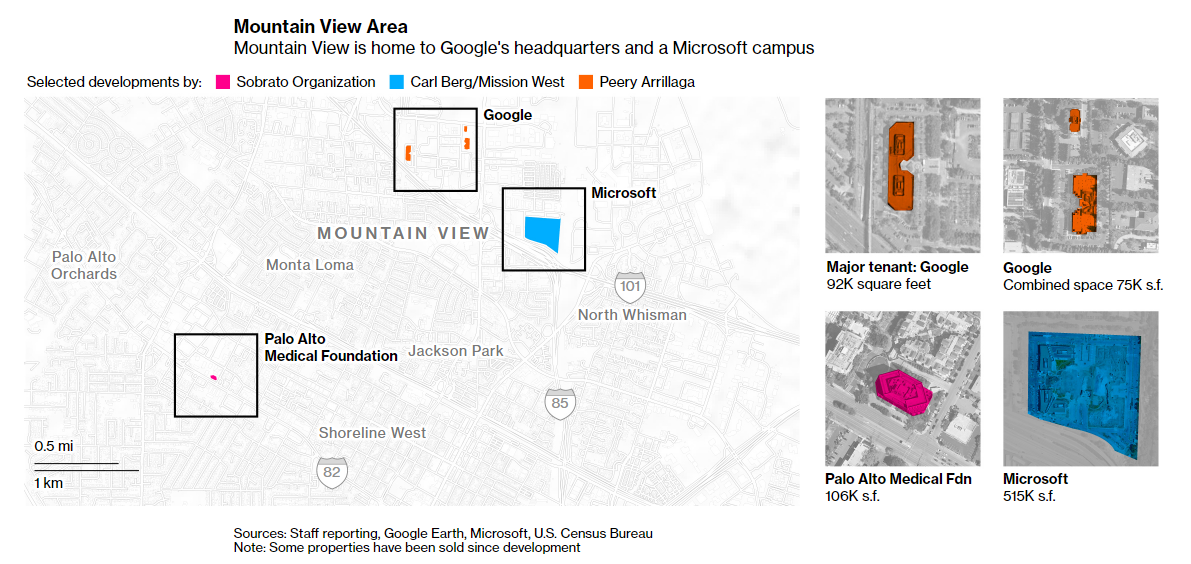

For instance, Google just dropped almost $139 million on "Building 900", a property near Mountain View that was dealt by Arrillaga and Peery.

Arrillaga and Peery have now become billionaires, about a half century after they began buying cherry and apricot orchards in what used to be Santa Clara farm country. Today, they're some of the only people in the area who have gotten rich, but not from tech.

They're worth a combined $6 billion now and two of their contemporaries, John A. Sobrato and Carl Berg, have also reportedly become billionaires.

While tech has been making others rich, it has also put real estate in demand, sending corporate office prices through the roof and bolstering the partners' riches.

Drew Arvay, a managing director at Cushman & Wakefield in San Jose said: “They are just as innovative and creative as Steve Jobs and other giants of the technology world. They continue to lead the market with some of the most influential tenants and developments.”

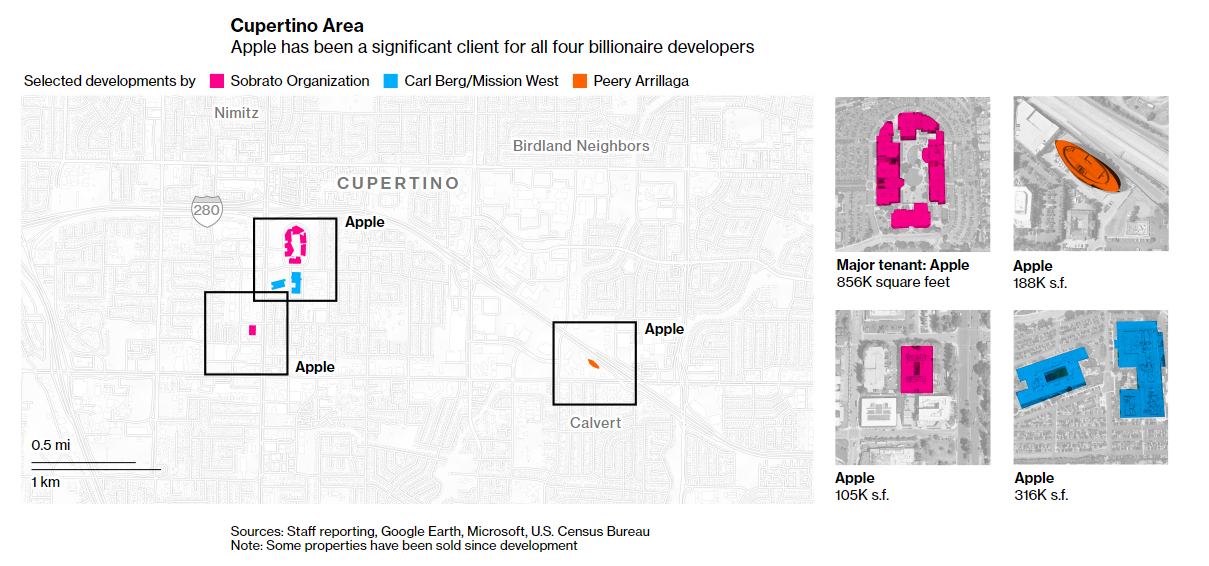

The men are in their 80's now, and started by developing tilt-up buildings that could be constructed quickly and now form the backdrop to much of Silicon Valley. As they got richer, they embarked on bigger projects, developing corporate campuses like Apple's One Infinite Loop, built by the Sobrato Organization in the early 1990s.

Sobrato said:

“No doubt I was in the right place at the right time. Building costs were under $10 a square foot and monthly shell rents were 10 cents or less per month. Today we have the same land selling for over $100 a square foot, building costs of $300 or more per square foot.”

And now Silicon Valley is one of the hottest real estate markets in the country. It's home to Apple, Google parent Alphabet Inc. and Facebook Inc - and many other names that are hungry for real estate.

“The only thing that can keep these companies from growing is not having places to put employees,” Arvay said.

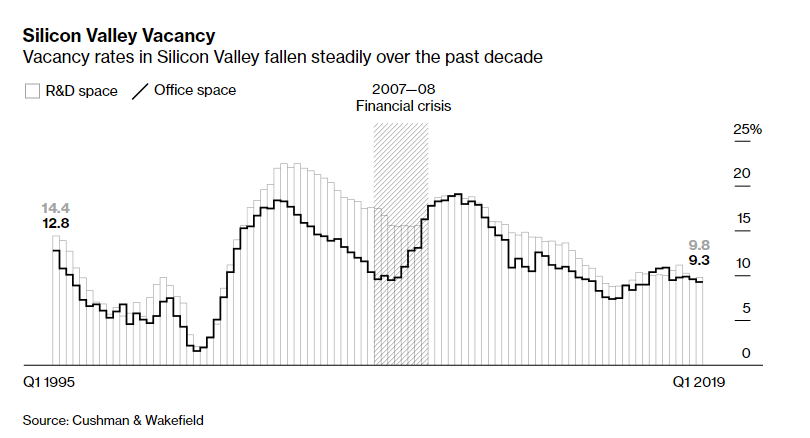

Office rents in Silicon Valley are up 35% over the past decade, while vacancy rates have plunged from 18% to less than 10%. The value of office buildings has tripled since 2010.

At the same time, residential real estate has also surged, a significant tailwind for landlords like Sobrato who own multifamily buildings. The price hikes, however, have also contributed to "growing inequality, homelessness and tension within local communities." Rents were up 40% in the five years leading up to 2017 and the median monthly cost for Santa Clara County came in at $3,800 in May.

But now, the idea of a downturn looms. After a decade of price hikes, Uber's IPO has telegraphed tepid interest in further expansion and capital investment in Silicon Valley. Additionally, some companies are taking on the task of developing their campuses themselves, while at the same time fresh builders like Related Cos. have entered the market.

Peery, Arrillaga, Sobrato and Berg are notable due to their longevity.

Julie Leiker, market director for Silicon Valley at Cushman & Wakefield said: “Throughout numerous cycles—including the oil embargo in the ’70s, the S&L crisis of the late ’80s and early ’90s, then the dot-com bust in 2001 and the Great Recession in the late aughts—the Valley’s real estate market has mirrored the region’s resiliency.”

The developers have also been able to time the market successfully:

Arrillaga and Peery sold a 5.3 million-square-foot portfolio, reportedly about half their holdings at the time, for more than $1 billion in 2006, ahead of the financial crisis. Their double act is still going strong. In addition to the Mountain View deal with Google—which also involved two other properties—they are building an office complex in San Jose where the search company has agreed to lease 729,000 square feet.

Both Sobrato and his son John Michael Sobrato, who led Sobrato Organization from 1997 to 2013, have stepped away from day-to-day operations. But the family still owns the entire company, which is increasingly investing in residential units. It now has more than 6,500 apartments on the West Coast, in addition to 7.5 million square feet of Silicon Valley office space, according to its website. The family’s wealth has almost doubled in the past five years to about $8 billion, according to the Bloomberg index.

Sobrato has focused on philanthropy. He, along with his wife and son, became the first two-generation family to sign Warren Buffett’s Giving Pledge. On top of that, the family has given $550 million to charitable causes since 1996.

Sobrato said: “Our current efforts are focused on how our projects can be both profitable and address some of the critical issues facing our region. Our large-scale developments are nearly all mixed-use with both residential and office space. Combining the two reduces traffic, increases sustainability and helps offset the housing affordability issues created by job growth.”

Phil Mahoney, executive vice chairman of brokerage Newmark Knight Frank said: "While Silicon Valley brokers are bracing for a downturn, the next one could be milder than in the past since technology is now embedded in the global economy. They're doing fine. They're all billionaires."

Just because something is ‘different’ doesn’t make it ‘better’ – just because something is not mainstream doesn’t make it ‘honest.’ We all here agree that mainstream investing sucks, but do we use the same rational methodology when evaluating alternatives? Crypto has proven this is not the case. Investors lost their minds and did all the things they have been told not to do over the years.

So what are alternative investments and how big is this industry?

Alternative Investments are basically any investments other than stocks, bonds, or cash; including stock listed funds like mutual funds. So alternative investments include hedge funds, strategy specific funds (such as a short term bridge loan fund), commodity trading advisors, and even real estate.

As of 2017 there were $8.8 Trillion in Assets in the alternative investment industry according to institutional investor, a media publication that tracks the industry[i]. But what’s interesting is that it’s predicted to grow to $14 Trillion by 2023, only 4 years away:

The alternative investment industry is expected to grow by 59 percent by 2023, reaching $14 trillion in assets in five years’ time, according to new research from alternative investment industry data provider Preqin. The industry managed $8.8 trillion as of the end of 2017, according to Preqin, which says growth will be driven by investors’ need for yield, alternative assets’ strong track record, and a declining number of publicly traded companies. The report, published online Friday, is based on surveys with 300 fund managers and more than 120 institutional investors completed by Preqin in June. The data show that investors plan to increase their allocations to three major categories in the next five years: 79 percent said they would increase their private equity allocation, 70 percent plan to boost allocations to infrastructure, and 62 percent plan to increase allocations to private debt.

Whether you are considering that a shift of funds from one investment sector to another, or just inflation – it still means growth.

So what are the big challenges?

Ultimately, there are only so many strategies. Markets go up, they go down, there are new issues, there are economic events – there are limited components in which to derive a strategy from. And you can bet that Wall St. has analyzed every which way to make a buck, including buying highways from local governments and turning them into toll roads. The problem with many strategies is that they become crowded. That means as the Assets Under Management (AUM) grow, at some point the strategy may reach a limit where it cannot perform at the same level with more capital. Investors like markets like FX and Stocks because liquidity is so deep. However, some strategies may not support assets upwards of $1 Billion USD. Take for example commodities futures strategies. When you start buying $4 Billion worth of S&P contracts, you are likely going to move the price. In fact, hedge funds have used a market making strategy whereby they would buy the futures as a head fake to go short the stock (the capital required to move the futures market vs. the stock market is a mere fraction).

Also managers experience something there is even a term for now ‘style drift’ – it means that managers don’t do what they say they are going to do. This is a big problem. So finding a good manager isn’t easy. Obviously if the industry is growing someone is doing something right. But everything looks good on the surface. When you walk into a bookstore, many of the books look interesting – but you certainly can’t walk away with the whole store. The method of most customers is to focus on a genre they prefer and hone in on some authors they are familiar with or who have high recommendations. These are good strategies but unfortunately like with any product the only way to see if a book is good is to read it. And with investing it’s not a good idea to test a strategy with your own money.

Finally, the track record fallacy needs to be emphasized. The regulators force CTAs to say “Past performance is not indicative of future results” because it’s an open glaring tautology. In first order logic, tautology is something that is always true no matter what. For example 2+2=4 even if you are on an airplane or are mentally deranged.

Just because a strategy did well for the past several years – what makes you think it will do the same in the future? In fact the opposite is true.

“Consider a turkey that is fed every day, Every single feeding will firm up the bird’s belief that it is the general rule of life to be fed every day by friendly members of the human race ‘looking out for its best interests,’ as a politician would say. On the afternoon of the Wednesday before Thanksgiving, something unexpected will happen to the turkey. It will incur a revision of belief.”

This can happen to any strategy – 5 good years of performance and one bad day can wipe it all out. That’s not defeatism, that’s just a possibility. It happens. So the catch is to find strategies that aren’t overleveraged, or who have risk management in place to at least attempt to capitalize positively on volatile moves that would otherwise negatively impact performance.

Every strategy has a potential flaw – we’re not here to suggest there is any perfect strategy. Our idea is that if you can eliminate or at least reduce losses – what you have left is profit. That means investors should be even paranoid about things that can go wrong, like the I.T. guy who thinks the world is going to end. Remember that there was a guy screaming to the SEC that Madoff was a fraud. Usually things are staring right in front of you. Like with Gold & Silver – sorry guys, the markets are manipulated. The argument for Gold 50,000 is strong – but if the market is completely rigged than the price is whatever the Rothschild fixing group says it is. So until there is another system in place, Gold isn’t going to 50,000 and neither is Bitcoin.

But if there’s one takeaway from this article it should be that if you don’t have the time, expertise, money, and nerves to invest in doing your own investing – find a professional who can do it for you.

Pre IPO Swap 5/5/2019 – (New York, NY) — With Lyft, Uber, Pinterest and others going live, we’re now looking further down the line to companies that are still some time away. Today we’ve added Cabify and Go Jek both non-US offerings in a similar space. But when we say ‘similar’ it means exactly that – they are both in the same industry as Lyft and Uber but clearly different models and they are exclusively outside the US market.

Go-Jek was founded by Nadiem Makarim, a native Indonesian, who holds degrees from Brown University and Harvard Business School. He worked at McKinsey and Co. consulting for three years before starting Go-Jek from a tiny call centre with only 20 ojek drivers, who later became recruiters. As a loyal ojek user, Nadiem discovered that ojek drivers spend most of their time waiting for customers, while customers waste time walking around looking for an available ojek. Go-Jek was built to solve this problem, by providing a platform where drivers and riders can connect efficiently and allowing those drivers to improve their income.