With the recent news that Tesla has now purchased $1.5 billion in bitcoin, there's going to be no shortage of people that follow Elon Musk and make their first foray into crypto as well. And, since a majority of the country is broke, it seems like a great time for what is essentially crypto lending to emerge.

Enter "flash loans" - a new service where borrowers can very quickly take collateral free loans from lenders and use the proceeds for whatever they want, before quickly paying the loan back - sometimes in seconds. The most popular use for these loans has been arbitraging coin prices on different crypto exchanges, according to Bloomberg. But what makes these loans different is that they are "bundled into the same block of transactions being processed on the Ethereum digital ledger and are executed simultaneously".

The loans sometimes take just seconds:

In the example, the transaction gets submitted to the network, temporarily lending the borrower the funds. If the trade isn’t profitable, the borrower can reject the transaction, meaning that the lender gets their funds back in either case. As far as the blockchain is concerned, the lender always had the funds. The user pays blockchain processing fees.

“In a way, flash loans make everyone a whale,” said Nikola Jankovic of loan provider DeFi Saver. Another player in the flash loan space, Aave, says it has already processed $2 billion in flash loans just last year alone.

The outlook for the loans is robust, according to crypto investor Aaron Brown: “I can see them becoming big. The same thing exists conceptually in the traditional financial system. I can buy and sell things for many times my total wealth during a day, as long as by the end of the day everything nets out to a positive balance. It’s just with crypto there is no settlement delay, so to do the same thing you need flash loans."

“At the end of the day, flash loans are going to be everywhere,” Stani Kulechov, Aave's CEO, said.

Jack Purdy, an analyst at researcher Messari commented: “They have the potential to greatly increase market efficiency as there are no longer high capital costs to exploiting arbitrage opportunities. When anyone in the world can execute these trades across disparate markets, it helps crypto prices converge, tightening spreads and reducing inefficiencies.”

On the other side of the "coin", however, the loans can also be used to manipulate coin prices. “Flash loans will continue to be associated with manipulation and hacks. But they’re not really essential to those things, they just mean manipulators and hackers no longer need capital,” Aaron Brown concluded.

President Joe Biden’s nominee to be chairman of the Securities & Exchange Commission, Gary Gensler, who we profiled here and is referred to as "the sheriff", could have a net worth between $41 million and $119 million.

Gensler was previously the chairman of the CFTC and a partner at Goldman Sachs. He disclosed his net worth as part of disclosures he had to file with the Office of Government Ethics, Bloomberg noted on Friday. A majority of his money was made at Goldman, where he joined in the late 1970's after graduating from the University of Pennsylvania. He became one of the youngest partners in Goldman Sachs history.

Gensler's largest holding is a stake worth $25 million and $50 million in the Vanguard Total Stock Market ETF. He also disclosed that he had between $50,000 and $100,000 in capital gains from holding shares of Tesla, the only stock that is listed individually on his disclosures. He has since sold the position.

He also disclosed that he will participate in a benefit plan from Goldman Sachs which is expected to pay out $977 per month starting at age 71.

Recall, we wrote about Gensler's nomination in mid-January.

His arrival will likely be a stark difference from the last 4 years of Jay Clayton, as Gensler's resume includes going to war with major financial titans when he was head of the Commodity Futures Trading Commission - and winning. Financial lobbyists sometimes simply called him "the enemy" during the 2010 Dodd-Frank Act battle.

Justin Slaughter, a consultant at Mercury Strategies, said: “The sheriff is coming to the preeminent financial regulator in the world. It means regulation and enforcement are about to get much tougher.”

When he arrives at his post, Gensler will not only have to deal with a Fed-induced stock market mania, but also tensions with China and the growth of private equity.

Graham Steele, who served as an aide to Senator Sherrod Brown of Ohio, said: “He developed a reputation for being adversarial to Wall Street because he came from the industry and understood the business so he could push back against their arguments when they were hollow.”

Ian Katz, an analyst at Capital Alpha Partners in Washington, commented: “What’s really unnerving to a lot of people is that it’s pretty clear that he doesn’t need them. He doesn’t need to go back there for a job, he’s made his money. He’s not terribly interested in who he ticks off or not and that’s very powerful.”

By Jeff Kauflin, Antoine Gara and Sergei Klebnikov

It’s just after midnight on Friday, July 31, and the Todd Capital Options Community, a $20-per-month subscription Slack channel favored by thousands of novice options traders, is buzzing with life. Unemployment is soaring and governments worldwide are desperately trying to fend off economic collapse. But members of this online enclave are partying, quite literally, like it’s 1999—the infamously frothy day-trading year before the dot-com bubble burst in March 2000.

Despite the pandemic, Amazon, Apple, Facebook and Google have just released jaw-dropping financial results, a staggering $205 billion in combined quarterly sales and $34 billion in earnings during a stretch when U.S. gross domestic product plunged at an annualized rate of 33%. For weeks, the club’s youthful members have been loading up on speculative call options using the mobile trading app Robinhood. Now they’re ready to cash in.

“Literally, NOTHING will make me sell my AMZN 10/16 calls tomorrow. I don’t care what happens. . . . I’m holding everything. Keep ya boi in your prayers,” says one user named JG. As dawn approaches, “NBA Young Bull” announces: “Good morning future millionaires . . . is it 9:30 yet?”

For these speculators, the adrenaline rush turned to euphoria after Apple not only beat earnings expectations but announced a 4-for-1 stock split, luring more small investors to the iPhone maker’s stock party. At 9:30 a.m. Friday, when trading begins, the call options on Apple and Amazon held by many of these market newbies pay out like Las Vegas slot machines hitting 7-7-7 as both tech giants gain a collective quarter-trillion dollars in market value. Throughout the day and over the weekend, a stream of posts scroll by from exuberant Robinhood traders going by screen names like “See Profit Take Profit” and “My Options Give Me Options.” On Monday, August 3, the Nasdaq index sets a new record high. (seeRobinhood Returns below)

The Physics of Amateur Trading: Baiju Bhatt (left) and Vladimir Tenev (pictured in 2015) met as physics students at Stanford. Even the best modeling could not have predicted that $1,200 stimulus checks would propel them to billionaire status.

KITTU KOLLURI

Welcome to the stock market, Robinhood-style. Since February, as the global economy collapsed under the weight of the coronavirus pandemic, millions of novices, armed with $1,200 stimulus checks and nothing much to do, have begun trading via Silicon Valley upstart Robinhood—the phone-friendly discount brokerage founded in 2013 by Vladimir Tenev, 33, and Baiju Bhatt, 35.

The young entrepreneurs built their rocketship by applying the formula Facebook made famous: Their app was free, easy to use and addictive. And Robinhood—named for the legendary medieval outlaw who took from the rich and gave to the poor—had a mission even the most woke, capitalism-weary Millennial could get behind: to “democratize finance for all.”

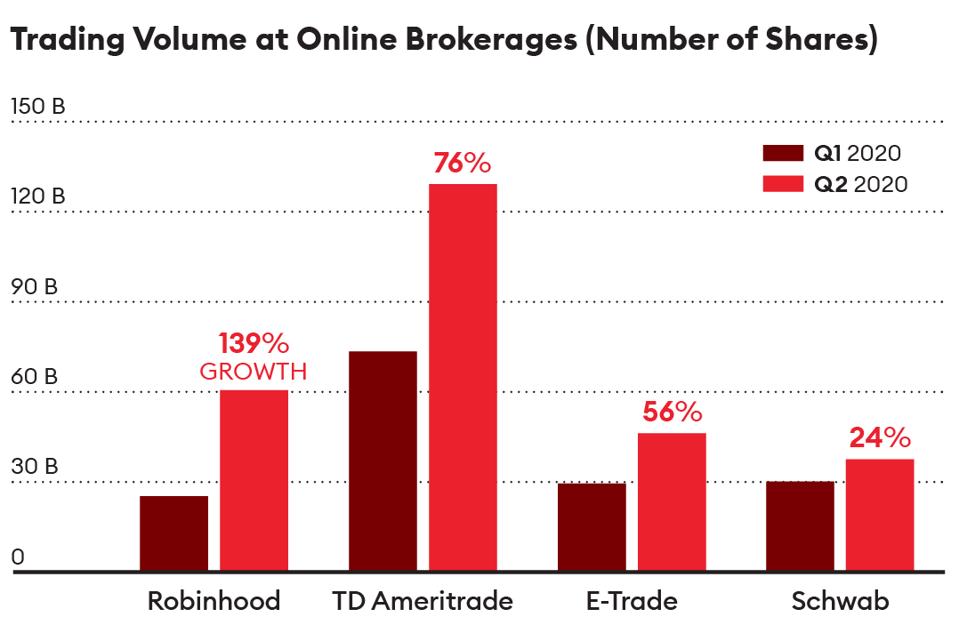

Covid-19 and the flow of government handouts have been manna from heaven for Robinhood. The firm has added more than 3 million accounts since January, a 30% rise, and it expects revenue to hit $700 million this year, a 250% spike from 2019, according to a person familiar with the private company’s finances. Not since May Day 1975, when the SEC deregulated brokerage commissions, giving rise to discount brokerages like Charles Schwab, has there been a more disruptive force in the retail stock market. Robinhood’s commission-free trading is now standard at firms including TD Ameritrade, Fidelity, Schwab, Vanguard and Merrill Lynch.

And Robinhood’s merry traders are moving markets: Certain stocks—Elon Musk’s Tesla, marijuana conglomerate Cronos, casino operator Penn National Gaming and even bankrupt car-rental company Hertz—have become favorites, swinging wildly on a daily basis. For the first time ever, according to Goldman Sachs, options speculators like the ones Robinhood has cultivated have caused single-stock option-trading volumes to eclipse common-stock trading volumes, surging an unprecedented 129% this year.

Lord of the Buys

The Covid bull market has been a godsend for retail brokers, but Robinhood and its swarm of newbie traders is schooling the competition.

Source: Piper Sandler

“I think you’ve seen a unique situation in the history of financial markets,” Tenev tells Forbes, working remotely from his home not far from Robinhood’s Menlo Park, California, headquarters, which resemble a beach house. “Typically when a market crash is followed by a recession, retail investors pull out. Institutions benefit. . . . In this case, Robinhood customers started opening new accounts and existing customers started putting in new money. This bodes positively for society and our economy if millions are investing when they otherwise wouldn’t have.”

Like any skilled trader, Tenev is talking his book. His proclamations ring a bit hollow, though, once you look more closely at what is actually driving his digital casino. From its inception, Robinhood was designed to profit by selling its customers’ trading data to the very sharks on Wall Street who have spent decades—and made billions—outmaneuvering investors. In fact, an analysis reveals that the more risk Robinhood’s customers take in their hyperactive trading accounts, the more the Silicon Valley startup profits from the whales it sells their orders to. And while Robinhood’s successful recruitment of inexperienced young traders may have inadvertently minted a few new millionaires riding the debt-fueled bull market, it is also deluding an entire generation into believing that trading options successfully is as easy as leveling up on a video game.

Stock options are contracts to buy or sell underlying shares of stocks for a set price over a specified period of time, typically at a fraction of the cost. Given their complexity, options trading has long been the realm of the most sophisticated hedge funds. In 1973, three Ph.D.s—Fisher Black, Myron Scholes and Robert Merton—developed an options pricing model that eventually won them the Nobel Prize in economics. Today their mathematical model, and variations of it, are easily incorporated in trading software so that setting up complicated—and risky—trades is no more than a few clicks away. Even so, making wrong bets is easy. According to the Options Clearing Corporation, more than 20% of all options contracts expire worthless versus 6% “in the money.”

In June, Robinhood witnessed firsthand what can happen when such tools are marketed to inexperienced investors. While it’s impossible to discern every factor contributing to suicide, one of Robinhood’s new customers, a 20-year-old college student from Illinois named Alexander Kearns, took his own life after mistakenly thinking that one of his options trades put him in debt to Robinhood for more than $730,000. His death prompted questions from several members of Congress about the platform’s safety.

Robinhood has sold the world a story of helping the little guy that is the opposite of its actual business model.

Despite these problems, millions continue to flock to the addictive app, and Tenev and Bhatt sit on a potential gold mine reminiscent of Facebook in its pre-IPO days. Amid its Covid-19 business surge, Robinhood has raised $800 million from venture investors, ultimately giving it a staggering $11.2 billion valuation, affording its cofounders a paper net worth of $1 billion each. But in light of Morgan Stanley’s success with its $13 billion acquisition of E-Trade in February and Schwab’s earlier purchase of TD Ameritrade for $26 billion, some think Robinhood could garner a $20 billion valuation if it went public or were acquired.

The problem is that Robinhood has sold the world a story of helping the little guy that is the opposite of its actual business model: selling the little guy to rich market operators with very sharp elbows.

The rise of Vladimir Tenev and Baiju Bhatt is a familiar one in the era of technology disruption.

They met as undergrads at Stanford University in the summer of 2005. “We had some astounding parallels in our lives,” Bhatt tells Forbes. “We were both only children, we had both grown up in Virginia, we were both studying physics at Stanford, and we were both children of immigrants because our parents were studying Ph.D.s.” Tenev’s family emigrated from Bulgaria, Bhatt’s from India.

Tenev, the son of two World Bank staffers, enrolled in UCLA’s math Ph.D. program but dropped out in 2011 to join Bhatt and build software for high-frequency traders. That was shortly after Wall Street’s 2010 “Flash Crash,” a sudden, near-1,000-point plunge in the Dow Jones Industrial Average at the hands of high-speed traders. The extreme volatility exposed how financial markets had mostly moved away from the staid, but stable, New York Stock Exchange and to a smattering of opaque quantitative trading pools dominated by a handful of secretive firms. These so-called “Flash Boys,” who worked milliseconds ahead of orders from both retail and institutional investors, had emerged from lower Manhattan’s back offices and IT departments, as well as university Ph.D. programs, to become the new kings of Wall Street.

Billionaires in Sherwood Forest: Forbes 400 members who feast on Robinhood customer trades (from left) Citadel Securities, owned by Ken Griffin; Two Sigma Securities, cofounded by David Siegel; Virtu Financial, founded by Vincent Viola

DAVID PAUL MORRIS/BLOOMBERG; MISHA FRIEDMAN/BLOOMBERG; WALTER MICHOT/MIAMI HERALD/NEWSCOM

At the same time Tenev and Bhatt were getting an insider’s education in how high-frequency traders operate and profit, the outside world was in turmoil, recovering slowly from the battering of the 2008–2009 financial crisis. It all played into the official Robinhood creation story: When the 2011 Occupy Wall Street movement materialized as a protest of bailouts on Wall Street and foreclosures on Main Street, one of Tenev and Bhatt’s friends accused them of profiteering from an unequal system. Soul searching led the pair in 2012 to conceive Robinhood, a trading app with a name that was an explicit reference to leveling the playing field. The most obvious—and disruptive—innovation: no commissions and no minimum balances, at a time when even low-cost rivals like E-Trade and TD Ameritrade made billions on such fees.

Initially, Tenev and Bhatt used the allure of exclusivity to capture interest. For their 2013 launch, they restricted access, building up a 50,000-person waiting list. Then they turned the velvet rope into a game, telling prospective users they could move up the waitlist by referring friends. By the time they launched on Apple’s App Store in 2014, Robinhood had a waitlist of 1 million users. They had spent virtually nothing on marketing.

Bhatt focused maniacally on app design, trying to make Robinhood “dead simple” to use. iPhones flashed with animations and vibrated when users bought stocks. Every time Bhatt came up with a new feature, he’d run across the street with staffers from Robinhood’s Palo Alto office to Stanford’s campus, approaching random students, asking for feedback. The app won an Apple Design award in 2015, a prize given to just 12 apps that year. Millennial customers started downloading it in droves.

By the fall of 2019, Robinhood had raised nearly $1 billion in funding and swelled to a $7.6 billion valuation, with 500 employees and 6 million users. Tenev and Bhatt, both minority owners of Robinhood with estimated 10%-plus stakes, were rich.

Flow Rider

Robinhood's entire business is built on selling its customers’ orders to trading titans like Citadel Securities. At Schwab, so-called PFOF or “payment for order flow” only accounts for 3% of revenues. ETrade, 17%.

Sources: Regulatory filings and industry experts.

Then, in September 2019, Goliath bowed low to David. Over a 48-hour span, E-Trade, Schwab and TD Ameritrade, industry giants many times Robinhood’s size, cut commissions to $0. A few months later, Merrill Lynch and Wells Fargo’s brokerage unit followed suit. As this source of revenue evaporated, brokerage stocks plunged, and TD Ameritrade soon entered a shotgun marriage with Schwab, while E-Trade ran into the arms of Morgan Stanley.

Two Millennials had done something that discount giants like Vanguard and Fidelity could never accomplish. They had dealt the final blow to the easy-money trading commissions that had fed generations of stockbrokers and formed the financial foundation of Wall Street brokerage firms.

The secret sauce of Robinhood’s success is something its founders are loath to publicize: From the beginning, Robinhood staked its profitability on something known as “payment for order flow,” or PFOF.

Instead of taking fees on the front end in the form of commissions, Tenev and Bhatt would make money behind the scenes, selling their trades to so-called market makers—large, sophisticated quantitative-trading firms like Citadel Securities, Two Sigma Securities, Susquehanna International Group and Virtu Financial. The big firms would feed Robinhood customer orders into their algorithms and seek to profit executing the trades by shaving small fractions off bid and offer prices.

Robinhood didn’t invent this selling of orders—E-Trade, for example, earned about $200 million in 2019 through the practice. Unlike most of its competitors, though, Robinhood charges the quants a percentage of the spread on each trade it sells, versus a fixed amount. So when there is a large gap between the bid and asked price, everyone wins—except the customer. Moreover, since Robinhood’s customers tend to trade small quantities of stocks, they are less likely to move markets and are thus lower-risk for the big quants running their models. In the first quarter of 2020, 70% of the firm’s $130 million in revenue was derived from selling its order flow. In the second quarter, Robinhood’s PFOF doubled to $180 million.

Given Tenev and Bhatt’s history in the high-frequency trading business, it’s no surprise that they cleverly built their firm around attracting the type of account that would be most desirable to their Wall Street trading-firm clients. What kind of traders make the most saleable chum for giant sharks? Those who chase volatile momentum stocks, caring little about the size of spreads, and those who speculate with options. So Robinhood’s app was designed to appeal to the video-game generation of young, inexperienced investors.

Options Trades are Prime Steak for Robinhood’s real customers, the Algorithmic Quant Traders.

Besides being given one share of a low-priced stock to start you on your investing journey, one of the first things you notice when you begin trading stocks on Robinhood and are authorized to trade options is that the bright orange button right above BUY on your phone screen says TRADE OPTIONS. Options are sexier than stocks because, like hitting a single number on a roulette wheel, they can offer more bang for the buck.

Options trades also happen to be prime steak for Robinhood’s real customers, the algorithmic quant traders. According to a recent report by Piper Sandler, Robinhood gets paid—by the quants—58 cents per 100 shares for options contracts versus only 17 cents per 100 for equities. Options are less liquid than stocks and tend to trade at higher spreads. While the company says only 12% of its customers trade options, those trades accounted for 62% of Robinhood’s order-flow revenues in the first half of 2020.

The most delectable of these options trades, according to Paul Rowady of Alphacution, may very well be so-called “Stop Loss Limit Orders,” which give buyers the opportunity to set automatic price triggers that close their positions in an effort either to protect profits or limit losses. In October 2019, Robinhood gleefully announced to its customers, “Options Stop Limit Orders Are Here,” a nifty feature which essentially puts trading on autopilot.

“That [stop limit] order is immediately sold to a high-speed trader who now knows where your intention is, where you would sell,” says one former high-speed trader. “It’s like you’re writing a secret on a piece of paper and handing it to your broker, who sells it to someone who has an interest to trade against you.”

Robinhood refutes the notion that its model preys on inexperienced investors and claims most of its customers use a buy and hold strategy. “Receipt of payment for order flow is a common, legal and regulated industry business practice,” says a Robinhood spokesperson who insists the app helped customers save $1 billion on trades this year. “We are focused on providing a platform that makes finance accessible and approachable and where people can make thoughtful, informed investing decisions.”

Billionaire competitor Thomas Peterffy, the founder of Interactive Brokers, says stop limit orders are the most valuable orders a sophisticated trader can buy. “If people send you orders, you see what they are. You can plot them up along a price axis and see how many buy and sell orders you have at each of those prices,” he says.

For instance, if a buyer sees sell orders bunched up around a certain price, it means that if the stock or option hits that price, the market is going to fall hard. “If you are a trader, it’s good for you if you can trigger the stop—you can go short and trigger the stop, and then cover much lower,” Peterffy says. “It’s an old technique.”

In a sense, Covid-19 has been both a blessing and a curse for Robinhood.

The pandemic forced millions of future Robinhood customers home to shelter in place, free from diversions like sports and armed with fast internet connections and free money from the government. The stock market, meanwhile, provided edge-of-your-seat excitement as it plunged and then soared, propelling superstars like Amazon and reviving walking-dead stocks like Chesapeake Energy. The result was unprecedented growth for the upstart brokerage. Robinhood now has more than 13 million registered customer accounts, nearly as many as venerable Charles Schwab, which after 49 years has 14 million funded accounts, and more than twice as many as E-Trade, with 6 million accounts.

Robinhood Returns

Robinhood may profit handsomely from its customers accounts, but that doesn’t mean some aren't also reaping big rewards. Take the entrepreneur behind Robinhood Slack channel, Todd Capital Options Community, Charles L. Oglesby III, 33. The personal injury lawyer and former stock broker started the business as a hobby with friends who joined him in an investment club focused on stock and options trading, real estate, and even owning networks of vending machines for cash flow. A year ago, he posted a few educational videos on Youtube about options trading that went viral after he promoted them to his Instagram followers. He turned his videos into a tutorial series and charged $139 for access.

Once the Covid-19 quarantines started his business exploded and for a month or so his videos were bringing more than $130,000 per week. In March Oglesby started his subscription Slack channel for DIY Robinhood traders, charging 19.99 per month. It now has nearly 4,500 members who pay him some $90,000 a month and hums with activity 24 hours a day, 7 days a week.

On Slack, his members share trade ideas and have neatly organized threads like “call outs and research,” where they mine the upcoming earnings reports and option chains in hopes of discovering out-of-the-money call options that might yield a jackpot. There’s an “Options Wins” thread where members post screenshots of big trading wins, and an “Option Loss Analysis” channel to cope with bets that expire worthless. Oglesby even hired a few frequent posters to become “administrators” of the channel, paying them between $500 and $1,000 a month to curate ideas and host weekly conference calls over Zoom.

The club is made in large part of working millennial-aged minorities, including a large number of women. Many have turned to trading options on Robinhood to help solve their crushing student loan debts, stagnant wages and address the yawing racial wealth gap.

“A lot of these people are in a rush. The idea of compounding 6% off of $1,000 in savings, it's just not going to do them any good,” says Oglesby.— Antoine Gara

The company has also been a game changer for some of its clients. Taylor Hamilton, 23, an IT worker who graduated from the University of Pennsylvania in 2018, opened a Robinhood account and began trading in March. He began buying put options against plummeting travel-industry stocks like Delta and Uber, and later bought calls on Boeing and other beaten-down companies, correctly figuring that they would benefit from the government’s de facto bailout via the bond market.

After four months and 300 trades, Hamilton has netted nearly $100,000 and paid down his $15,000 in student loans. “It felt like a once-in-a-lifetime opportunity,” says Hamilton, who reports that he has transferred most of his profits to his bank account to eliminate the temptation to trade away his gains.

The pandemic has also exposed Robinhood’s warts. During the market’s 5% one-day swoon and subsequent rebound in early March, Robinhood’s customers were completely shut off from their accounts for nearly two days as the brokerage firm’s technology systems crumpled under the weight of a tenfold jump in order volume. Angry customers lashed out against Robinhood on social media, and more than a dozen lawsuits were filed against the company.

In the last few months, Robinhood has quietly been restructuring. Tenev says it’s making major technology investments to increase capacity and add redundancy. A sizable chunk of its $800 million in fresh venture capital is going toward upgrades and adding engineers to the 300 already on staff.

In the wake of the Kearns tragedy, Robinhood’s options-trading interface is also being overhauled. The company has pledged to help educate its customers on the highly speculative nature of the trades. That includes hiring an “Options Education Specialist” and “rolling out improvements to in-app messages and emails” that it sends to customers about their complex options trades. In August, the brokerage app said it would hire hundreds of new customer-service representatives in its Texas and Arizona offices by the end of 2020.

According to insiders, there’s a sense of urgency at the company these days. For two years, Robinhood has been speaking publicly about an IPO. With interest rates near zero and the stock market roaring, the public-offering window is wide open, but it won’t be forever.

A better option—especially considering Robinhood’s current problems—might be a quick sale to a full-service firm such as Goldman Sachs, UBS or Merrill Lynch. Such a sale would surely provide billion-dollar windfalls for its young founders, Tenev and Bhatt. And as any good trader knows, it’s much better to sell when you can than when you have to.

Last week, in a historic sequence of events on Wall Street, the struggling mall-based videogame retailer GameStop (Ticker: GME) was the subject of an epic “short squeeze” ignited primarily by individual investors on the Reddit message board r/wallstreetbets (WSB). Members of WSB implored each other to purchase shares of GME; a buying frenzy ensued. The stock, heavily “shorted” by certain hedge funds and other professional investors increased to nearly $500, up from just ~$20 in early January. Additional stocks including AMC Entertainment (AMC), BlackBerry (BB), Bed Bath & Beyond (BBBY), and a few others were caught up in the buying hysteria. Hedge funds and other professional investors suffered severe losses. After the fact, certain WSB members and other retail investors were in a jovial, celebratory mood. Together, they bet against the supposed smartest people in the room…and won. It was an apparent victory for the little guy. Or was it?

What Happened

During the speculative mania’s zenith, the retail stock and options trading platform Robinhood enacted sudden changes to their platform. Without warning, account holders were banned and or severely curtailed from trading in the shares of GME and other heavily volatile stocks; only sell orders to liquidate existing positions were permitted. Immediately thereafter, a collective rage took hold.

Politicians on both sides of the aisle, Robinhood customers, market pundits, and even entertainers lashed out at Robinhood. In their view, the brokerage firm’s actions unfairly punished individual investors while professionals were left unscathed. Said David Portnoy, founder of the popular website Barstool Sports, “@RobinhoodApp entire business model is to cater to the exact people they are now trying to fck with and scare into selling. They will never recover from this.” As usual, Senator Elizabeth Warren (D-MA) blamed “hedge funds, private-equity firms and wealthy investors…for…treating the stock market like their own personal casino while everyone else pays the price.” Gavin Wax, President of the New York Young Republican Club accused Wall Street of “corporatizing the American dream and making a mockery of American freedom.” Curtis Sliwa, founder of The Guardian Angels, a “volunteer organization of unarmed crime-prevention,” apparently had a change of heart when he encouraged his followers to “get these hedge-fund monsters before they get us.” In a rare moment of unity, Alexandria Ocasio Cortez (AOC) (D-NY) & Ted Cruz (R-TX) both voiced their displeasure at Robinhood for helping hedge funds to the detriment of day traders. How ironic, for the first time in political history, AOC and Ted Cruz agreed…and they were both wrong. Let us be clear, the optics (and explanation) of what transpired were abysmal. That said, the statements above are categorically incorrect, highly irresponsible and were spit by people who share one important property in common. They have absolutely no clue what they are talking about.

In truth, the happenings of last week were complex, multi-faceted, and extremely granular. They involved the plumbing of financial markets that very few people, except dedicated experts, fully comprehend. In fact, many people who work in finance themselves do not fully grasp the magnitude of terms such as T+2 trade settlement, margin calls, margin loans, collateral, collateral calls, implied volatility, and so forth, that are closely intertwined and imperative in maintaining an orderly process of buying, selling, and shorting stocks and settling those trades. In this post, we will try our best to explain, in plain English, what transpired and dispel many of the falsehoods that are circulating on (and off) line.

Capital Punishment: Why Robinhood Restricted Trading

Did Robinhood restrict trading to “screw the little guy,” as Curtis Sliwa so eloquently espoused? How about to bail out hedge funds that were caught in a short squeeze? Or to help Citadel and Point72, two firms that injected capital into a hedge fund called Melvin, that had suffered losses in GME? Or did Robinhood throttle back because they are in the view of Mr. Portnoy, “the biggest frauds of them all” and because “too many ordinary people are getting rich”? The simple answer(s) to all these questions is unequivocally “no.”

Robinhood curbed trading because a sudden onset of activity concentrated in a few stocks, combined with the volatility of those stocks, left them desperately short of cash. If they did not take decisive action, they risked insolvency. In fact, in addition to restricting trading, Robinhood simultaneously drew down all their existing credit lines. Worth noting is that drawing on credit lines is an expensive form of financing. Firms draw on credit lines when they must, not because they want to. Finally, to further strengthen their balance sheet, Robinhood raised billions of dollars of additional capital as expeditiously as possible.

But Wait, How Could Robinhood “Run Out Of Cash”?

When an investor purchases (or sells) a stock, they see (and have come to expect) the funds credited (or debited) to their account instantaneously. Typically, they can use those funds to purchase another security, withdraw the cash, and or for collateral. What they do not see is the backend complexities that must work seamlessly for the aforementioned to be facilitated.

Unbeknownst to most investors is that almost all stock trades take 2 business days to “settle.” In Wall Street parlance, this is called T+2 settlement. Because there is a lag from the time a trade is executed to the time it settles, an investor’s broker – in this case Robinhood – must ensure they have enough cash on hand to meet customer demands until the trade settles. And since so many customers were trading GME at one time, often on the same “side” of the trade, Robinhood’s cash position dropped precipitously.

Like all brokers, Robinhood allows qualified clients to trade on “margin,” or with borrowed money. Robinhood earns a fee for providing this financing. However, should one of their customers fail to meet a margin call (pay back the loan), Robinhood would be on the hook for the funds. Some customers were buying shares of GME using borrowed funds (or margin). If the shares of GME dropped by a certain percentage, a customer might face a “margin call,” meaning the balance in their account had fallen below a minimum maintenance level required by law. When this happens, an investor must deposit more funds into their account. If they fail to do so, their broker is obliged to liquidate some or all their remaining holdings to satisfy the margin call. If the cash derived from liquidating a customer’s account is not sufficient to cover the margin call, the broker (Robinhood) is responsible for the balance. A disproportionate amount of customers trading shares in one extremely volatile stock, GME, thrusted Robinhood into an extraordinarily difficult and highly unusual situation; too many customers might be unable to meet margin calls simultaneously, forcing Robinhood to draw down their cash reserves to fill the difference.

Finally, all brokers clear and settle trades through an intermediary called The Depository Trust and Clearing Corporation (DTCC). To better understand what DTCC’s function is, imagine it as a broker to all brokers, or a reinsurer to all brokers. The “buck” excuse the pun, stops with them. The DTCC demands cash collateral (think of it as an insurance premium) from all clearing brokers, including Robinhood. The amount of capital they require depends on various quantitative factors (think of how an insurance company prices a life insurance policy). When market conditions change, the DTCC can, and often does, demand more (or less) collateral from clearing brokers. Last week’s buying binge in a few highly speculative, volatile stocks prompted DTCC to raise cash collateral requirements to protect the financial system’s integrity. Because Robinhood had a disproportionate number of retail accounts trading in these securities, they had to come up with a lot of cash, and quickly. Robinhood was far from the only affected broker. Noted Thomas Peterffy, the well-respected chairman of the brokerage firm Interactive Brokers, (we were) "concerned about the ability of the market and the clearing systems, through the onslaught of orders, to continue to provide liquidity. And we are concerned about the financial viability of intermediaries and the clearing houses.”

Paying For Order Flow

Robinhood does not charge brokerage commissions for stock and options trading; customers can trade for free. Indeed, the lure of zero commissions has been a huge driver of demand for retail brokerage services throughout the financial services community. This then begs the question: How does Robinhood make money? One way is by charging interest to customers who trade on margin. Another way is through something called “payment for order flow.” Here is an oversimplification of how it works: Retail brokerage firms like Robinhood, Ameritrade, Fidelity, etc., route customer orders to sophisticated firms called market makers in exchange for cash payments. Two of the largest market makers are Citadel Securities and Virtu Financial. These firms and other market makers pay for this order flow for the simple reason that they can trade against it for a profit.

The merits of paying for order flow go well beyond the scope of this post. In short, detractors say there is an inherent conflict of interest. Advocates say it facilitates low or no cost trading for individual investors and the opportunity for “price improvement." In this post, we only mention payment for order flow to dispel some nonsensical arguments from a peanut gallery of ill-informed charlatans. Suppose Robinhood was out to “screw the little guy” and or involved in a conspiracy with other professional market participants to illegally profit at the expense of individual investors. Why would they restrict trading in their most heavily traded stocks and by doing so, have less customer order flow to sell and earn a profit from? They would not. Bottom line, the more Robinhood’s customers trade, the more order flow Robinhood can sell; the more order flow Robinhood sells, the more money Robinhood makes, not the other way around.

Legitimate Beef

The action taken by Robinhood and many other retail brokers last week was not only correct, but it was also well within their legal rights. Still, it is also worth calling out certain market professionals on their hypocrisy; for in the past, they have profited from the very thing they are now complaining about, which is a coordinated a short squeeze. This time, however, they were the ones nursing losses.

Said Nicholas Colas, co-founder of DataTrek Research, “Retail investor wolf packs are new, but if you’ve ever sat on a hedge fund trading desk you know squeezing shorts has been a Wall Street blood sport for decades.”

Most professional investors are honest, hard-working people that adhere to the rules and (try to) earn legitimate profits. They do not get involved in activities that stretch the bounds of legality. Still, we can certainly understand and appreciate why the general public has little if any sympathy for a few hedge fund managers crying foul because now, instead of them orchestrating and profiting from a short- squeeze by sharing information at an idea dinner or investment summit, it is retail investors on reddit doing something similar.

Short Sellers & Short Sightedness

True to form in acting reactively instead of proactively, the Senate Banking Committee and other regulators will hold hearings on the “current state of the stock market.” Among the topics of discussion will be restrictions or even banning the practice of short selling. This is a terrible idea.

Short sellers are good for the stock market. And despite what some ill-informed people say, short selling specialists protect individual investors in a myriad of ways. How? Traditional Wall Street analysts almost always (~90%) have “Buy” or “Hold” recommendations on stocks. One reason for this is because financial malfeasance is often extraordinarily difficult to identify. Short sellers are experts at rooting out nefarious behavior. They provide a vital service to individual investors, sniffing out corporate misdeeds such as aggressive accounting and even outright fraud. Their research helps keep companies honest and investors well-informed. Worth noting, it was not Wall Street analysts that alerted the investing public (and regulators) about the multi-billion-dollar frauds Enron, WorldCom and SinoForest. It was short sellers. Finally, during normal stock market corrections short sellers often purchase shares they have previously sold short to close out their trades. This helps stabilize the market during a downturn, when most market participants want to sell. Eliminate short selling, and you eliminate a natural buyer of stocks, at precisely the juncture when you need them most.