Earlier today, when we were conducting a routine check with the Office of the Currency Comptroller's on the total notional amount of derivatives held at the Big 4 banks in the context of the "JPMorgan break up" story, we found something stunning: using the latest, just released Q3 OCC data, JPMorgan is no longer America's undisputed derivatives king. Well, it still is at the HoldCo level, where it is number one in terms of notional derivatives with $65.5 trillion, but when one steps a level lower, namely the FDIC-insured commercial bank (the National Association or N.A.) level, something quite disturbing emerges. This:

As the chart above, which references Table 1 in the Q3 OCC report, shows Citigroup, or rather its FDIC-insured Citibank National Association entity, just surpassed JPM and is now the biggest single holder of total derivatives in the US. Furthermore, as the charts below show, while every other bank was derisking its balance sheet, Citi not only increased its total derivative holdings by $1 trillion in Q2, but by a whopping, and perhaps even record, $9 trillion in the just concluded third quarter to $70.2 trillion!

Here is Citi in context:

What is the reason for the surge in total derivative exposure? was it futures, options, forward or CDS? Neither. The answer: OTC traded swaps...

... which soared by $5 trillion in Q2 and over $8 trillion - or a massive 20% in just one quarter - in Q3 to a whopping $49 trillion, $16 trillion more than the OTC swaps held by JPMorgan or Goldman Sachs, and more than double the swaps held by Bank of America!

And that's not all: perhaps what is most bizarre is that Citigroup is the one bank whose HoldCo holds less derivatives, or $64.8 trillion, than its FDIC-insured N.A. OpCo which has $70.3 trillion in derivative notional exposure. For those wondering: this was not the case in the second quarter when the HoldCo ($61.8 trillion) held more derivatives than Citi's FDIC-insured bank ($61.1 trillion).

Then we started thinking:

Citigroup... swaps... Citigroup... swaps...

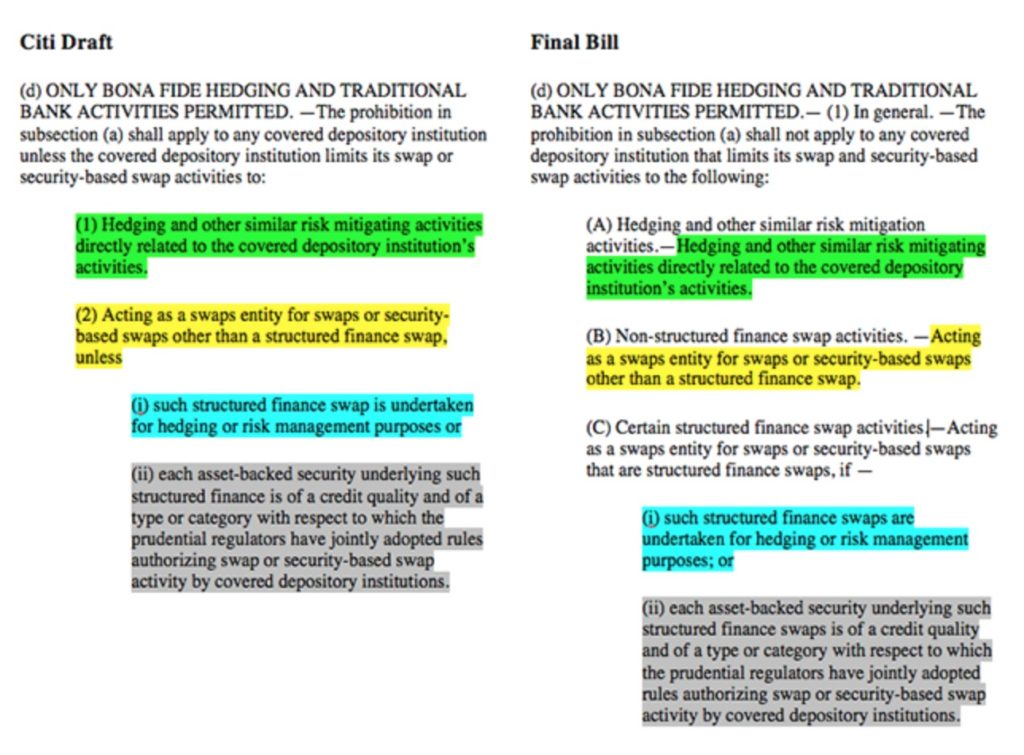

and a lightbulb click, because we remembered that it was none other than Citigroup that crafted the legislation on the swaps push-out provision which passed Congress without nary a peep from either side of the aisle, and which put taxpayers on the hook for FDIC-insured derivative exposure- and in Citi's own case a soaring $70 trillion as of September 30, 2014:

We also revealed that, not surprisingly, the main backer of the bill is notorious Wall Street puppet Jim Himes (D-Conn.) the man BusinessWeek branded "Wall Street's Favorite Democrat" who also happens to be a former Goldman Sachs employee.

And yet, despite all these critical recollections, many questions remains, such as:

- Why does Citi's FDIC-insured bank suddenly have more derivative notional exposure than its HoldCo: something which is generally without precedent?

- Why, when every other Big 4 bank is derisking its balance sheet and reducing its derivative exposure in light of far more stringent capital requirements, is Citigroup adding to its derivative notional and swap exposure at an unprecedented, feverish pace, which saw the bank boost its OTC Swaps holdings by 20% in just one quarter?

- When Congress was voting for the swaps push-out legislation, the Q3 OCC data was not yet publicly available. Was anyone in Congress aware that some $9 trillion had been added to the tally of taxpayer insured derivatives held at Citibank NA as of September 30.

- What is Citigroups and Citibank's total derivative and total swap exposure as of December 31, and has it continue to soar at a rate of roughly $10 trillion per quarter?

And perhaps most impotantly: what is the underlying trade that requires Citigroup to keep adding to its swap exposure at a time when increasing volatility is forcing all other banks to unwind swaps in order to minimize VaR and be in compliance with Fed capitalization requirements?

And then another lightbulb went over our heads: the last entity to do this was, drumroll, JPMorgan, in early 2013, just before its London whale trade imploded and when the bank's attempt to corner the IG9 market failed miserably but not before JPM's CIO trading desk doubled down, then doubled down again and doubled down some more taking their total derivative exposure to several hundred billion... before it all came crashing down.

Now, we are not saying Citigroup is in the same boat as JPM's infamous CIO which led to congressional hearings and what not - especially since $250 billion was manageable; $50 trillion will not be - but we do wonder: just what is going on behind the massivaly margined scenes if Citi is following every page in the London Whale book and on top of everything it also had to lobby and petition Congress to change the law just so whatever it is that Citigroup is doing, it could continue to do, and what's more: with explicit taxpayer-funded backing.

Which leads us to the final question:

- Is Citigroup about to become the "New Normal" AIG?

Source: OCC