Friday, August 28, 2020

Sunday, August 23, 2020

Friday, August 21, 2020

Thursday, August 20, 2020

Jeffrey Epstein’s Private Banker At Deutsche & Citi Found Swinging From A Rope

Jeffrey Epstein’s private wealth banker, who brokered and signed off on untold multiple millions of dollars in controversial Deutsche Bank and Citibank loans spanning two decades for the convicted pedophile, has died from a reported suicide.

The news of yet another mysterious Epstein-linked death comes shortly after the FBI was seeking to interview the bank executive about loans he approved for Epstein and the indicted child trafficker’s labyrinth of US-based and offshore companies.

The Los Angeles County Medical Examiner confirmed Thomas Bowers died by an apparent suicide by hanging at his home.

Bowers headed the private wealth banking division for Deutsche Bank and signed off on millions in loans to Epstein.

Bowers, prior to taking over the private banking arm at Deutsche Bank, served in the same top position at Citibank, as the head of the bank’s private wealth arm. Citigroup also made massive loans to Epstein, according to records and banking sources who spoke to True Pundit.

True Pundit founder Mike “Thomas Paine” Moore previously headed anti-money laundering for a major Citigroup division during the time frame Citi commenced large loans to Epstein.

“The loans to Epstein were personal and commercial,” Paine confirmed. “The Citi loans I can confirm were for more than $25 million. Some were secured, some were not.”

Did Citi bend its lending rules for Epstein? Paine said that appears “quite likely,” with Bowers and other Citi executives he later recruited to work for him at Deutsche all working to secure the approvals regardless of compliance-related red flags.

And sources said Citi loaned Epstein much more money, eclipsing $100 million and also allowed Epstein to use the bank to send thousands of wire transfers from his accounts. Bowers, who turned up dead just days ago, brokered the loans for Epstein, sources said.

Bowers was the chief of Deutsche Bank’s Private Wealth Management division and worked from the bank’s Park Avenue offices in New York City. At Citi, Bowers served as the chief of the The Citi Private Bank and previously ran Citigroup’s Global Markets and Wealth Management businesses.

And when Bowers left Citi for Deutsche Bank, Epstein followed.

Meanwhile, Epstein stopped making payments on his millions in outstanding Citi loans. But that mattered little because Bowers approved new high-risk loans and credit lines from Deutsche Bank, sources said.

And that relationship with Epstein continued until Bowers left Deutsche Bank in 2015. By that time, Epstein had chalked up untold millions in loans with the help of Bowers who recruited many of his top private wealth top bankers from Citi to Deutsche Bank.

The FBI who was interested in interviewing Bowers, sources confirm. The FBI subpoenaed Deutsche Bank in May for all loans and accounts linked to Epstein and there were many unanswered questions. Deutsche Bank closed out Epstein’s accounts weeks after the bank was served federal subpoenas.

Federal law enforcement officials said the FBI planned to interview all Wall Street wealth fund managers who worked for Epstein. Bowers included.

How much money did Deutsche broker for Epstein? That number to this point has proven elusive. The FBI is not talking, but one executive divulged Epstein had secured more than $60 million from Deutsche Bank’s U.S. and German arms. Likely that number is larger, but at this point the bank is keeping its exposure quiet.

Just like Bowers had brokered for Epstein at Citi, Deutsche also set the convicted pedophile up with over a dozen bank accounts that Epstein employed to receive and send wires and funds.

One banking executive said Bowers had visited Epstein on his private island at least once. Bowers had also visited Epstein in New York and attended social events at his mansion. Federal law enforcement sources did not comment about these new revelations.

However, Citi executives who worked with Bowers said the bank executive maintained an active night life and enjoyed the party circuit.

Epstein also helped bring in a plethora of new business from wealthy associates to Bowers at both Deutsche Bank and Citi, sources said.

“Epstein made Bowers and his financial institutions hundreds of millions of dollars,” one executive said. “It really didn’t even matter that Epstein stiffed Citi for $30 million in defaults because he brought so much new money, new blood in. Citi made far more than it lost.”

Seems like a pattern. The American Banker reports:

Epstein brought lucrative clients into JPMorgan’s private-banking unit and was close to former head Jes Staley, who visited Epstein’s private island as recently as 2015. Leon Black, Apollo Global Management’s billionaire chairman, met with the financier from time to time at the company’s New York offices, and used Epstein for tax and philanthropic advice.

Police reportedly found Bowers hanging from a rope in his California home.

He was 55.

Previous press releases detailing Bowers’ role with the private wealth arm of Deutsche, detailed the division and its target clientele:

Deutsche Bank Private Wealth Management has been serving the interests of wealthy individuals, families and select institutions for more than a century. With offices across the U.S., Deutsche Bank’s Private Wealth Management business division provides a variety of customized solutions to private clients worldwide including traditional and alternative investments, risk management strategies, lending, trust and estate services, wealth transfer planning, family office services, custody and family and philanthropy advisory.

Private Wealth Management includes the U.S. Private Bank and Deutsche Bank Alex. Brown, the private client services division of Deutsche Bank Securities Inc., the investment banking and securities arm of Deutsche Bank AG in the United States and a member of NYSE, FINRA and SIPC.

This story is developing.

Friday, August 14, 2020

A New World Order & "The End Of Capital Markets As We Have Known Them"

The following letter was sent by Bob Rodriguez to his friends and colleagues yesterday, as well as to Bob Huebscher. Bob Rodriguez has graciously allowed us to publish it.

Robert L. Rodriguez was the former portfolio manager of the small/mid-cap absolute-value strategy (including FPA Capital Fund, Inc.) and the absolute-fixed-income strategy (including FPA New Income, Inc.) and a former managing partner at FPA, a Los Angeles-based asset manager. He retired at the end of 2016, following more than 33 years of service.

He won many awards during his tenure. He was the only fund manager in the United States to win the Morningstar Manager of the Year award for both an equity and a fixed income fund and is tied with one other portfolio manager as having won the most awards. In 1994 Bob won for both FPA Capital and FPA New Income, and in 2001 and 2008 for FPA New Income.

The opinions expressed reflect Mr. Rodriguez’ personal views only and not those of FPA.

Dear friends and colleagues,

Though the virus pandemic has been tumultuous, challenging and with little precedence, from a capital market perspective, this market collapse was quite predictable.

Capital market excesses became pervasive in ways that were also unprecedented. Zombie companies, corporate operating strategies that elevated financial risk to extreme levels and consumers who also became highly leveraged were the accepted actions of the day. Prudence was an extremely rare virtue. Many times I expressed the opinion that I thought the various equity markets were at least 40-60% over valued. Recent events would tend to confirm my assessment.

Back in 2009, in my Morningstar speech, and then after I returned from my 2010 sabbatical, I argued that, if we did not get our economic house in order, we would experience a crisis of equal or greater magnitude than the 2008-2009 period and that this would take place after 2017.

With the passage of the 2017 omnibus bill and the 2017 tax cut, along with a continuation of unsound and insane monetary policies, this speculative excess period was able to be extended. We knew there would be a pin that would prick this unbelievably speculative bubble but we just didn’t know what it would be. Now we do.

Our economic and financial market systems were not prepared with appropriate “rainy day reserves” to withstand an exogenous shock. Balance sheets were stretched in all economic sectors. The shock to the US economy by the bombing of Pearl Harbor and the beginning of WW2 was more traumatic and of greater magnitude than what we are experiencing now and it would also last longer. However, after 12 years of Depression, the financial system was cleansed of speculative excesses that allowed for a financial re-leveraging of the economy to fight the war. After the carnage was over, the economy was able to grow out of an extreme leverage position. In contrast to then, this is not the case today, given that the economy is already extremely leveraged prior to the onset of the crisis. My worst fears have materialized.

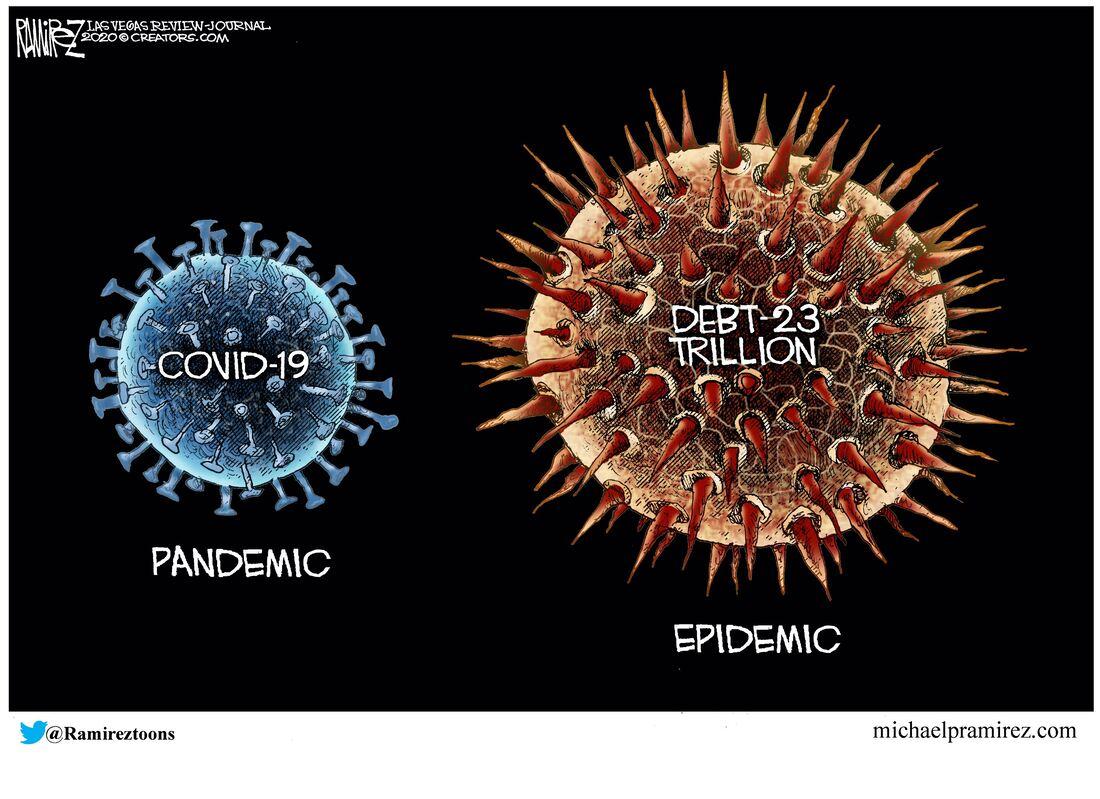

Since 2013, I have been preparing for an economy of monumental excess, where debt and deficits do not appear to matter, along with Fed and other central bank monetary policies that totally distort the fundamental elements of the Capital Asset Pricing Model. With the events of the past three weeks, the perversion and conversion to a dystopian capital market and economic system is virtually complete.

As for me, with the Fed's announcement of unlimited QE and its “will buy or support almost anything,” along with the pending passage of a $2-2.5 trillion stimulus package, this is the end of the capital markets as we have known them.

We have now entered unlimited QE and MMT where there is no escape.

It is the Roach Motel all over again.

In Chairman Bernanke‘s 2010 Washington Post op-ed, he argued that QE would lead to a virtuous economic cycle; therefore, the Fed would eventually be able to exit from its QE operations. I argued that once initiated, a reversal would be impossible. It would be like the Roach Motel, “You can check in, but you cannot check out.”

With the initiation of the Fed’s complete takeover and control of the US financial economy, there is now absolutely no accurate pricing discovery in the capital markets and we have entered a period of total manipulation. In light of this, the only markets I have an interest in are those where the heavy hand of government is not involved or only minimally involved. This leads me to rare commodities and collectibles. The public equity and debt markets are now nothing more than greater fool markets that are led by the greatest fools of all, the Fed and the Congress. US capital markets, RIP!

Despite my having avoided 100% of the market carnage and also being profitable, I have to shed a tear for the passing of a capital market that has benefitted the real and financial economy so well for decades. In 2008, when I wrote, “Crossing the Rubicon,” I argued we had crossed over into a new economic order and system. Little did I know that within twelve short years this transformation would be virtually complete. We have entered into a far more dangerous environment where normal rules of analytics will likely not apply.

When everything is essentially socialized as to risk, a return vs risk evaluation is essentially meaningless since the risk side of the equation has been truncated.

Over a period of time which I cannot estimate yet, I will continue my preparation for a far different economic and financial environment.

Capital deployment strategies will likely have to change from what has been the norm in the post WW2 environment. We are in a New World Order.

I hope I am wrong in my assessment, but I doubt it.

Good luck,

Bob

Did Buffett Just Bet Against The US? Berkshire Buys Barrick Gold, Dumps Goldman

This is going to get awkward.

Berkshire Hathaway's latest 13F just dropped and contained inside is a signal that none other than the Oracle Of Omaha appears to now be quietly betting against The United States.

Why? Because for years - in fact for as long we can remember - Warren Buffet has denigrated gold:

In a speech delivered at Harvard in 1998, Buffett said:

“(Gold) gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

He once famously said:

“Gold is a way of going long on fear, and it has been a pretty good way of going long on fear from time to time. But you really have to hope people become more afraid in a year or two years than they are now. And if they become more afraid you make money, if they become less afraid you lose money, but the gold itself doesn’t produce anything.”

In his 2011 letter, Buffett noted that for $9.6 trillion you could buy "pile a" — all of the gold in the world, or "pile b" — the entire US cropland (400 million acres) plus 16 ExxonMobils and still have another $1 trillion left over.

"Admittedly, when people a century from now are fearful, it's likely many will still rush to gold," he wrote. "I'm confident, however, that the $9.6 trillion current valuation of pile A will compound over the century at a rate far inferior to that achieved by pile B."

In 2013, Buffett even went so far as to mock investors betting on gold, saying that there were better places to put your money.

“What motivates most gold purchasers is their belief that the ranks of the fearful will grow,” Buffett wrote in 2012. “During the past decade that belief has proved correct. Beyond that, the rising price has on its own generated additional buying enthusiasm, attracting purchasers who see the rise as validating an investment thesis. As ‘bandwagon’ investors join any party, they create their own truth -- for a while.”

At Berkshire's 2018 annual meeting, Buffett compared $10,000 invested in stocks and gold in 1942 (the first year he invested in stocks):

"... for every dollar you could have made in American business, you'd have less than a penny of gain by buying into a store of value which people tell you to run to every time you get scared by the headlines."

And in his 2019 letter he reiterated:

"The magical metal was no match for the American mettle."

All of which makes the following even more stunning...

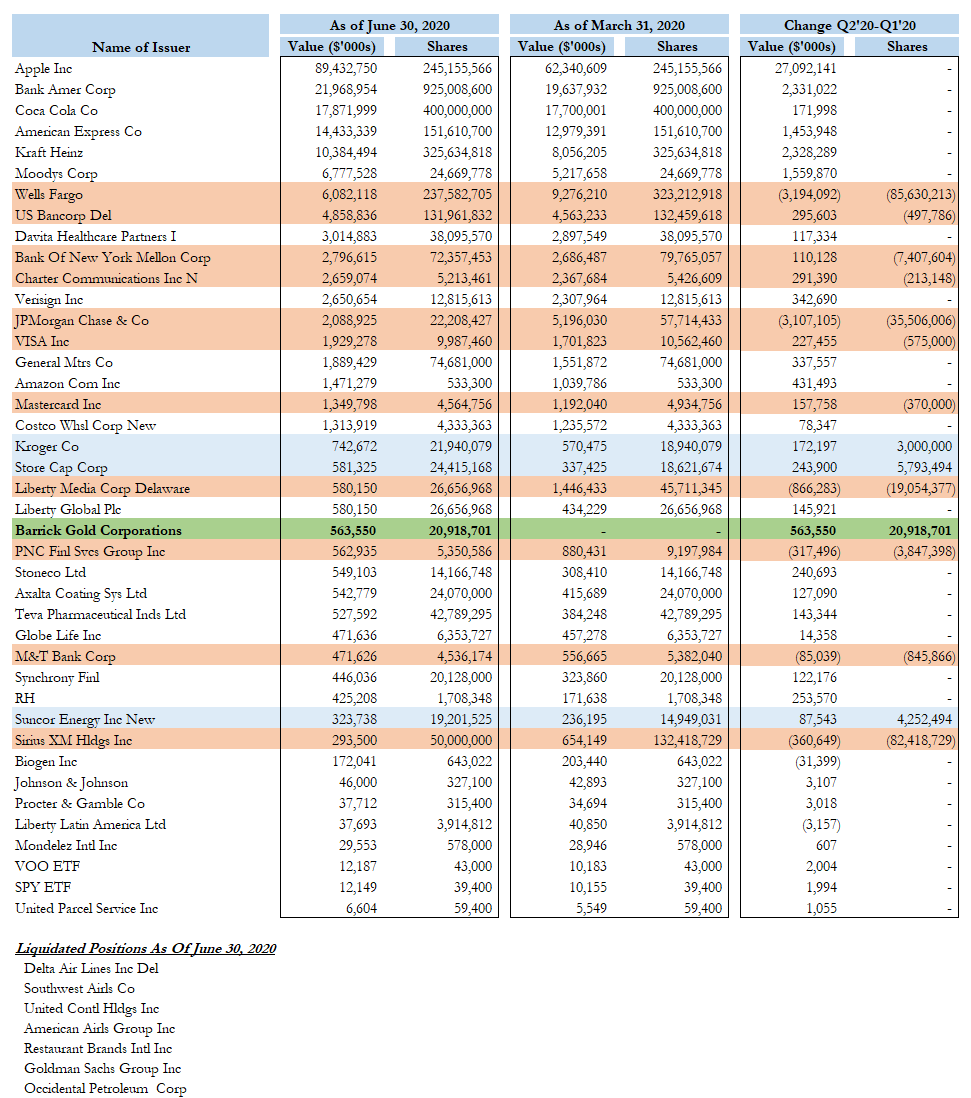

According to the latest 13F, Howard Buffett's Berkshire Hathaway not only dumped all his airlines - as we learned previously 0 but has also liquidated huge amounts of its exposure to US banks (exiting Goldman Sachs entirely).

- Berkshire's JPMorgan Stake Down 62% to 22.2M Shrs

- Berkshire's Wells Fargo Stake Down 26% to 238M Shrs

- Berkshire trimmed its bet on PNC Financial and M&T Bank as well as Bank of New York Mellon Corp., Mastercard, and Visa.

- Berkshire Exits Goldman stake entirely

And while he modestly added to his positions in Kroger, Store Cap and Suncor Energy, the only new stock he bought in Q2 was... the world's (formerly biggest) gold miner:

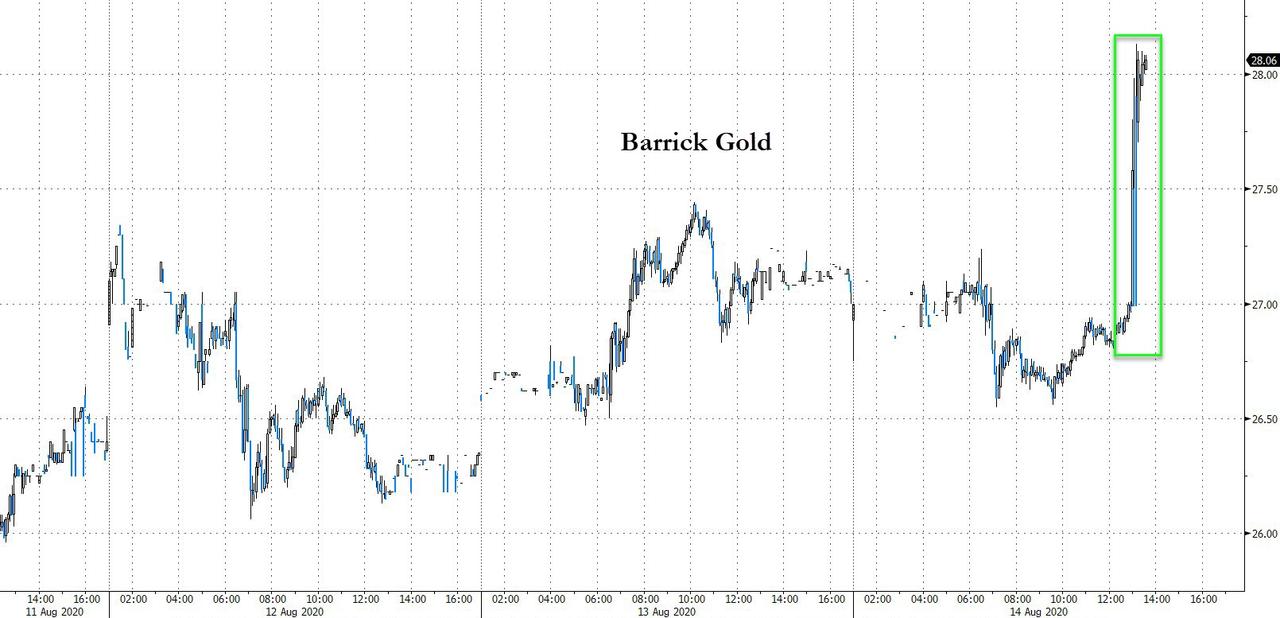

- Berkshire took a new stake (20.9 million shares) in Barrick Gold, a holding that was valued at about $564 million at the end of that period.

Barrick Gold is up around 6% after hours...

Of course, we do note that this 13F filing reflects the stock picks of Buffett as well as his long-time deputies, Todd Combs and Ted Weschler. So it’s unclear who exactly put money to work in Barrick.

So, the famously anti-gold investor has abandoned banks - 'the backbone of America's credit-driven economy - in favor of a gold miner (which was the largest in the world until last year when Newmont bought Goldcorp).

Is Buffett betting against America with a levered position on precious metals?

What is most ironic about all of this is that Warren's father, Howard Buffett, is among the great gold bugs of all time.

As we noted in 2010, a must read essay by Howard Buffett, father of the "legendary" investor who initially was so very much against derivatives then promptly changed his tune, discusses fiat money and gold, and concludes that "human freedom rests on gold redeemable money."

In this stunningly simple, straightforward, and flawless analysis, Buffett's father stresses the relation between money and freedom and contends that without a redeemable currency, an individual's freedom and one's access to property is dependent on goodwill of politicians.

Buffett also says that paper money systems generally collapse and result in economic chaos. He goes on to observe that a gold standard would restrict government spending and give people greater power over the public purse. Lastly, back in 1948, Howard Buffett, said this the "present" is the right time to restore the gold standard. Alas, 60 years later, his advice has still been largely ignored, and as a result we have a global economy that stands on the precipice of global default with runaway budget deficits across the entire developed world. Key quotes:

"Is there a connection between Human Freedom and A Gold Redeemable Money? At first glance it would seem that money belongs to the world of economics and human freedom to the political sphere.

But when you recall that one of the first moves by Lenin, Mussolini and Hitler was to outlaw individual ownership of gold, you begin to sense that there may be some connection between money, redeemable in gold, and the rare prize known as human liberty. Also, when you find that Lenin declared and demonstrated that a sure way to overturn the existing social order and bring about communism was by printing press paper money, then again you are impressed with the possibility of a relationship between a gold-backed money and human freedom."

His conclusion is eerily prophetic with what is happening with US society currently:

"I warn you that politicians of both parties will oppose the restoration of gold, although they may outwardly seemingly favor it. Unless you are willing to surrender your children and your country to galloping inflation, war and slavery, then this cause demands your support. For if human liberty is to survive in America, we must win the battle to restore honest money."

And of course, he notes that the Federal Reserve is at the forefront of those who will do everything in their power to prevent a return of the gold standard:

Most opponents of free coinage of gold admit that that restoration is essential, but claim the time is not propitious. Some argue that there would be a scramble for gold and our enormous gold reserves would soon be exhausted.

Actually this argument simply points up the case. If there is so little confidence in our currency that restoration of gold coin would cause our gold stocks to disappear, then we must act promptly.

The danger was recently highlighted by Mr. Allan Sproul, President of the Federal Reserve Bank of New York, who said:

"Without our support (the Federal Reserve System), under present conditions, almost any sale of government bonds, undertaken for whatever purpose, laudable or otherwise, would be likely to find an almost bottomless market on the first day support was withdrawn."

Our finances will never be brought into order until Congress is compelled to do so. Making our money redeemable in gold will create this compulsion.

The full essay is below, which we are confident was never read by Howard's "oracular" son... until perhaps very recently...

Did it really take him until he was 90-years-old to realize that his dad was right after all?

So what happens next? Do Munger and Buffett buy bitcoin?

Thursday, August 13, 2020

A Preview Of The Fed's Coming Direct Money Transfers: Brainard Says Fed Collaborating With MIT On "Hypothetical" Digital Currency

One week ago, we published a remarkable interview with two former Fed economists - Simon Potter and Julia Coronado - who have tremendous impact and influence on prevailing thinking at the Federal Reserve, and who hinted at the Fed's last ditch reflationary strategy: wiring digital money into the bank accounts of Americans, bypassing the reserve system entirely, and sparking an inflationary conflagration. As we said last Monday, "the two propose creating a monetary tool that they call recession insurance bonds, which draw on some of the advances in digital payments, which will be wired instantly to Americans."

"One of the issues Congress had in passing the Cares Act is identifying who’s got mainly tip income, who doesn’t have sick days. If society wanted, you could use large datasets to direct fiscal transfers to those people." - Bloomberg Interview with Coronado And Potter

And while this idea may have seemed absolutely ludicrous as recently as just one year ago, the fact that the just as ludicrous Helicopter Money is now de facto policy means that direct deposits of cash by the Fed into individual accounts is becoming increasingly probable, the only thing missing is the "digital currency" that would be used by the central bank.

Addressing this issue, on Thursday afternoon, Federal Reserve Governor Lael Brainard hinted once again at the coming monetary revolution when she said that the Fed is studying the opportunities and challenges presented by central bank digital currencies.

"To enhance the Federal Reserve’s understanding of digital currencies, the Federal Reserve Bank of Boston is collaborating with researchers at the Massachusetts Institute of Technology in a multi-year effort to build and test a hypothetical digital currency oriented to central bank uses."

The objectives of our research and experimentation across the Federal Reserve System are to assess the safety and efficiency of digital currency systems, to inform our understanding of private-sector arrangements, and to give us hands-on experience to understand the opportunities and limitations of possible technologies for digital forms of central bank money. These efforts are intended to ensure that we fully understand the potential as well as the associated risks and possible unintended consequences that new technologies present in the payments arena.

In prepared remarks of a speech titled simply enough "An Update on Digital Currencies" and prepared for delivery Thursday at a Fed technology event, Brainard said that "a significant policy process would be required to consider the issuance of a CBDC, along with extensive deliberations and engagement with other parts of the federal government and a broad set of other stakeholders."

The punchline: "It is important to understand how the existing provisions of the Federal Reserve Act with regard to currency issuance apply to a CBDC and whether a CBDC would have legal tender status, depending on the design. The Federal Reserve has not made a decision whether to undertake such a significant policy process, as we are taking the time and effort to understand the significant implications of digital currencies and CBDCs around the globe."

So what would prompt the Fed to undertake this significant policy process? Why another crisis, of course.

For those who missed our comments on the recent interview with Potter and Coronado which lays out quite clearly just what is coming and what the motive is behind the Fed's fascination with digital currencies, here are excerpts from our Aug 3 post again: From "The Fed Is Planning To Send Money Directly To Americans In The Next Crisis"

* * *

We read with great interest a Bloomberg interview published on Saturday with two former central bank officials: Simon Potter, who led the Federal Reserve Bank of New York’s markets group i.e., he was the head of the Fed's Plunge Protection Team for years, and Julia Coronado, who spent eight years as an economist for the Fed’s Board of Governors, who are among the innovators brainstorming solutions to what has emerged as the most crucial and difficult problem facing the Fed: get money swiftly to people who need it most in a crisis.

The response was striking: the two propose creating a monetary tool that they call recession insurance bonds, which draw on some of the advances in digital payments, which will be wired instantly to Americans.

As Coronado explains the details, Congress would grant the Federal Reserve an additional tool for providing support—say, a percent of GDP [in a lump sum that would be divided equally and distributed] to households in a recession. Recession insurance bonds would be zero-coupon securities, a contingent asset of households that would basically lie in wait. The trigger could be reaching the zero lower bound on interest rates or, as economist Claudia Sahm has proposed, a 0.5 percentage point increase in the unemployment rate. The Fed would then activate the securities and deposit the funds digitally in households’ apps.

As Potter then elucidates, "it took Congress too long to get money to people, and it’s too clunky. We need a separate infrastructure. The Fed could buy the bonds quickly without going to the private market. On March 15 they could have said interest rates are now at zero, we’re activating X amount of the bonds, and we’ll be tracking the unemployment rate—if it increases above this level, we’ll buy more. The bonds will be on the asset side of the Fed’s balance sheet; the digital dollars in people’s accounts will be on the liability side."

And that, in a nutshell, is how the Fed will stimulate the economy in the next crisis in hopes of circumventing the reserve creation process: it will use digital money apps (which explains the Fed's recent fascination with cryptocurrency and digital money) to transfer money directly to US consumers.

To be sure, the narrative is already set for how the Fed will "sell" this direct transfer of money to the rest of the world and the broader US population: as Coronado explains "it’s the most efficient from a macroeconomic standpoint in supporting spending and confidence. The fear of unemployment acts as an accelerant on a recession. There’s a shock—people are losing their jobs or worry about losing their jobs. They get very risk-averse. [By] getting money to consumers you can limit the depth and duration of a recession."

And the kicker:

"you could actually generate real inflation. It could be beneficial for not only avoiding negative rates but creating a more healthy interest-rate market, a more healthy yield curve."

So there you have it: the one thing that was missing from a decade of monetary tinkering by the Fed, the spark of inflation, will finally arrive as the Fed gives money to those most likely to spend it: the lower and middle classes of society.

But wait, there's more: now that the Fed is implicitly focusing on racial inequality, and soon explicitly with Joe Biden going so far as to urge the Fed to fight "racial economic inequality" and former Minneapolis Fed president Kocherlakota writing an op-ed in which he said the Fed "should have a third mandate on racial inquality", the stage is now set for the Fed to specifically release funds for those who have "suffered from inequality", and once the time comes when the narrative allows to deploy reparations or direct funding to minorities, the Fed will be ready.

* * *

Below we republish the Bloomberg Markets interview with Coronado and Potter because it lays out, very clearly, just what the next monetary stimulus will look like now that helicopter money is fully engaged and money is about to be sent by the Fed directly to those Americans the Fed finds to be "in need."

BLOOMBERG MARKETS: How would recession insurance bonds work?

JULIA CORONADO: Congress would grant the Federal Reserve an additional tool for providing support—say, a percent of GDP [in a lump sum that would be divided equally and distributed] to households in a recession. Recession insurance bonds would be zero-coupon securities, a contingent asset of households that would basically lie in wait. The trigger could be reaching the zero lower bound on interest rates or, as economist Claudia Sahm has proposed, a 0.5 percentage point increase in the unemployment rate. The Fed would then activate the securities and deposit the funds digitally in households’ apps.

And so instead of these gyrations we’ve been going through to get money to households, it would happen instantaneously.

SIMON POTTER: It took Congress too long to get money to people, and it’s too clunky. We need a separate infrastructure. The Fed could buy the bonds quickly without going to the private market. On March 15 they could have said interest rates are now at zero, we’re activating X amount of the bonds, and we’ll be tracking the unemployment rate—if it increases above this level, we’ll buy more. The bonds will be on the asset side of the Fed’s balance sheet; the digital dollars in people’s accounts will be on the liability side.

BM: Aside from speed, what are the main advantages of this approach?

JC: It’s the most efficient from a macroeconomic standpoint in supporting spending and confidence. The fear of unemployment acts as an accelerant on a recession. There’s a shock—people are losing their jobs or worry about losing their jobs. They get very risk-averse. [By] getting money to consumers you can limit the depth and duration of a recession. And you could actually generate real inflation. It could be beneficial for not only avoiding negative rates but creating a more healthy interest-rate market, a more healthy yield curve.

BM: What are the origins of the idea?

JC: The Bank of England has proposals for digital currency. And a number of people have talked about the need for monetary financing—the idea that the interest-rate tool is simply less effective in lower growth, slower credit growth economies. Helicopter money [making direct payments to the public] goes back to Milton Friedman, but Ben Bernanke revisited it. Some people proposed doing that through financing fiscal stimulus. We think going directly to consumers is more efficient than wading through that sticky fiscal process.

BM: This policy could be complementary to Treasury stimulus?

JC: It’s not a replacement for fiscal policy. It makes sense from a fiscal perspective, for example, to authorize unemployment insurance benefits for people who lose their jobs and other assistance for medical-care providers in the current situation.

SP: The central bank is not elected. It cannot make allocation decisions about fiscal transfers. It’s now being pushed to make allocation decisions around credit with the Treasury, because we believe this situation is so unique that the private sector cannot make those decisions itself. The simplest way to do this would be a lump sum. Not in the way Congress did it. We’d take the bluntness of monetary policy and say anyone who’s eligible should get the same amount of bonds.

Fiscal controls could use the same infrastructure. The imperative to invest in it is high. Nearly all Treasury payments at some point touch the Fed because it’s the Treasury’s bank. The digital payment providers—called interface providers in the Bank of England proposal—would manage these accounts and link them to the Fed and Treasury.

BM: What are the objections from the Fed, and other challenges?

SP: The reaction from some of my former colleagues a while ago to the notion of helicopter money was not the most embracing. Some of those concerns have disappeared.

The two objections were related to the switch of deposits in normal times from the traditional banking system into digital accounts and the extra stress in crisis times as people want to get safe. An account with the central bank is safe because the central bank can always print money to honor that claim. A private bank can’t do that because their asset side has all kinds of credit on it. What we’ve created is a narrow bank-type model [narrow banks only take deposits and invest them in the safest assets] that’s small and fit for purpose, with a cap of $10,000 [per person].

JC: One challenge is making it profitable for digital providers. We want strict limitations on the fees so we’re reaching people that are underbanked, but we also want a public-private partnership with a diversity of competitors jumping into this market. Privacy is just as important, because one thing that might induce them is access to people’s data. As the Fed, are you blessing that, and what structure do you put around that?

SP: We’ll all have to deal with deep questions of privacy in the digital world. One of the issues Congress had in passing the Cares Act is identifying who’s got mainly tip income, who doesn’t have sick days. If society wanted, you could use large datasets to direct fiscal transfers to those people. But that’s a job for Congress.

BM: Have you seen similar trials elsewhere?

{kind=link}

{kind=link}

SP: Sweden is a leader in thinking about this in part because they had a large decline in cash use. China is testing versions of digital currency. Fintech firms in the U.S. are interested in this—there’s a stable coin version of our proposal. There’s easily sufficient innovation within the U.S. to do this. How to do it in a way that’s well regulated and serving the public purpose is something the Fed should focus on over the next few years. It would be a key accomplishment of the Fed and Treasury to get this infrastructure in place.