Open a Forex Trading Account

The foreign exchange market (forex, FX, or currency market) is a form of

exchange for the global decentralized trading of international

currencies. Financial centers around the world function as anchors of

trading between a wide range of different types of buyers and sellers

around the clock, with the exception of weekends. The foreign exchange

market determines the relative values of different currencies. Non-US

Citizens have the ability to use non-US brokers. Click here to open a Forex account - Non-US Citizens only.

Tuesday, September 24, 2013

Credit Suisse Closing "Non-Super Rich", "Risky" Client Accounts

In a move that clearly seeks to distance the second largest Swiss

bank from potentially "risky" or just not that profitable (read "rich or super rich")

accounts, Credit Suisse announced today that it plans to close some

clients' accounts as it focuses on high-value customers in some

countries and pulls out of others altogether. The development is

somewhat ironic: while banks around the world scramble to obtain ultra

cheap funding, of which deposits are currently the cheapest alternative,

Credit Suisse is saying to people, thanks but no thanks, we don't want

your money. Then again, perhaps this is an admirable stance by the bank.

It certainly is preferable to CS eagerly accepting every last Swiss

Franc only to pull a Cyprus in a few months (indicatively speaking) and

"bailing in" said money. It does however pose the question: has CS found

an alternative method of funding its assets now that it is actively

deleveraging, and if so what, and who is the source?

More from AFP:

http://www.zerohedge.com/news/2013-09-24/credit-suisse-closing-non-super-rich-risky-client-accounts

More from AFP:

Taking this to its next logical step, assuming the disposed capital is indeed illegally acquired, it would be unable to bypass US, and western, Anti-Money Laundering checks for securities accounts, which would leave it only one option: US real estate, where as we have been reporting over the past 18 months, the NAR is explicitly exempt from AML provisions. In fact, the NAR would welcome all illegally procured foreign capital, especially if in a few months the US District Attorney earns some cheap brownie points announcing said real estate has been confiscated (as we saw recently in New York not once but twice)."We've decided to focus on certain segments and markets and exit some countries that are too small," said a spokeswoman for the Swiss banking giant.

Switzerland's Tages-Anzeiger newspaper reported that the accounts involved would be closed by the end of the year, affecting clients in nearly 50 countries.

The Credit Suisse spokeswoman said the bank would exit some countries entirely, including Congo, Angola and Turkmenistan. In others, such as Denmark and Israel, it will close small accounts to focus on the top segment of the market, she said.

Tages-Anzeiger said the bank considered the risk to its reputation in countries such as Turkmenistan, Uzbekistan and Belarus to be too high, and elsewhere wanted to focus on "rich and super-rich clients" with balances of at least one million Swiss francs (800,000 euros, $1.1 million).

In Israel, where many clients have dual US citizenship, the bank also wanted to reduce the regulatory burden of complying with American tax law, the report said.

The bank had said in July it planned to exit smaller markets, as it announced second-quarter profits of 1.04 billion francs, a 32-percent increase from the year before.

...

Pressure has increased on banks in recent years to help identify accounts linked to organised crime, high-level corruption or other wrongdoing, causing the cost of complying with regulatory procedures to rise sharply.

http://www.zerohedge.com/news/2013-09-24/credit-suisse-closing-non-super-rich-risky-client-accounts

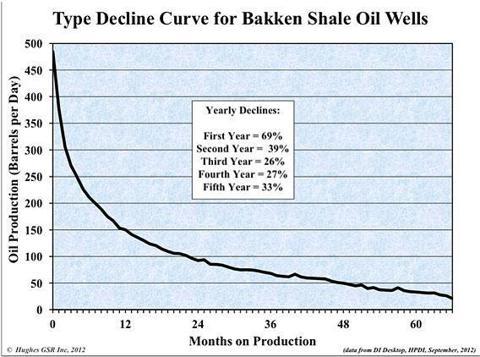

Bakken - Hype Versus Reality

As Wall Street, CNBC, and feckless politicians tout American energy independence from the miracle of shale oil, reality is already rearing its ugly head. Production grew by 24% over the first six months of 2012. Production has grown by only 7% over the first six months of 2013. That is a dramatic slowdown. The fact is that these wells deplete at an extremely rapid rate. Oil companies will always seek out the easiest to access oil first. They have already accessed the easy stuff. This explains the dramatic slowdown. Peak Bakken oil production will be below 1 million barrels per day. The last time I checked, we consumed 18 million barrels per day. I wonder when that energy independence will be achieved? Reality is a bitch.

Bakken Oil Production Growth Has Slowed Significantly In 2013

By: Devon Shire

http://seekingalpha.com/author/devon-shire [9]

The headlines ring of “booming” American oil production and “gluts” of oil (USO [10]). I’m here to tell you that while the boom is real, there is no glut of oil and we need to be aware that the huge production growth of the past eighteen months is going to slow.

It already is slowing.

I’ve been watching what is going on in the Bakken pretty closely because I think it is going to be an excellent proxy for what will happen across the country.

Let’s take a look at what happened to production in North Dakota during the first six months of last year (2012). Here is the raw data [11] detailing barrels of oil production per day:

December 2011 – 535,000 boe/day

January 2012 – 547,000 boe/day

February 2012 – 559,000 boe/day

March 2012 – 580,000 boe/day

April 2012 – 611,000 boe/day

May 2012 – 644,000 boe/day

June 2012 – 664,000 boe/day

Daily production in North Dakota increased by 129,000 barrels per day from December 2011 to June 2012.

Now let’s look at the same period for this year (2013):

December 2012 – 768,000 boe/day

January 2013 – 739,000 boe/day

February 2013 – 780,000 boe/day

March 2013 – 785,000 boe/day

April 2013 – 793,000 boe/day

May 2013 – 811,000 boe/day

June 2013 – 821,000 boe/day

Where last year production increased by 129,000 barrels per day in the first six months of the year, this year production is up by only 53,000 barrels per day.

Yes, the rate of growth in the Bakken has slowed considerably in 2013.

To understand why, a person needs to look at the production profile for these horizontal oil wells.

By the end of the first year of production, a new well is producing at a rate that is 30% of where it was the year before. That means a huge amount of drilling each year has to be done just to offset the production lost due to these steep decline rates.

Without a continuous step change each year in the number of wells being drilled and the capital available to do so, production in the Bakken is going to flatten.

Good things are still happening, but we can’t repeat every year the hyperbolic growth that we saw in 2012.

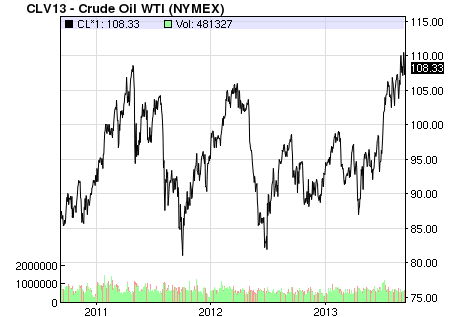

What this means for investors is that we shouldn’t expect oil prices to fall much from where we have seen them over the past three years.

For the past three years WTI oil prices have ranged from $85 per barrel to $105 per barrel. I think $85 is about as low as we can go for an extended period of time because that is likely just about the marginal cost of production for oil in the world today.

Production growth in the Bakken is slowing and so too will production growth in the Eagle Ford. That is the nature of these horizontal oil fields. We get an initial surge in production as capital comes into the play. Then that growth rate slows steadily until it flattens and enters a decline.

http://www.zerohedge.com/print/479286

Bakken Oil Production Growth Has Slowed Significantly In 2013

By: Devon Shire

http://seekingalpha.com/author/devon-shire [9]

The headlines ring of “booming” American oil production and “gluts” of oil (USO [10]). I’m here to tell you that while the boom is real, there is no glut of oil and we need to be aware that the huge production growth of the past eighteen months is going to slow.

It already is slowing.

I’ve been watching what is going on in the Bakken pretty closely because I think it is going to be an excellent proxy for what will happen across the country.

Let’s take a look at what happened to production in North Dakota during the first six months of last year (2012). Here is the raw data [11] detailing barrels of oil production per day:

December 2011 – 535,000 boe/day

January 2012 – 547,000 boe/day

February 2012 – 559,000 boe/day

March 2012 – 580,000 boe/day

April 2012 – 611,000 boe/day

May 2012 – 644,000 boe/day

June 2012 – 664,000 boe/day

Daily production in North Dakota increased by 129,000 barrels per day from December 2011 to June 2012.

Now let’s look at the same period for this year (2013):

December 2012 – 768,000 boe/day

January 2013 – 739,000 boe/day

February 2013 – 780,000 boe/day

March 2013 – 785,000 boe/day

April 2013 – 793,000 boe/day

May 2013 – 811,000 boe/day

June 2013 – 821,000 boe/day

Where last year production increased by 129,000 barrels per day in the first six months of the year, this year production is up by only 53,000 barrels per day.

Yes, the rate of growth in the Bakken has slowed considerably in 2013.

To understand why, a person needs to look at the production profile for these horizontal oil wells.

By the end of the first year of production, a new well is producing at a rate that is 30% of where it was the year before. That means a huge amount of drilling each year has to be done just to offset the production lost due to these steep decline rates.

Without a continuous step change each year in the number of wells being drilled and the capital available to do so, production in the Bakken is going to flatten.

Good things are still happening, but we can’t repeat every year the hyperbolic growth that we saw in 2012.

What this means for investors is that we shouldn’t expect oil prices to fall much from where we have seen them over the past three years.

For the past three years WTI oil prices have ranged from $85 per barrel to $105 per barrel. I think $85 is about as low as we can go for an extended period of time because that is likely just about the marginal cost of production for oil in the world today.

Production growth in the Bakken is slowing and so too will production growth in the Eagle Ford. That is the nature of these horizontal oil fields. We get an initial surge in production as capital comes into the play. Then that growth rate slows steadily until it flattens and enters a decline.

http://www.zerohedge.com/print/479286

Monday, September 23, 2013

$3.39T Quantitative Explosion: Fed Owns More Treasuries and MBSs Than Publicly Held Debt Amassed From Washington Through Clinton

The same day that the Federal Reserve's Federal Open Market Committee announced last week that the Fed would continue to buy $40 billion in mortgage-backed securities (MBSs) and $45 billion in U.S. Treasury securities per month, the Fed also released its latest weekly accounting sheet indicating that it had already accumulated more Treasuries and MBSs than the total value of the publicly held U.S. government debt amassed by all U.S. presidents from George Washington though Bill Clinton.

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

The same day that the Federal Reserve's Federal Open Market Committee announced last week

that the Fed would continue to buy $40 billion in mortgage-backed

securities (MBSs) and $45 billion in U.S. Treasury securities per month,

the Fed also released its latest weekly accounting sheet

indicating that it had already accumulated more Treasuries and MBSs

than the total value of the publicly held U.S. government debt amassed

by all U.S. presidents from George Washington though Bill Clinton.

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

The same day that the Federal Reserve's Federal Open Market Committee announced last week

that the Fed would continue to buy $40 billion in mortgage-backed

securities (MBSs) and $45 billion in U.S. Treasury securities per month,

the Fed also released its latest weekly accounting sheet

indicating that it had already accumulated more Treasuries and MBSs

than the total value of the publicly held U.S. government debt amassed

by all U.S. presidents from George Washington though Bill Clinton.

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

(CNSNews.com) - The same day that the Federal Reserve's Federal Open Market Committee announced last week

that the Fed would continue to buy $40 billion in mortgage-backed

securities (MBSs) and $45 billion in U.S. Treasury securities per month,

the Fed also released its latest weekly accounting sheet

indicating that it had already accumulated more Treasuries and MBSs

than the total value of the publicly held U.S. government debt amassed

by all U.S. presidents from George Washington though Bill Clinton.

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

(CNSNews.com) - The same day that the Federal Reserve's Federal Open Market Committee announced last week

that the Fed would continue to buy $40 billion in mortgage-backed

securities (MBSs) and $45 billion in U.S. Treasury securities per month,

the Fed also released its latest weekly accounting sheet

indicating that it had already accumulated more Treasuries and MBSs

than the total value of the publicly held U.S. government debt amassed

by all U.S. presidents from George Washington though Bill Clinton.

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

Since the beginning of September 2008, in fact, the Fed's ownership of Treasury securities and MBSs has increased seven fold.

As of the close of business Thursday, the Fed said, it owned approximately $2,052,055,000,000 in U.S. Treasury securities and approximately $1,339,771,000,000 in mortgage-backed securities—for a combined total of about $3,391,826,000,000 in Treasury securities and MBSs.

The U.S. Treasury divides the U.S. government debt into two parts: debt held by the public, which includes publicly traded Treasury securities such as Treasury bills, notes and bonds, and intra-governmental debt, which is money the Treasury has borrowed out of the Social Security trust fund and other government trust funds and then used to pay current expenses.

As of the opening of business back on Nov. 23, 2001, according to the Daily Treasury Statement, the federal government’s total debt held by the public was $3,383,605,000,000. (By the close of business that day, the total debt held by the public would increase to 3,406,661,000,000.) The $3,383,605,000,000 in U.S. Treasury debt held by the public as the morning of Nov. 23, 2001, represented the total publicly held debt the federal government had accumulated until that date from the moment the Treasury first opened during the presidency of George Washington.

The $3,383,605,000,000 the Treasury owed to the public as of the morning of Nov. 23, 2001 was less than the $3,391,826,000,000 in Treasury and mortgage-backed securities owned by the Federal Reserve as of the close of business last Thursday.

Thus the Federal Reserve now owns more debt in the form of U.S. Treasury securities and MBSs than the sum total of the publicly held debt that the U.S. government accumulated from George Washington’s administration into November 2001, during President George W. Bush’s first term.

The mortgage-backed securities owned by the Fed are those that have been issued and guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae. Ginnie Mae is government-owned corporation operated by the U.S. Department of Housing and Urban Development. Fannie Mae and Freddie Mac are congressionally chartered, government-sponsored enterprises, that are now held in conservatorships by the federal government.

“Fannie Mae and Freddie Mac are chartered by Congress as government-sponsored enterprises (GSEs) to provide liquidity in the mortgage market and to promote homeownership for underserved groups and locations,” the Congressional Research Service explained in a report published this August. “They purchase mortgages, guarantee them, and package them in mortgage-backed securities (MBSs), which they either keep as investments or sell to institutional investors. In addition to the GSEs’ guarantees, investors widely believe that MBSs are implicitly guaranteed by the federal government. In 2008, the GSEs’ financial condition had weakened and there were concerns over their ability to meet their obligations on $1.2 trillion in bonds and $3.7 trillion in MBSs that they had guaranteed. In response to the financial risks, the federal government took control of these GSEs in a process known as conservatorship as a means to stabilize the mortgage credit market.”

The federal government first took control of Fannie Mae and Freddie Mac on Sunday, Sept. 7, 2008. In its last weekly accounting sheet released before that, on Thursday, Sept. 4, 2008, the Fed said that it owned $479.726 billion in U.S. Treasury securities. That sheet did not even include a line item for mortgage-backed securities.

The Fed’s combined ownership of $3,391,826,000,000 in Treasury securities and mortgage-backed securities is now more than 7 times as great as the $479.726 billion in Treasury securities it owned five years ago before the takeover of Fannie and Freddie.

Of the ten members of the Federal Open Market Committee who voted on whether the Fed should continue purchasing $40 billion in MBS each month and $45 billion in Treasury securities, only one voted no. That was Esther George, who is president of the Federal Reserve Bank of Kansas City.

The Fed’s press release announcing the vote said George voted against the continued buying of Treasury securities and MBS because she was “concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.”

- See more at: http://cnsnews.com/news/article/terence-p-jeffrey/339t-quantitative-explosion-fed-owns-more-treasuries-and-mbss#sthash.lMYAYAJU.toT70JK9.dpuf

Apple Touch ID fingerprint tech 'broken', hackers say

Hackers claim to have broken Apple's iPhone 5S Touch ID fingerprint recognition system just a day after the phone was launched.

Germany's Chaos Computer Club claims it "successfully bypassed the biometric security of Apple's Touch ID using easy everyday means".By photographing a fingerprint left on a glass surface and creating a fake finger they were able to unlock the phone, the hackers claim.

But Apple maintains Touch ID is secure.

On its website the iPhone maker says there is a one in 50,000 chance of two separate fingerprints being alike and the technology provides "a very high level of security".

Karsten Nohl, chief scientist at SRLabs, a German hacking think tank, told the BBC: "It would have been incredible if Apple had managed to do something the rest of the biometrics industry has failed to achieve after decades of trying, so I'm not surprised it was hacked after just one day.

"Claiming this system offers a high level of security is just ridiculous," he added.

Convenience Apple does not suggest that Touch ID is a total replacement for traditional passcode security, simply a more convenient way of unlocking the phone.

The Chaos Computer Club believes fingerprint biometrics "should be avoided"

"Touch ID is designed to minimise the input of your passcode;

but your passcode will be needed for additional security validation,"

Apple says. But it does not address the ability of hackers lifting individual prints and creating fake fingers, as the Chaos Computer Club claims to have done.

Mr Nohl says a five-digit password would be more secure than a fingerprint and believes Apple should have focused on convenience rather than security in its marketing of the Touch ID feature.

On Friday, an influential US senator called for Apple to answer "substantial privacy questions" arising from the technology.

Apple did not respond to the BBC's request for a comment.

http://www.bbc.co.uk/news/technology-24203929

Sunday, September 22, 2013

Gold And Monetary Inflation Prospects

On Wednesday last the Fed surprised most people by deciding not to taper. What

is not generally appreciated is that once a central bank starts to use

monetary expansion as a cure-all it is extremely difficult for it to

stop. This is the basic reason the Fed has not pursued the idea, and why

it most probably never will.

That is a strong statement. But consider this: Paul Volcker faced this same dilemma in 1979, when he was appointed Chairman of the Fed. In raising interest rates to choke off inflation he had two things going for him that his successor has not: rising inflation was already over 10% so was an obvious priority, and importantly private sector debt-to-GDP was at a far lower level than today. It was a tough decision at the time to nearly double interest rates. Today, with official inflation low and private sector indebtedness high it would be extremely difficult.

Until official inflation picks up, it is far more comforting to pretend it won’t be an issue, which reasonably describes the Fed’s approach. Instead it is targeting unemployment rates, on the basis that price inflation is tied to capacity utilisation, which in turn is tied to employment.

One thing is certain in life, besides death and taxes, and that is if you expand the quantity of money prices eventually rise; or more accurately the purchasing power of debased money falls. The problem is how to measure currency debasement, and this has been a topic of heated debate since fiat currencies first developed. This has led me to propose a new measure of money, which at James Turk’s suggestion I am calling the Fiat Money Quantity (FMQ). The purpose is to gives us a measure of fiat money that enables us to assess the danger of currency hyperinflation. I shall be publishing a paper on this shortly explaining the methodology.

The principle behind it is to signal deviations from the long-term trend of currency growth to alert us to both monetary crises and excessive inflation. The approach is to unwind the historic progression from full gold convertibility to the current state of no convertibility. Our gold was first deposited with our banks, and then from there with the central bank. In return for our gold deposits we have been issued cash notes and coin and credits in the form of deposits at the bank, and our bank equally has deposits at the central bank.

The FMQ is therefore comprised of the sum of cash and coin, plus all accessible deposits, plus our bank’s deposits held at the central bank. This for the US dollar is illustrated in the chart below.

The dotted line is the long-term exponential trend rate, and it is immediately obvious that the FMQ is now hyper-inflating. It currently requires a $3.6 trillion contraction of deposits to return this measure of currency quantity back to trend.

This accurately sums up the problem facing the Fed. We must understand they are in an almost impossible position that dates back to their monetary response to the banking crisis. Not even Paul Volcker could have got us out of this one. Once the addiction to weak money hits this pace there is no solution without threatening to bring down the whole system.

http://www.zerohedge.com/news/2013-09-22/guest-post-gold-and-monetary-inflation-prospects

That is a strong statement. But consider this: Paul Volcker faced this same dilemma in 1979, when he was appointed Chairman of the Fed. In raising interest rates to choke off inflation he had two things going for him that his successor has not: rising inflation was already over 10% so was an obvious priority, and importantly private sector debt-to-GDP was at a far lower level than today. It was a tough decision at the time to nearly double interest rates. Today, with official inflation low and private sector indebtedness high it would be extremely difficult.

Until official inflation picks up, it is far more comforting to pretend it won’t be an issue, which reasonably describes the Fed’s approach. Instead it is targeting unemployment rates, on the basis that price inflation is tied to capacity utilisation, which in turn is tied to employment.

One thing is certain in life, besides death and taxes, and that is if you expand the quantity of money prices eventually rise; or more accurately the purchasing power of debased money falls. The problem is how to measure currency debasement, and this has been a topic of heated debate since fiat currencies first developed. This has led me to propose a new measure of money, which at James Turk’s suggestion I am calling the Fiat Money Quantity (FMQ). The purpose is to gives us a measure of fiat money that enables us to assess the danger of currency hyperinflation. I shall be publishing a paper on this shortly explaining the methodology.

The principle behind it is to signal deviations from the long-term trend of currency growth to alert us to both monetary crises and excessive inflation. The approach is to unwind the historic progression from full gold convertibility to the current state of no convertibility. Our gold was first deposited with our banks, and then from there with the central bank. In return for our gold deposits we have been issued cash notes and coin and credits in the form of deposits at the bank, and our bank equally has deposits at the central bank.

The FMQ is therefore comprised of the sum of cash and coin, plus all accessible deposits, plus our bank’s deposits held at the central bank. This for the US dollar is illustrated in the chart below.

The dotted line is the long-term exponential trend rate, and it is immediately obvious that the FMQ is now hyper-inflating. It currently requires a $3.6 trillion contraction of deposits to return this measure of currency quantity back to trend.

This accurately sums up the problem facing the Fed. We must understand they are in an almost impossible position that dates back to their monetary response to the banking crisis. Not even Paul Volcker could have got us out of this one. Once the addiction to weak money hits this pace there is no solution without threatening to bring down the whole system.

http://www.zerohedge.com/news/2013-09-22/guest-post-gold-and-monetary-inflation-prospects

Saturday, September 21, 2013

Alpari leaves US market

Letter from Alpari

Dear Trader,

I am writing to inform you of upcoming changes to Alpari (US) LLC's ("Alpari") business model that will impact your relationship with us. Following a strategic review, Alpari has decided to exit the US retail foreign exchange market as a Retail Foreign Exchange Dealer ("RFED") and focus on developing its successful institutional division, QuantumFX.

As of the close of business on Friday, September 27, 2013, Alpari will no longer be the counter-party to your trades. To facilitate the transition, Alpari has made arrangements to transfer your MetaTrader 4 trading account to Forex Capital Markets, LLC ("FXCM"). FXCM is a leader in online forex trading headquartered in the heart of New York City's Financial District at 55 Water Street, and is dually registered with the Commodity Futures Trading Commission ("CFTC") as a Futures Commission Merchant ("FCM") and an RFED with the National Futures Association ("NFA"), member ID 0308179.

Moving your account from Alpari to FXCM is simple, all you need is to complete this short form. There will be several changes to your account including your account number and login details, as your account will be transferred to a different counterparty but you can continue to trade through your MetaTrader 4 platform after the transfer is complete. For more information about the transfer, please visit our FAQ page.

Please note that after the close of business on September 27, 2013, Alpari will no longer be the counterparty to your trades. As such, all open positions will be liquidated and all floating profits/losses will be realized. The subsequent cash balance of your account will then be transferred to your new counterparty, FXCM.

Please be aware, FXCM intends to re-establish all open positions liquidated by Alpari. The re-establishment of positions is limited to positions liquidated by Alpari and does not include positions manually liquidated by clients between the time of this notification and the close of business at 5:00PM ET on Friday, September 27, 2013. Please manage any open positions with these considerations in mind. For more information about the transfer, please visit our FAQ page

Note: You are not required to accept the proposed transfer and may direct Alpari to liquidate your positions or transfer your account, including open positions, to a firm of your selection. If you wish to discuss alternative options regarding this transfer, please contact Alpari's customer service no later than 4:00PM ET Friday, September 27, 2013; otherwise, your account will be transferred to FXCM at the close of trading day.

Once again, for more information about the transfer, please visit our FAQ page. If you have any additional questions, please direct them to Alpari's customer service by email at cs@alpari-us.com, by phone at 1 (646) 825-5760, or via live chat. You may also contact FXCM's customer support by phone at 1 (212) 897-7660 or by email at clients@fxcm.com.

We sincerely appreciate your business with us and I would like to personally thank you for your continued support over the years. We wish you the best of luck in all of your future trading endeavors.

Sincerely,

Jermaine C. Harmon

CEO, Alpari (US), LLC

FXCM announced that it will be assuming the retail client accounts of Alpari US, in a notification issued today. The listed firm was chosen by Alpari US, as it exits the retail FX arena in the United States.

Alpari US has revealed that the 27th of September, the last Friday of the month, as its departure date. FXCM will take over client accounts from the specified date.

Alpari US issued a statement earlier today, providing further details of the reason the company was pulling out of the US market. The statement came after the news release issued by Forex Magnates about the move. In addition, the firm sent out an email to all of its clients, providing details about the withdrawal, and also contained specific questions and answers that could be raised by clients.

One of the most important questions for current clients was answered in the email.

“What will happen to my open positions? Alpari will not transfer open positions to FXCM. All open positions will be liquidated, and all pending orders will be cancelled at close of business at 5:00PM ET on Friday, September 27, 2013. Alpari recommends that you manage all your positions prior to this date. However, FXCM intends to re-establish the positions liquidated by Alpari. Please note, that the re-establishment of positions is limited to positions liquidated by Alpari, and does not include positions manually liquidated by clients, between the time of this notification and the close of business at 5:00PM ET on Friday, September 27, 2013. Additionally, FXCM will only be able to re-establish positions offered by both Alpari and FXCM.”

The US FX brokerage space has been systematically declining over the last three years since the implemetation of the new rules, which have affected leverage, capital adequacy and order types. Once a flourishing industry, the US FX brokerage sector was home to the world’s largest providers. The regulatory changes have had a negative impact, with a flurry of brokers packing their bags. Alpari US follows in the shadows of FX Solutions, Easy Forex, Forex Club and GFT.

The new rulings are thought to be positive for the market. However, when assessing their impact on traders, the results are quite the opposite. The reduction in the number of brokers from whom traders can choose, means that there will be little or no competition, in addition, brokers will not have the need nor desire to innovate and introduce new trading solutions. Only regulated firms in the USA are allowed to solicit US clients. Therefore, US clients will lose out.

Capital adequacy requirements for FX brokers in the US are extraordinarily high, when compared to other major regulators. In the UK, firms need to hold a minimum of seven hundred and thirty thousand Euros. In Singapore firms are obliged to hold one million Singapore dollars.

The $20 million bounty set by the US regulator, has been one of the major factors that has been drowning the FX markets in USA.

Turkey’s financial regulator, SPK, issued a circular specifying that it intends to increase capital requirements for brokers. Unlike other regulators, the SPK is following the direction of the NFA.

Financial terms of the transaction between FXCM and Alpari US have not been disclosed.

http://forexmagnates.com/fxcm-adopts-retail-fx-accounts-from-alpari-us/

Wednesday, September 18, 2013

NFA fines New York forex firm FXDirectDealer LLC $1.1 million and orders the firm to pay $1.8 million in restitution to customers

For Immediate Release

September 18, 2013

For more information contact:

Larry Dyekman (312) 781-1372, ldyekman@nfa.futures.org

Karen Wuertz (312) 781-1335, kwuertz@nfa.futures.org

NFA fines New York forex firm FXDirectDealer LLC $1.1 million and orders the firm to pay $1.8 million in restitution to customers

September 18, Chicago - National Futures Association (NFA) has issued a $1.1 million fine and a $1.8 million restitution order against FXDirectDealer LLC (FXDD), a registered futures commission merchant Forex Dealer Member of NFA located in New York City. The Decision, issued by NFA's Hearing Committee (Committee), is based on Complaints filed on June 29 and October 23, 2012 and a settlement offer submitted by FXDD.

The June 29 Complaint charged FXDD with using asymmetrical price slippage settings that favored FXDD over its customers; failing to supervise the trade integrity of the firm's electronic trading systems; failing to maintain complete and accurate records; and failing to review the use of promotional material. The June Complaint also charged FXDD with making improper price adjustments in customers' accounts; converting customer funds; willfully submitting misleading information to NFA and others; and failing to treat all customers equally when giving price adjustments.

In addition, the June Complaint charged FXDD with failing to implement an adequate anti-money laundering (AML) program; failing to develop and implement adequate screening procedures to determine whether persons and entities with whom FXDD intended to do forex business were required to be registered with the Commodity Futures Trading Commission (CFTC) and Members or Associates of NFA.

The October 23 Complaint charged FXDD with failing to implement an adequate AML program and failing to adequately supervise the firm's AML program.

As part of the settlement offer, FXDD agreed to pay restitution in the amount of $1,828,261 to FXDD customers who experienced unfavorable price slippage on "limit-fill-or-kill" trades placed in their accounts from December 10, 2009 until June 29, 2011.

In addition, FXDD will pay a fine of $1.1 million, of which $914,131 is attributable to FXDD's unfavorable price slippage practices. In a related action taken by the Commodity Futures Trading Commission, FXDD will pay an additional penalty of $914,131 to the CFTC.

FXDD neither admitted nor denied the allegations.

The complete text of the June 29 Complaint, October 23 Complaint and Decision can be viewed on NFA's website (www.nfa.futures.org).

http://www.nfa.futures.org/news/newsRel.asp?ArticleID=4299

September 18, 2013

For more information contact:

Larry Dyekman (312) 781-1372, ldyekman@nfa.futures.org

Karen Wuertz (312) 781-1335, kwuertz@nfa.futures.org

NFA fines New York forex firm FXDirectDealer LLC $1.1 million and orders the firm to pay $1.8 million in restitution to customers

September 18, Chicago - National Futures Association (NFA) has issued a $1.1 million fine and a $1.8 million restitution order against FXDirectDealer LLC (FXDD), a registered futures commission merchant Forex Dealer Member of NFA located in New York City. The Decision, issued by NFA's Hearing Committee (Committee), is based on Complaints filed on June 29 and October 23, 2012 and a settlement offer submitted by FXDD.

The June 29 Complaint charged FXDD with using asymmetrical price slippage settings that favored FXDD over its customers; failing to supervise the trade integrity of the firm's electronic trading systems; failing to maintain complete and accurate records; and failing to review the use of promotional material. The June Complaint also charged FXDD with making improper price adjustments in customers' accounts; converting customer funds; willfully submitting misleading information to NFA and others; and failing to treat all customers equally when giving price adjustments.