ETFs used to be touted as a great way to gain exposure to the stock market. But now, thanks to fee-hungry issuers, the tail is wagging the dog and ETFs are the stock market.

As far back as late 2017, there were just 3,671 domestic listings, according to the Wall Street Journal. The number had declined due to the growth of venture capital and private equity.

"The number of public companies in the U.S. has been on a steady decline since peaking in the late 1990s. In 1996 there were 7,322 domestic companies listed on U.S. stock exchanges. Today there are only 3,671. Easy access to venture, growth and private-equity capital means that companies no longer need to pursue an initial public offering to fund growth or access liquidity," the WSJ wrote about 3 years ago.

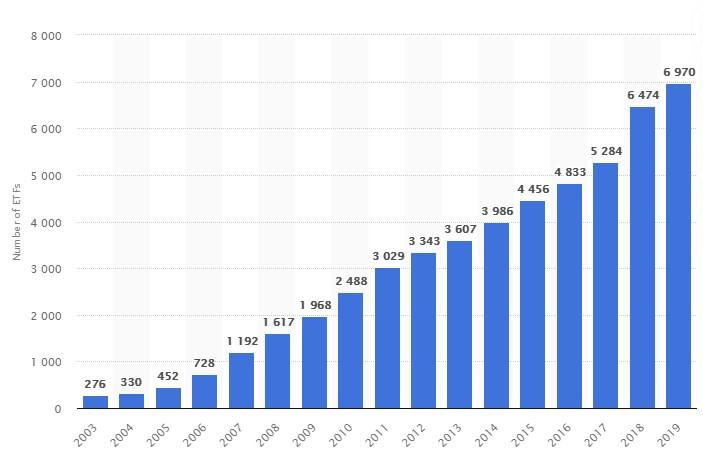

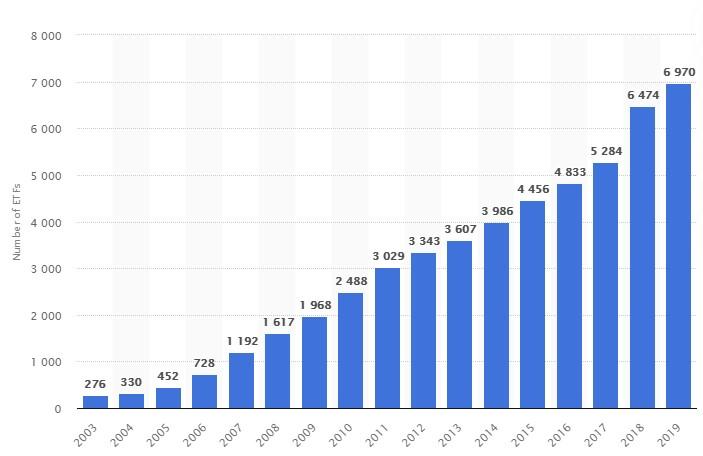

Since then, the number has continued to decline. Yesterday on CNBC, it was reported that there are now less than 3,000 public listings. But there's now more than 7,000 ETFs globally.

Number of ETFs worldwide from 2003 to 2019 (Statista)

We have often discussed the liquidity crisis that could be created from passive investing in ETFs as their popularity grows. Additionally, the use of ETFs as trading vehicles instead could wind up distorting the true price of the underlying stocks held within them.

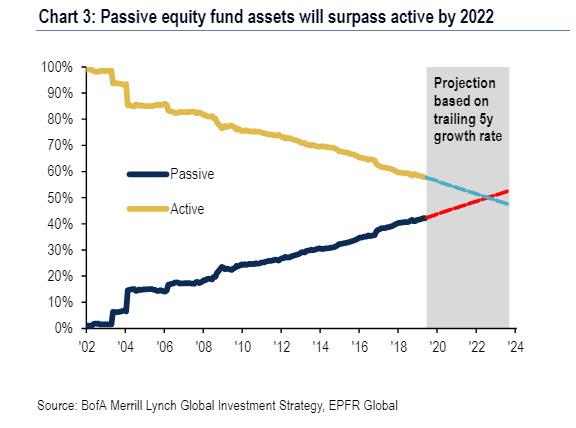

Late last year we noted that passive funds had surpassed active funds thanks to the Fed basically making active investing obsolete. Retail masses followed this lead, which has spurred the demand for ETFs that have allowed them to continue to pop up at an alarming rate.

Recall, back in September of 2019, Michael Burry had claimed that "Passive investments such as index funds and exchange-traded funds are inflating stock and bond prices in a similar way that collateralized debt obligations did for subprime mortgages more than 10 years ago."

He continued: “Like most bubbles, the longer it goes on, the worse the crash will be. This is very much like the bubble in synthetic asset-backed CDOs before the Great Financial Crisis in that price-setting in that market was not done by fundamental security-level analysis, but by massive capital flows based on Nobel-approved models of risk that proved to be untrue.”

In case anyone has wondered just how long it has gone on, the widening delta between listed companies and global ETFs gives an indication of exactly how distorted things have become.

For years, the website RobinTrack.net has been doing a great job of mining RobinHood's data to provide raw data and a visualization of which stocks the users of the retail brokerage have been holding and disposing of on a daily basis.

RobinTrack.net has been a wonderful way to keep an eye on exactly what stocks the bagholder crowd have been rushing into on a daily basis, providing insight into the hysteria of retail daytraders, allowing hedge funds to likely frontrun the data and providing opportunities for short sellers looking for ideas.

But those days appear to be all but over.

On Friday, CNBC reported that the brokerage will no longer display how many of its users hold a certain stock. In addition it is going to be taking down its public API data that allows other sites, like RobinTrack.net, to source its data for visualization and analysis purposes.

"The data has been used to show booms in retail stocks," a CNBC report said on Friday. "You guys know RobinTrack well. A lot of financial news outlets use it for reporting, including CNBC."

Robinhood has said in a statement that even thought it is restricting third party access to its API data, it still has "many other tools" that its users can offer.

"Trends and data are often misconstrued and misunderstood," Robinhood said. "The majority of its users" are buy and hold users, not daytraders, the brokerage said.

Yeah, right. Aside from the PR spin of trying to position itself as a serious brokerage and not a casino app for unemployed daytraders, we're guessing there is another angle to Robinhood removing this data: if you want it in the future, you're going to have to pay.

It was about a year ago when we showed a snapshot of the outrages wealth imbalance in the US with the help of just one metric: as of Aug 2019, Wall Street (US private sector financial assets) was 5.5x the size of Main Street (US GDP), and as BofA's Michael Hartnett pointed out, between 1950 & 2000 the norm was 2.5-3.5x. His conclusion, as recent events have sadly confirmed "Wall Street is now "too big to fail"."

Well fast forward one global pandemic and one unprecedented bailout later, which none other than Hartnett himself framed in the best possible way as follows...

"The monetary and the fiscal stimulus in terms of the announcements thus far, it comes to $20 trillion, $8 trillion of monetary stimulus and $12 trillion of fiscal stimulus. And that number is - it's a little over 20% of global GDP. So it's just astonishing and breathtaking and you have to sort of pinch yourself sometimes to sort of realize that it's actually happening."

... when in his latest Flows and Liquidity report, the BofA Chief Investment Officer provided an update on this most critical metric and it's a doozy.

Dubbing it the "Nihilistic Bull", Hartnett describes the current market as the consequence of a decade-long backdrop of Maximum Liquidity & Minimal Growth still Maximum Bullish, and more importantly, it has led to the value of US financial assets (Wall Street) now hitting an all time high 6.2X size of GDP (Main Street). In other words, not only is Wall Street now "even bigger to fail", but in its attempt to "fix" inequality, the Fed has made it greater than ever, and the now daily violence on America's streets is the most immediate consequence... if only those people protesting knew that they should target their anger not at the Capitol but the Marriner Eccles building.

Going back to the chart above, and the market that spawned it, Hartnett writes that "nothing matters but liquidity...GDP loss of $10tn & US claims 53mn numbed by $21tn policy stimulus, $2bn per hour central bank asset purchases." Furthermore, according to the BofA credit strategist, "the structural view on low yields now shared by all...doesn’t mean to say it is wrong...but it’s inciting a bubble" which is why Hartnett is now confident that the scramble into all asset will not end until the S&P is at 4000, gold $3000, and oil $60, all of which are "probably inconsistent with 0% Treasury yields."

And while not directly caused by it, it's worth recalling that the top 5 stocks are now a record 23% og the S&P500, surpassing dramatically the tech bubble peak:

And in the latest indication of just how long in the tooth the current bubble has become, BofA is now recycling the worst puns of 2018 and 2019, to wit:

I’m so bearish, I’m bullish: Minimal Growth = Maximum Liquidity = Maximum Bullish; narrative of 2010s hardens in 2020 as massive Wall St recovery coincides with Main St recession.

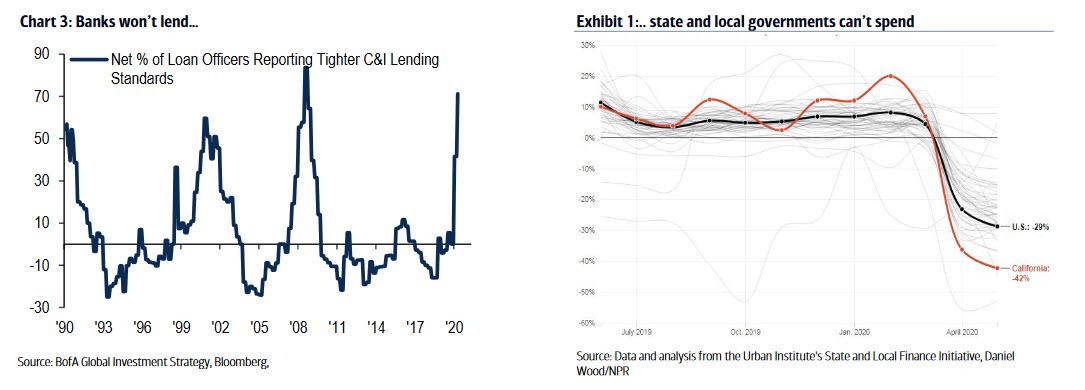

Meanwhile, as the market is stuck in the biggest bubble every, the economy is disintegrating, as banks refuse to lend (as discussed extensively here), while states can't spend, to wit:

Banks won’t lend: 71% of loan officers reported tighter bank lending standards in Q2, the tightest since Q4 ’08.

State & local governments can’t spend: state tax revenues down 37% YoY in New York, down 42% in California, down 53% in Oregon (Exhibit 1); US state & municipal shortfalls could be >$1tn worse-case in 2020 as no back-to-school, no back-to-office, no back-to-revenue.

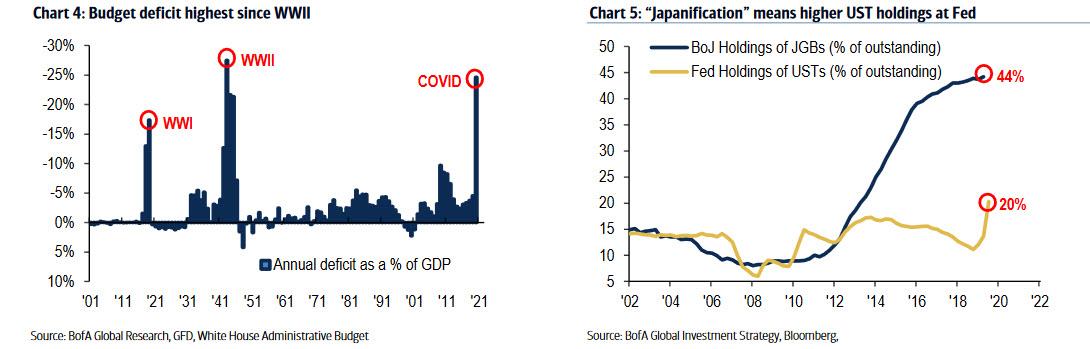

All of this is of course happening as gold is exploding to daily all time highs as helicopter money is off the charts and deficits soaring: "U.S. federal budget deficit @ 25% of GDP if Phase IV fiscal stimulus >$1tn, highest since 1943 WWII peak of 27.5%."

Meanwhile, as even Goldman notes, the Dollar's reserve status is on borrowed time due to a tsunami of printing and debasing: as Hartnett writes, the US debt & deficits to be financed by:

Fed balance sheet (“Japanification” means higher UST holdings at Fed – Chart 5), and

Debasement of US dollar; big inflection points in US dollar always harbinger of leadership change (1971 = Stagflation, 1980 = Disinflation, 2001 = Globalization, 2020 = Inflation to solve Inequality).

What does all of this mean for markets? Three things - the "summer dip" Hartnett expected may not be coming after all, but 2020 will be the "big top ", and while 2020 is the megabull unleashed by central banks, 2021 will be the bear:

Summer dip: late-summer dip (SPX to 3050) thus far wrong but “air pocket” risk grows post +ve July payroll & Phase IV fiscal stimulus; Turkish lira at all-time low = 1st sign capital flow dislocations (as JPY approached 100); lower government yields bullish until credit spreads widen

Big top: 2020 risk asset peak most likely at time of vaccine, full capitulation by bears, higher interest rates; history of great bear market rallies predicts SPX 3300-3600 top between Aug-Jan; liquidity driving Wall St overshoots until weaker dollar/wider credit spreads signal credit event or fiscal stimulus/higher yields signal recovery.

His conclusion: "2020 = Bull; 2021 = Bear: bigger government, smaller world, US dollar debasement...big picture themes of 2021...buy volatility & inflation assets."

With more than 3,000 Beirut families now homeless, and more than 150 have officially been declared death as the search for remains over the massive blast site continues, Lebanese President Michel Aoun said Friday that an official government probe would look into the "possibility of external interference", including the possibility that the explosion was triggered by a rocket or a bomb.

"The cause has not been determined yet. There is a possibility of external interference through a rocket or bomb or other act,” President Michel Aoun said in comments carried by local media and confirmed by his office, per Reuters.

Meanwhile, thousands of Beirutis took to the streets last night to protest the government's apparent incompetence. Some hurled stones at police while others mourned the descent into anarchy.

The small crowd, some hurling stones, marked a return to the kind of protests that had become a feature of life in Beirut, as Lebanese watched their savings evaporate and currency disintegrate, while government decision-making floundered.

“There is no way we can rebuild this house. Where is the state?” Tony Abdou, an unemployed 60-year-old.

His family home is in Gemmayze, a district that lies a few hundred metres from the port warehouses where 2,750 tonnes of highly explosive ammonium nitrate was stored for years, a ticking time bomb near a densely populated area.

A security source and local media previously said the fire that caused the blast was ignited by warehouse welding work.

Lebanon has promised a full investiation, and 16 people have already been arrested. But many fear that those taken into custody are merely scapegoats for government incompetence.

The government has promised a full investigation. State news agency NNA said 16 people were taken into custody.

But for many Lebanese, the explosion was symptomatic of years of neglect by the authorities while corruption thrived.

Officials have said the blast, whose seismic impact was recorded hundreds of miles (kilometres) away, might have caused losses amounting to $15 billion - a bill the country cannot pay when it has already defaulted on its mountain of national debt, exceeding 150% of economic output, and talks about a lifeline from the International Monetary Fund have stalled.

Theories that the explosion was precipitated by a missile or a bomb have been summarily dismissed, due to both a purported preponderance of evidence to the contrary (video of the scene clearly shows a fire and several explosions in the warehouse precipitating the explosion), and the readiness of international terror groups and foreign governments to deny responsibility for the attack. But there's still so much left unknown, and Lebanon's apparent disinterest in pursuing the Russian businessman whose seized cache of ammonium nitrate caused the explosion has led to more questions.

To be sure, negligence, or a tragic accident, would also be examined as probable causes. Reuters reported, citing anonymous sources close to the Lebanese government, that an initial probe has blamed negligence pertaining to the storage of the explosive material.

But the US has previously said it has not ruled out an attack. Israel, which has fought several wars with Lebanon, has also previously denied it had any role.

As we explained earlier this week, a 2,500-ton cache of ultravolatile ammonium nitrate had been stored in a waterfront warehouse by the Lebanese government after it was seized from a foreign ship back in 2013. For years, several port authorities (some of whom are now under house arrest as the government starts its investigation/hunt for a scapegoat) reportedly warned the government about the dangers associated with the chemical cash, and urged them to find a way to dispose of it - even if it meant handing it out to Lebanese farmers to spread over their crops.

And the almost unbelievable story of how the explosive substance got there has emerged. It's centered on a derelict and leaking vessel leased by a Russian businessman living in Cyprus. In 2013 the man identified as Igor Grechushkin, was paid $1 million to transport the high-density ammonium nitrate to the port of Beira in Mozambique. That's when the ship, named the Rhosus, left the Black Sea port of Batumi, in Georgia.

But amid mutiny by an unpaid crew, a hole in the ship's hull, and constant legal troubles, the ship never made it. Instead, it entered the port of Beirut where it was impounded by Lebanese authorities over severe safety issues, during which time the ammonium nitrate was transferred off, and the largely Ukrainian crew was prevented from disembarking, leading to a brief international crisis among countries as Kiev sought the safe return of its nationals.

Meanwhile, Igor Grechushkin - believed to still be living in Cyprus - reportedly simply abandoned the dangerously subpar vessel he leased, as well as its crew, never to be heard from again.

The ammonium nitrate was supposed to be auctioned off, but this never happened. Apparently exasperated customs and dock officials even suggested Lebanese farmers could simply spread it across their fields for a good crop yield. But not even this simple solution was heeded, nor proposals to give it to the Lebanese Army.

[…]

Meanwhile, the fate of the man originally at the center of the saga, whose decision to simply abandon the leaky ammonium nitrate laden ship in the first place, remains somewhat of a mystery and is now largely being overlooked in international media reports. Strangely, it doesn't even appear that Lebanese law enforcement is eager to talk to him just yet.

Cypriot media is saying Igor Grechushkin is not a Cypriot passport holder but is indeed residing in the EU country. Local authorities have indicated they are ready to bring him in for questioning, but they haven't received a request from either Lebanese authorities or Interpol. Cypriot police spokesman Christos Andreou announced Thursday: “We have already contacted Interpol Beirut and expressed our readiness to provide them with any assistance they need, if and when our assistance is requested.”

An initial government "probe" blamed negligence related to storage of the explosive material. And with more Beirutis taking to the streets to demand an answer, we're curious to see how the government handles the process as it seeks to preserve what little credibility it has left.

The Swiss population owns 920 tonnes in private gold, next to 1,040 tonnes in official gold reserves. In total, Switzerland likely has the highest amount of gold per capita in the world. This article is part of a series in which we examine how much private gold is located in major economies—information that can be decisive for a monetary reset.

In my previous article, “Europe Has Been Preparing a Global Gold Standard Since the 1970s,” we saw that the world is possibly heading towards a new international monetary system that incorporates gold. In the article I exposed that European central banks have sold monetary gold from the 1990s until 2008 to equalize reserves internationally. The same central banks are currently promoting gold as “the ultimate store of value,” protection against “high inflation” and the possibility “the system collapses.” In case we will return to an international gold standard the distribution of gold is essential, which is why I study the whereabouts of all above ground reserves.

I showed that since 1971 official and private gold reserves have been distributed more evenly across the world on a relative basis. In today’s article the spotlight is on Switzerland.

The main motivation for the Swiss to save in physical gold is as a long-term investment (53%), followed by security reasons (39%), and financial stability (34%). The study shows that in 2019 the Swiss invested 1.42 billion CHF in gold, which equals to a gold savings rate of 11.6%

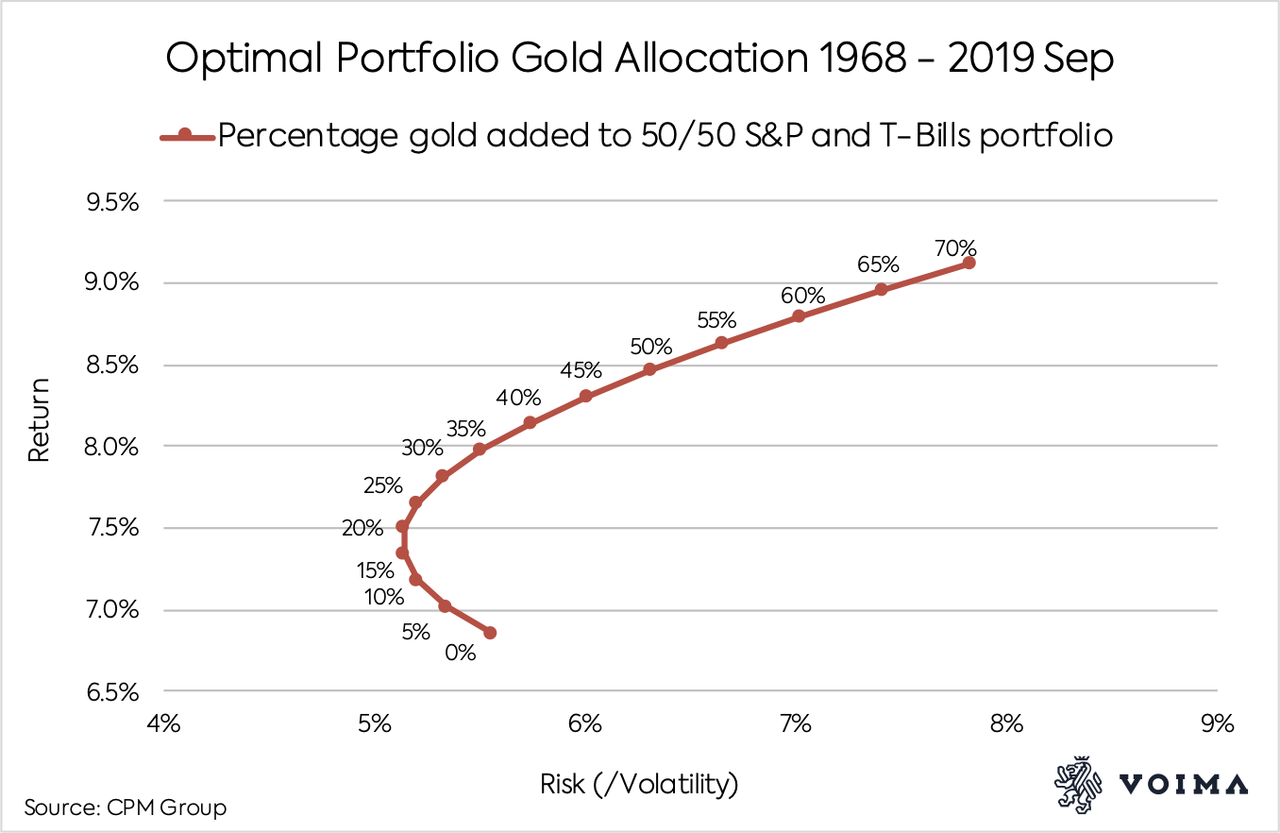

Switzerland's gold savings rate matches what several studies suggest as the best long-term allocation of gold. According to calculations by CPM Group the optimal risk-return balance of an investment portfolio is reached when it includes 20% of gold (next to an equal share of stocks and bonds). But of course timing, risk appetite, and portfolio size can change the optimal allocation.

In total, the Swiss population owns 920 tonnes in private gold. Note, this does not include all the private gold that is stored in Switzerland. Switzerland is known for having the largest precious metals refining capacity in the world, and there are many vaults located in Switzerland that store gold for residents from abroad.

My estimates for private gold ownership in different countries for 2019:

Hopefully more surveys will be conducted so we can get a better view on the distribution of private gold.

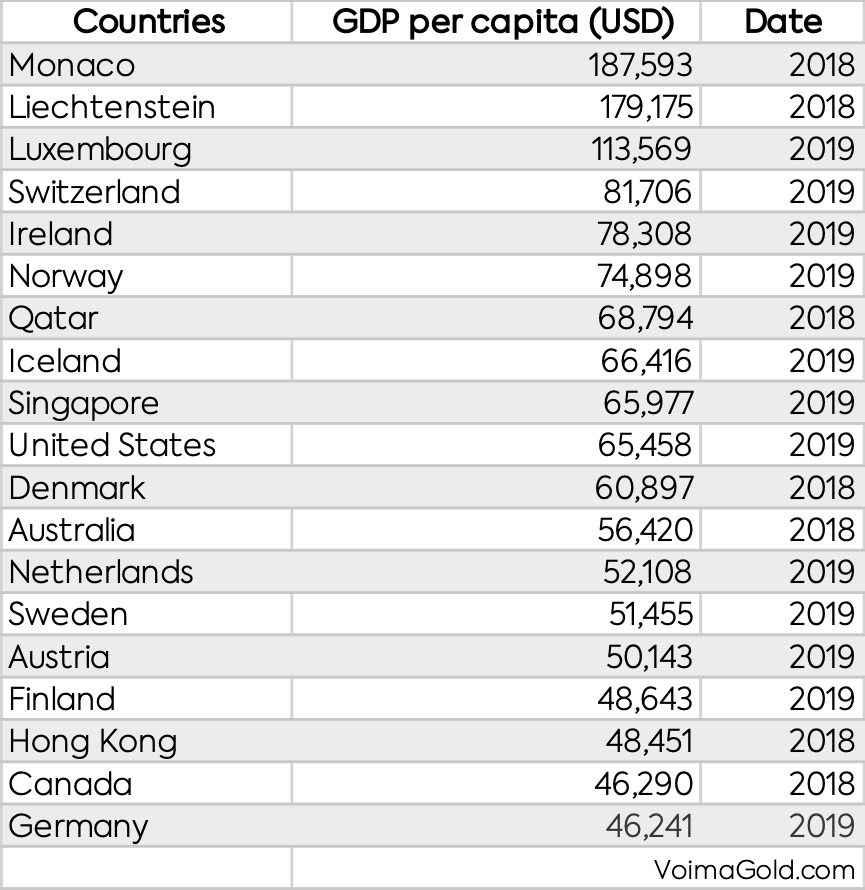

Next to the private gold hoard of 920 tonnes, the central bank in Switzerland holds 1,040 tonnes in official gold reserves. Combined, the Swiss own 1,960 tonnes, which is 231 grams per capita. This is higher than “total gold grams per capita” in India, China, France and even Germany. However, relative to “GDP per capita,” it’s in line with the global mean.

For all the countries I have data of, the amount of gold owned by citizens, directly or via their central bank, approximately equals their economic income (GDP per capita). At a gold price of $10,000 U.S. dollars per troy ounce, that is. We will save the number crunching and economic analysis for a future article.

Likely, Switzerland has the highest amount of “total gold grams per capita” in the world. As, there is a correlation between GDP per capita and private gold ownership, and Switzerland ranks very high on the list of GDP per capita.

Only small states with insignificant official gold reserves, like Monaco and Liechtenstein, have a higher GDP per capita. So, it's likely the Swiss have the highest amount of gold per capita.

H/t Mark Valek. All GDP data used in this article is pre-COVID.

{kind=link}