For the first time, companies including Nissan Motor Co. (7201) are building products abroad to ship home as a stronger yen, aging workforce and improved skills overseas erode a century-old mantra that what’s sold in Japan should be made there.

Nissan’s decision to import foreign-made vehicles in 2010 paved the way for some of Japan’s biggest companies, including cosmetics company Shiseido Co. (4911) and electronics maker Toshiba Corp. (6502) Shipments home from Japanese producers’ overseas plants have more than doubled in a decade to a record, including a 31 percent jump in the past two years, compared with a 61 percent gain in total importsover the 10 years, government data show.

“Nissan’s decision was epochal,” said Masato Sase, an auto-industry analyst and partner at Deloitte Tohmatsu Consulting Co. in Tokyo. “Before then there was a tacit assumption that cars sold in Japan would be made in Japan.”

The shift reflects one of the biggest departures from an industrial strategy begun by the Meiji leaders who ousted the last shogun in 1868 and set up western-style factories. A “made by Japan” model, where manufacturers base operations with less regard to nationalism, may boost corporate competitiveness at the cost of jobs in the world’s third-biggest economy, deepening deflation pressures.

“People see the sale of cars made abroad as a sign of the times, as globalization,” said Shiro Kakinuma, a salesman at Taiyo Nissan Auto Sales Co.’s Shibaura Chuo showroom in Tokyo, which offers the Thai-made Nissan March subcompact. “When the new March came out there were some articles questioning the quality of a car made in a developing country. Not anymore.”

system developers know, the process of building automated trading systems is complex and filled with biases. A machine is not necessarily a physical mechanical machine. It can be a virtual machine, electrical machine, or in our case, software-based logical trading machine. System trading is the process of building and implementation of algorithm-based systems that execute trades automatically. While many associate this with machine intelligence, only the execution is fully automated.

Don't allow the low volatility in August to make you complacent.

Most of the world is on vacation, even in the hard working United States. Kids are off from school, some hedge funds even shut down in August. Those who aren't on vacation, use this as a quiet time for planning so they are ready for a big September.

BofA strategists Arjun Mehra and Cheryl Rowan have a warning more precisely aimed at the stockmarket. In a note to clients entitled Code Red, Mehra and Rowan claim there is "limited upside from here" and the "risk of a sell-off is high."

Peter from Ireland wrote in asking me to do a piece on liquidity on

the forex market. Although the market trades 5 trillion dollars per day

in volume, even forex traders face limitations in how much volume they

can push through in a short period of time.

A Zero Hedge article on the Reuters 3000 platform outage

cited some interesting statistics for the currency markets and where

the trading actually occurs. Although I was familiar with Reuters and

EBS previously, the Dow Jones article was the first place where I've

seen volume statistics published. Apparently Reuters, the biggest

platform, trades approximately $130 billion dollars in volume per day.

That's an astronomical amount of money. Intuition makes it feel like hitting

the ceiling on executing large transactions might be a problem for only

the biggest institutions. Let's take a look at where we might expect to

run into problems.

When I went through broker training at FXCM,

the team leader cited the EUR and USD as being involved with 60% of all

forex trading volume. That number does not imply how much volume occurs

in the specific EURUSD pair. Also, that that was seven years ago. I dug

around looking for more up to date numbers. Forex trading volume is

notoriously hard to track due to it being an over the counter market.

The best proxy that I know of is the FX futures market.

The CME publishes FX futures contracts volume

(page 16), which I used to estimate the proportion of the EURUSD pair

in relation to all traded volume. FX futures contracts, like their spot

counterparts, are all denominated in different currencies. Except for

the e-mini and e-micro contracts, which resemble the mini lots of retail

forex trading, the contract size is roughly $150,000. I'm counting

contracts rather than actual notional value to speed up the

calculations. You can double check my calculations by downloading this spreadsheet. The EURUSD pair represents 33% of all forex trading volume based on my rough estimates.

The

EURUSD value traded per day on Reuters is 33% of $130 billion, which is

43.33 billion. The average trading consists of 1,440 minutes per day.

43.33 billion trades per day / 1,440 minutes per day yields an average

traded amount of $30,092,592 traded per minute. Again, this is a huge

number.

Everyone in forex trades on margin. Institutions

traditionally keep their margin very low. Assume that 3:1 is the norm

for the big players. That means that the actual funding in the account

only needs to be $10 million dollars (30/3). That's a lot of money, but

that is chump change by institutional standards. That's more on par with

a wet behind the ears CTA that launched within the past few years. This

scenario is for the most liquid currency pair on the largest currency

trading platform in the world.

Dropping down to the retail scenario, the numbers involved get much, much smaller. The Financial Times cites FXCM's average trading volume

as $55 billion per day. This is tens of multiples higher than an

average broker's volume. I picked it because it's the highest that I

know of and I wanted to demonstrate a big scenario. 33% of $55 billion

is $18.15 billion traded on the EURUSD. $18.15 billion / 1,440 minutes

per day is $12.6 million traded per minute.

Retail traders

leverage far higher than institutions. Again, let's be kind and make the

assumption that the average retail trader employes 15:1 leverage on the

account (hint: it's much higher). $12.6 million / 15 implies that it

only takes an account balance of $840,277 to trade all of the expected

trading volume in an average minute. One trader is unlikely to have a

balance that large, but a segment of a broker's customers most certainly

do.

The fragmentation of the market combined with leverage makes

it strikingly easy for a group of traders to suck up all of the

liquidity available on a given platform. Even though trillions are

available across the broader market, the broker or platform where a

trader participates is substantially more limited. The scenarios modeled

use the EURUSD, the most liquid pair in the world. Liquidity gets

exponentially worse when examining exotics or cross currencies. The

volumes are far lower, but the available leverage and account balances

remain the same.

When too many traders buy the same EA, all orders

fire off at the same time. Blockbuster EAs easily reach the combined

account equity floor where demand overwhelms supply. Finer details like

all of the supply is being one sided make the situation all the worse.

Based on an overwhelming bearish negative bias on the euro (FXE) from multiple sources (individuals, banks,

analysts, and fund managers) we believe selling the euro on any run-up is a

viable strategy.

The euro climbed to a fresh seven-week high against the dollar on Thursday on news Spain is negotiating with the euro zone over conditions for international aid to bring down its borrowing costs though the country has not made a final decision to request a bailout.

Earlier, the single currency set a fresh seven-week high against the U.S. dollar after Federal Reserve minutes hinted at more monetary easing in the U.S., while French and German business activity surveys were not as bad as feared.

In today's volatile business environment, organisations must be ready to reconfigure their strategic priorities at speed, and with certainty.

Crucially, instead of basing major business decisions on intuition, they need to mine the data and information at their disposal to drive rapid decision making.

This is why analytics - the use of data, statistical and quantitative analysis, explanatory and predictive models - has moved centre-stage.

According to market research firm IDC, the market for business analytics software grew 14 percent in 2011 and will hit US$50.7bn by 2016.

Of course, analytics itself is nothing new.

Organisations such as Google, Tesco and Caesars Entertainment are well recognised for their ability to predict market trends, customer behaviours and workforce staffing requirements and turn these into top-line growth and/or bottom line savings.

But for the many other businesses now seeking to take advantage of analytics, there continues to be a lack of clarity around certain fundamental questions.

What is analytics? How can it propel and improve an organisation's competitive positioning or effectiveness?

What does it mean to truly become an analytical organisation? And how does an organisation set out on this critical journey?

Although the development of analytical capabilities and capacity is obviously important, a focus on data, methods and technology alone will not magically deliver the insights needed for competitive edge.

UBS AG (UBS) is starting a unit aimed at attracting clients among quantitative hedge funds, combining services from its prime brokerage and direct-execution trading businesses.

Scott Stickler in New York will be global head of the operation, called UBS Quant HQ. Strategies across equities, options and futures will be supported with fixed income and foreign exchange to be added later, he said. The business targets startups and established funds with long-short or hedged strategies and those focused on arbitrage.

Investment firms formed as a result of regulations to curb risk-taking within banks are looking for help with technology consulting services, trading and financing, according to Stickler, who was hired in July 2011. The unit began working with more than a dozen hedge-fund clients in the second quarter as it prepared for the Quant HQ introduction, he said.

“One of the trends we’re seeing is a number of startups, folks coming out of big banks because of the Volcker rule and starting their own hedge funds,” Stickler said in a phone interview. “Clients are coming to us who wanted us to be in this business and who want to be able to take advantage of our global presence and our counterparty safety, stock-loan and execution capabilities.”

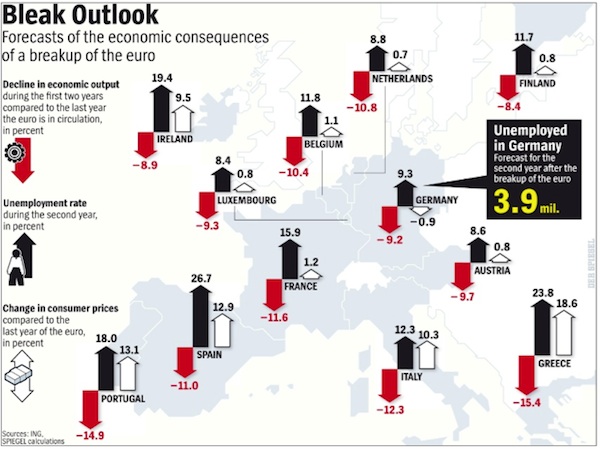

Banks, companies and investors are preparing themselves for a collapse of the euro. Cross-border bank lending is falling, asset managers are shunning Europe and money is flowing into German real estate and bonds. The euro remains stable against the dollar because America has debt problems too. But unlike the euro, the dollar's structure isn't in doubt.

Otmar Issing is looking a bit tired. The former chief economist at the European Central Bank (ECB) is sitting on a barstool in a room adjoining the Frankfurt Stock Exchange. He resembles a father whose troubled teenager has fallen in with the wrong crowd. Issing is just about to explain again all the things that have gone wrong with the euro, and why the current, as yet unsuccessful efforts to save the European common currency are cause for grave concern.

He begins with an anecdote. "Dear Otmar, congratulations on an impossible job." That's what the late Nobel Prize-winning American economist Milton Friedman wrote to him when Issing became a member of the ECB Executive Board. Right from the start, Friedman didn't believe that the new currency would survive. Issing at the time saw the euro as an "experiment" that was nevertheless worth fighting for.

Fourteen years later, Issing is still fighting long after he's gone into retirement. But just next door on the stock exchange floor, and in other financial centers around the world, apparently a great many people believe that Friedman's prophecy will soon be fulfilled.

Banks, investors and companies are bracing themselves for the possibility that the euro will break up -- and are thus increasing the likelihood that precisely this will happen.

There is increasing anxiety, particularly because politicians have not managed to solve the problems. Despite all their efforts, the situation in Greece appears hopeless. Spain is in trouble and, to make matters worse, Germany's Constitutional Court will decide in September whether the European Stability Mechanism (ESM) is even compatible with the German constitution.

There's a growing sense of resentment in both lending and borrowing countries -- and in the nations that could soon join their ranks. German politicians such as Bavarian Finance Minister Markus Söder of the conservative Christian Social Union (CSU) are openly calling for Greece to be thrown out of the euro zone. Meanwhile the the leader of Germany's opposition center-left Social Democrats (SPD), Sigmar Gabriel, is urging the euro countries to share liability for the debts.

On the financial markets, the political wrangling over the right way to resolve the crisis has accomplished primarily one thing: it has fueled fears of a collapse of the euro.

AFTER a promising May and June, Steffen Knoop has seen his sales dip by 30%. His small Hamburg-based company, Wascut, sells cooling and cleaning oils for big machines, including those that make cars. “I have a pretty good window on the economy,” he says. Mr Knoop wonders whether the dip is caused by people taking extra long summer holidays or something more serious. Others with a broader and more long-term view of the economic landscape are asking the same question.

Building forex trading systems is the reason that this company

exists. Nearly every one of our clients aspires to be a fully automated

trader.

The percentage of clients that succeed over the long run,

however, is incredibly small. I don't think that is a big secret. If

that is news to you, allow me to be clear. The chances of developing a

successful expert advisor over the long term are minimal.

The

inevitable next question from new clients is an attempt to pick my brain

for some features common to successful systems traders. I decided to

outline the traits common to this rare breed and some of the challenges

that they encounter.

Traits of a successful EA developer

Expert

advisor developers that succeed are either incredibly bright

(engineers, Ph.D. holders, etc) or dumber than a sack of rocks. No

middle ground exists. A friend/client told me about an experiment that

struck me as telling. If you put a mouse in a cage where cheese appears

40% of the time on one side of the box and 60% of the time on the other,

all mice eventually pick the side that "wins" 60% of the time. The mice

stop guessing and go with what works more often than not.

That's

my theory for why the "intellectually challenged" crowd seems

disproportionately likely to profit from trading. They see right through

the noise to pick out a simple observation that wins more than it

loses. Holy grail systems certainly do not come from this group. That's

not honestly not the goal. It's about eating cheese more often than

going hungry.

The brainy crowd benefits from a heavy dependence on

analysis. Ideas usually stem from pet theories, many of which look like

the crackpot variety on first glance. The theory shifts and twists as

market tests reveal strengths and weaknesses. Logical conclusions

instill a robustness and variety into the system. Interestingly, the

approach to testing and verifying the systems follows the opposite path

of most developers. The ideas tend to get simpler with time rather than

more complex.

Emotion does not play a large role in the rationale

for developing an expert advisor. Again, the reasons are usually

logical. Examples like "I've been trading this system for 20 years and I

need to automate it" or "I came up with a way to accurately predict

market direction."

It may sound a bit zen, but the systems that

make money are the ones that do not set their primary goals as making

money. Making money is a totally open ended goal. The potential

variables know no limit. The lack of constraint encourages would be EA

traders to shoot off on tangents. Unless the wild ride accidentally

leads to the pot of gold at the end of the rainbow, they will fail. The

limitless bounds make it impossible to measure any progress.

In

that same vein, the journey is as important as the destination. Many

traders pay lip service to limiting drawdown. Few are able to

effectively rein in drawdown, especially within the context of an expert

advisor. To a certain extent, limiting drawdown is not possible. My

experience with money management makes it clear how much wandering a

return can make, even with a heavy advantage.

The easiest way to

limit drawdowns is to fight against severe losses. The goal is to obsess

over risk and reduce it to the lowest possible point. I want to

emphasize this point carefully. Risk always exists. The market

chaotically switches from deep slumber to extreme violence. No amount of

system engineering eliminates or alters the structure of the market.

The most effective way to handle risk that I see is not to prevent it

from happening (not possible), but rather how to react when risk

eventually flares up.

Approaching system design as a process

rather than a destination also encourages global thinking. My old boss

would describe it as the 40,000 foot perspective. When a forex trader,

for example, emphasizes a system's percent accuracy, it typically comes

at the expense of exiting at a better point in the market. A need to win

slightly more often actually drags the system away from its optimal

performance. A process oriented design watches how changes in the entry

method affects the exit efficiency. Clever money management removes the emphasis from entry and exit methods.

Designing

these systems takes hundreds of man hours or results from more than a

decade of experience. Emotion will certainly enter the equation at some

point. The real question is not how to remove it. It is how to

appropriately channel it.

Designing an expert advisor quickly

takes on the characteristic of an obsessive hobby. If the system's

success is measured in quantities of dollars, the emotional roller

coaster rises in tune with the account balance. A more appropriate use

for the emotion is to take heart in the system working correctly, not

profitably. Ideally, correctly also means profitably. They are not the

same thing, however. Drawdown and unlucky losing streaks are an inherent

part of trading. Gaining satisfaction from the trade behaving as

designed rather than as desired makes your emotional well being far less

dependent on market performance.

I have been running this company

for nearly five years and literally spoken with thousands of traders

over that time. In spite of that overwhelming number, I still have yet

to speak with anyone that traded a commercial EA successfully for more

than a few months.

The successful traders that I know personally

all developed their systems and strategies on their own. Maybe that

reflects on the abysmal quality of expert advisors for sale on the

internet. Maybe it reflects on not-so-expert trading coaches, or perhaps

genuine trading coaches and hapless traders unable to follow sound

advice. I suspect it's a little of everything. Regardless of the

problems, the take away point is that the person doing the succeeding is

also the person doing the developing. They take control of the

experience from the beginning and lead it into a successful outcome.

Systems trading is not a process where you buy your way to success or

follow like a sheep to green pasture. You must earn it.

Challenges of using a winning expert advisor

The

path to achieving a profitable strategy on paper is a long, hard road.

The switch from theoretical turns to live trading is a challenge in its

own right. Backtests spit out instantaneous results. Traders see

something like a 20% annual return, then mentally prepare themselves for

the steady accumulation of funds.

That kind of trajectory puts a

number in the trader's mind that is terribly misleading in real life.

Steady annual growth of 20% suggests a constant return of 1.67% (20/12).

That number 1.67% is a hiccup in a trading account. Many forex traders

risk more than that amount on a single transaction. Factoring in the

inevitable drawdown or periods of loss, the market makes it impossible

to distinguish whether or not the expert advisor is behaving correctly

or if it is falling apart.

Uncertainty in the face of risk makes

any normal person panic. At the very least, it instills a degree of

anxiety over the future. The moment that the machine stops churning out

profits is the moment where doubt enters the picture. Doubt feeds on

itself, which leads to changing the trading plan in midstream.

I

can tell you from experience that the transition from research to

execution is huge. A learning curve exists, like with everything. I

learn to cope by taking the confidence that I gain through the same debugging techniques

used in testing. The same techniques work for comparing live results to

backtested results. Does the backtest over the same time period as my

real trading match the actual performance? If so, then all is well. If

not, it at least gives me as the developer an opportunity to think about

specific problems. Execution or forex broker manipulation

can cause problems. More often that not, however, is some flaw in the

strategy design or code. Developing a methodical, reason based process

helps calm nerves and to stay focused. The alternative is a general,

undefined worry.

Exotic bar types, as NinjaTrader likes to call them, create unique challenges when backtesting strategies. The primary problems is that the backtests are usually bogus. The trader often has no idea that the profitable backtest calculated from errant data.

Renko

bars form based on the order of incoming ticks to create specific box

sizes. Say, for example, that a trader creates a box size of 5 pips. If

the price rises 5 pips from the close price of the last Renko bar, then

the chart creates a new bar 5 pips tall. Every 5 pip increment, whether

up or down, draws a new Renko bar.

Using increments that easily

fall within normal market gaps creates the false impression of

trade-able prices where none existed. Minor news events frequently

result in 5-10 pip market gaps. In the case of the 10 pip gap, a box

size of 5 pips creates 2 Renko bars. The two bars do nothing to

communicate the fact that the prices never existed. Their presence

merely indicates the direction of a move and eliminates the idea of time

altogether. Time, or more specifically the absence of it, strikes me as

rather important.

Small box sizes more commonly lead to questions about wildly inaccurate backtests. I received two questions last week inquiring why NinjaTrader showed $19,000 returns in a backtest, but the same forward test lost nearly an identical amount.

The backtests rely on a selected data set to generate the Renko bars used for testing. Users nearly always overlook the data source option in NinjaTrader.

It defaults to one minute charts. One tick bid is the only type of data

that will form perfectly accurate charts. Any other increment risks

creating Renko bars that never existed.

Change your backtest settings to use not only Renko charts, but also Bid data.

Take

an extreme example of one minute chart data drawing Renko bars with a 3

pip box size. Say that the over-all height of the bar is 10 pips, the

low is 1 pip from the open and the M1 bar closes 8 pips higher. How many

Renko boxes does the chart need to draw? The correct answer is that

there is no way of knowing.

Examples:

The market goes down 1 pip, then up 10 pips and settles at the close price. This draws 3 total box with one box in progress.

The

market goes down 1 pip, then up 3 pips, then down 3 pips, then up 10

pips. This draws 5 boxes total with one box in progress.

The

market does down 1 pip, then up 3 pips, then down 3 pips, then up 3

pips, then down 3 pips, then up 10 pips. This draws 7 boxes total with

one box in progress.

As you can see, we have no way of

knowing which of the above options is correct, if any of them are

correct at all. Summarizing price over time inevitably papers over what

happens in the middle (information entropy). NinjaTrader has no option but to guess the unknowable.

It's done in good faith, but NinjaTrader is

essentially making up Renko data to cover up gaps in the price data.

When you're running a backtest, the whole point of the exercise is to

eliminate guessing and deliver solid answers.

Most people make the

hand waving assumption that it all averages out in the end. The two

clients asking me this week about why their Renko backtests came

out so screwy, and the reason that I'm writing this post, is that the

hypothetical versus real performance was as different as night from day.

It most certainly does not average out. Rather, it introduces so many

errant points as to make the tests worthless.

Don't make assumptions in your backtest. Get tick data and, if you're using Renko bars, make sure to set the test up properly.

Swiss banks are turning over thousands of employee names to U.S. authorities as they seek leniency for their alleged role in helping American clients evade taxes, according to lawyers representing banking staff.

At least five banks supplied e-mails and telephone records containing as many as 10,000 names to the U.S. Department of Justice, according to estimates by Douglas Hornung, a Geneva- based lawyer representing 40 current and former employees of HSBC Holdings Plc’s Swiss unit,Credit Suisse Group AG (CSGN) and Julius Baer Group Ltd. (BAER) The data handover is illegal, said Alec Reymond, a former president of the Geneva Bar Association, who is representing two Credit Suisse staff members.

“The banks are burning their own people to try and cut deals with the DOJ,” said Hornung. “This violation of personal privacy is unprecedented in the Swiss banking industry.”

Swiss banks want to settle a U.S. tax-evasion probe after the Justice Department indicted Wegelin & Co. on Feb. 2 for allegedly helping customers hide money from the Internal Revenue Service. Credit Suisse, HSBC and Julius Baer, which have said they expect to pay fines to resolve the tax matter, are handing over data to mollify the U.S., according to Hornung.

Credit Suisse said the Swiss government authorized the delivery of staff names and that the “large majority” of employees have nothing to fear. Julius Baer and Zuercher Kantonalbank also said they received authorization. HSBC said it has delivered documents and is cooperating with the U.S.

Europe’s failure twice plunged the world into war. In today’s globalized economic world, Europe’s failure to resolve its financial crisis could plunge the world into economic chaos. This is a global crisis — not a euro-zone crisis — and we must take international action to deal with it. http://www.nytimes.com/2012/08/16/opinion/the-global-not-euro-zone-crisis.html

Peregrine Financial Group Inc. CEO Russ Wasendorf Sr. could face up to 155 years in prison if convicted on all counts, prosecutors said. His attorney didn’t immediately return a phone message Monday, and the date for an arraignment, where Wasendorf will enter a plea, has not been set. Peregrine operated as PFGBest.

Wasendorf, 64, a major player in Chicago’s futures industry, was arrested last month while hospitalized in Iowa City following a failed suicide attempt outside Peregrine’s office in Cedar Falls. Authorities said Wasendorf left a detailed suicide note in which he confessed to a 20-year scheme to commit fraud and embezzle customer funds.

For any PFG Best Customer, in case you have not seen this:

Important Message for Customers of Peregrine Financial Group and Peregrine Asset Management - Updated on August 3, 2012

As you aware, PFG filed for liquidation in a U.S. bankruptcy court in Chicago and the U.S. Trustee appointed Ira Bodenstein to act as trustee for PFG and its assets, including customer property. On July 13, the bankruptcy court authorized the trustee to continue to operate PFG's business for a limited time in order to (among other things) prepare and distribute final customer statements, and record transactions related to customer accounts. At this time, it is not clear how long it will take to complete these processes or when the trustee will be authorized to release any funds to customers.

The trustee has established a website, www.PFGChapter7.com, that contains information about the PFG case. The website was created to assist the trustee in providing information to customers and to receive comments or questions from customers. According to the website, the Trustee has not yet determined whether PFG customers will need to prepare a claim form. Customers are encouraged to visit the site regularly for updates from the Trustee regarding customer claims.

Once triggered on Aug. 1, the dormant system started multiplying stock trades by one thousand, according to the people, who spoke anonymously because the firm hasn’t commented publicly on what caused the error. Knight’s staff looked through eight sets of software before determining what happened, the people said.

Knight, based in Jersey City, New Jersey, hasn’t explained in detail what caused the trading losses, which depleted its capital and led to a $400 million rescue that ceded most of the company to a group of investors led by Jefferies Group Inc. (JEF) The 45-minute delay in shutting down the malfunction has confused some securities professionals, who say that trading programs can typically be disabled instantly.

Investors are losing confidence in the single currency and seeking havens for their cash outside the euro area asEurope’s debt crisis drags on in its third year. That has forced the Swiss National Bank to buy euros to prevent the franc from appreciating, and prompted the Danish central bank to charge for the use of its deposit facility while yields on U.K. two-year notes are less than 0.14 percent.

“Now there are growing signs that the crisis of confidence in the euro zone has assumed a new dimension,” Kressin wrote. “Whereas initially investors fled to the safety of the euro zone’s core, now they are taking their capital out of the euro zone altogether.”

The Swiss central bank’s sales of the euro to rebalance its reserves are “reinforcing” pressure on the single currency, according to Kressin. Its purchases of top-rated Europeangovernment bonds, particularly bunds, are also forcing down yields on those securities, he said.

(Reuters) - U.S. regulators directed five of the country's biggest banks, including Bank of America Corp and Goldman Sachs Group Inc, to develop plans for staving off collapse if they faced serious problems, emphasizing that the banks could not count on government help.

The two-year-old program, which has been largely secret until now, is in addition to the "living wills" the banks crafted to help regulators dismantle them if they actually do fail. It shows how hard regulators are working to ensure that banks have plans for worst-case scenarios and can act rationally in times of distress.

Officials like Lehman Brothers former Chief Executive Dick Fuld have been criticized for having been too hesitant to take bold steps to solve their banks' problems during the financial crisis.

BRUSSELS - Former European Central Bank (ECB) chief economist and German central banker Otmar Issing has warned that the eurozone may split up - another voice in the chorus talking about a Greek exit from the common currency.

"Everything speaks in favour of saving the euro area. How many countries will be able to be part of it in the long term remains to be seen," Issing wrote in his latest book, entitled: "How we save the euro and strengthen Europe."

Alas, August 20 is the out-of-money date. September is irrelevant. Because someone else turned off the spigot. Um, the ECB. Two weeks ago, it stopped accepting Greek government bonds as collateral for its repurchase operations, thus cutting Greek banks off their lifeline. Greece asked for a bridge loan to get through the summer, which the ECB rejected. Greece asked for a delay in repaying the €3.2 billion bond maturing on August 20, which the ECB also rejected though the bond was decomposing on its balance sheet. It would kick Greece into default. And the ECB would be blamed.

But the ECB has a public face, President Mario Draghi. He didn’t want history books pointing at him. So the ECB switched gears. It allowed Greece to sell worthless treasury bills with maturities of three and six months to its own bankrupt and bailed out banks. Under the Emergency Liquidity Assistance (ELA), the banks would hand these T-bills to the Bank of Greece (central bank) as collateral in exchange for real euros, which the banks would then pass to the government. Thus, the Bank of Greece would fund the Greek government.

Precisely what is prohibited under the treaties that govern the ECB and the Eurosystem of central banks. But voila. Out-of-money Greece now prints its own euros! The ECB approved it. The ever so vigilant Bundesbank acquiesced. No one wanted to get blamed for Greece’s default.

I picked up Dark Pools by Scott Paterson on Friday evening and finished Sunday afternoon. That ought to say something for the book's readability. I recommend it to anyone that trades, especially equities traders.

The structure of the stock market is far more complicated than I ever expected. Trading at Interactive Brokers, I always noticed that the execution venue would vary between different acronyms like ISLAND, ARCA and BATS. I knew that they were ECNs, but I never really understood what linked them together.

The stock market is not an exchange in the sense of a centralized location where all transactions occur. It is more like a listing entity where public companies go to list their shares. Actual trading occurs on any network plugged into the system.

The "exchange" is really a complex network of networks with varying degrees of favoritism shown to high volume clients.

Electronic Communication Networks ("ECN") originally started in the mid 1980s with the idealistic goal of eliminating the corrupt practices of the NASDAQ floor specialists and market makers. These guys were notorious (and later heavily fined) for colluding to artificially widen spreads on stocks for their own profits. ECNs would cut out the hated middle man while reducing errors, increasing transparency and dramatically decreasing execution time.

As one can imagine, the ECNs took off rather quickly. Not only did they offer much faster execution, but they were also about 60% cheaper to execute a trade.

They corruption that ECNs sought to eliminate inadvertently replaced one problem with another. Networks looking for liquidity offered trading rebates for limit orders that added orders into the system. The setup, which came to be known as maker-taker, created perverse trading incentives for participants. The more trades executed, the more the profits would add up.

Firms sought to become something like Walmart is to wide screen TVs. The more you sell, the more you make. The liquidity providers started fighting aggressively for inside placement of the spread to facilitate ever more trades.

The system spun out of control in two ways. It created a computing arms race where firms focused on purchasing cutting edge technology that shaves microseconds off of calculation time. Firms with the deepest pockets could literally buy an advantage through their computing hardware over the average Joe.

More importantly, the system itself bred its own corruption. The ECNs grew addicted to the liquidity fees. The more trades that fired off, the more money they made. They naturally started catering to their most important clients.

How they did it, though, is what sickens me as a trader. The ECNs started creating order types that were effectively secret. They allowed high speed firms to jump in line over retail chumps using vanilla limit orders. The ECNs offered colocation access at exorbitant fees to give the machines an edge. They allowed the creation of dark liquidity where some players could literally hide orders for execution while others displayed theirs 100% of the time. It makes a complete mockery of the idea of a level playing field.

Artificial intelligence played a big role in how the algorithms operate. What encouraged me, however, was how Patterson chose to wrap up the book. Many of the funds covered near the end start out as relatively small fish working with various types of AI to build predictive trading systems. Their initial results appear encouraging.

One of our biggest projects here is to use various models of fractal markets to build an automated trading system on behalf of the client that I go visit in Ireland so often. Andy and I meet on a near daily basis to discuss our genetic algorithm and how best to encourage the network to behave as we want it to. We are about a month from running our first predictive tests with our in house model. Reading this book encourages me that we are blazing down the right path.

Bernanke didn’t address the outlook for monetary policy or the economy, or expand on the Fed’s Aug. 1 statement. His remarks, focused on economic measurement, will be delivered via prerecorded video.

The 58-year-old Fed chief, a former Princeton professor, said economists should “increase the attention paid to microeconomic data, which better capture the diversity of experience across households and firms.” Also, researchers should “seek better and more-direct measurements of economic well-being, the ultimate objective of our policy decisions.”

He said interesting projects include the Organization for Economic Co-operation and Development’s Better Life Initiative, which aims at measuring quality of life in different countries, and the Gross National Happiness index compiled by Bhutan.

Since the Euro's existence, it has been debated by analysts that the U.S. Dollar is losing its place as the only reserve currency in the world. In other words, the age of U.S. Dollar hegemony was coming to an end. Central Banks such as Bank of Russia have started diversifying into reserve currencies other than the U.S. Dollar, most recently theAustralian Dollar. This is the effect of a global sentiment that the U.S. Dollar outlook is extremely bearish. A number of factors including low interest rates, a weakening U.S. economy, a perceived shift to emerging markets by multinational corporations, a rising China and India, and other factors, make the U.S. Dollar look weak-- especially with new choices such as the Euro (FXE), Chinese Renmimbi, and others.

Knight Capital Group Inc. (KCG) has “all hands on deck” and is in close contact with clients and counterparties as it tries to weather trading errors that cost it $440 million, Chief Executive Officer Thomas Joyce said.

Joyce said it’s “hard to comment” on discussions with creditors as Knight stock extended a two-day plunge to 70 percent and the firm explored strategic and financial alternatives following a loss almost four times its annual profit. The problems were triggered by what Joyce called “a bug, but a large bug” in software as the company, one of the largest U.S. market makers, prepared to trade with a New York Stock Exchange program catering to individual investors.

Knight Capital Group Inc. (KCG) said losses from yesterday’s trading breakdown are $440 million, almost quadruple its 2011 net income and more than some analysts had estimated, and the firm is exploring strategic and financial alternatives. Its stock has lost 66 percent in two days.

Knight said it will continue its trading and market-making today as it considers its options. Yesterday’s issue was related to the installation of trading software and resulted in the company sending “numerous erroneous orders,” the Jersey City, New Jersey-based firm said today. The stock tumbled 50 percent to $3.46 at 9:36 a.m. New York time today.

Clinton Ang, the grandson of a gunny- sack seller who emigrated last century from China to Singapore, oversees a fortune valued at almost $80 million for himself and three siblings.

That makes him a target for wealth managers in Singapore, the private-banking capital of Asia. Yet the 39-year-old managing director of Hock Tong Bee Pte, which evolved from his grandfather’s sacks and foodstuff supplier into a purveyor of $6,000 Grand Cru wines, has already fired two bankers and prefers mostly to manage the money himself.

“I am very open to private banks for their propositions, but I want them to be relevant,” said Ang, who’s cut the amount of his family’s money managed by professionals to less than 5 percent from 25 percent three years ago. “We felt we could do better ourselves.”

Disillusionment with investment products and returns has made Asian millionaires such as Ang take greater control of their wealth than rich Europeans. Managers at Credit Suisse Group AG (CSGN), Citigroup Inc. and other banks in Asia have full discretion over clients’ portfolios for just 4 percent of assets under management, according to a June report from Boston Consulting Group. That’s down from 7 percent in 2006. In Europe, it’s 23 percent, rising from 18 percent six years ago.

“Asia’s wealthy lost a lot of trust in their private banks and private bankers during the 2008 financial crisis,” said Peter Damisch, a Zurich-based BCG partner and managing director who co-authored the report.

{kind=link}