One of the nation’s top credit-rating agencies says that the U.S.

Treasury Department is likely to continue paying interest on the

government’s debt even if Congress fails to lift the limit on borrowing

next week, preserving the nation’s sterling AAA credit rating.

In a memo being circulated on Capitol Hill Wednesday, Moody’s

Investors Service offers “answers to frequently asked questions” about

the government shutdown, now in its second week, and the federal debt

limit. President Obama has said that, unless Congress acts to raise the

$16.7 trillion limit by next Thursday, the nation will be at risk of

default.

Not so, Moody’s says in the memo dated Oct. 7.

” We believe the government would continue to pay interest and

principal on its debt even in the event that the debt limit is not

raised, leaving its creditworthiness intact,” the memo says. “The debt

limit restricts government expenditures to the amount of its incoming

revenues; it does not prohibit the government from servicing its debt.

There is no direct connection between the debt limit (actually the

exhaustion of the Treasury’s extraordinary measures to raise funds) and a

default.

The memo offers a starkly different view of the consequences of

congressional inaction on the debt limit than is held by the White

House, many policymakers and other financial analysts. During a press

conference at the White House Tuesday, Obama said missing the Oct. 17

deadline would invite “economic chaos.”

The Moody’s memo goes on to argue that the situation is actually much

less serious than in 2011, when the nation last faced a pitched battle

over the debt limit.

“The budget deficit was considerably larger in 2011 than it is

currently, so the magnitude of the necessary spending cuts needed after

17 October is lower now than it was then,” the memo says.

Treasury Department officials did not immediately respond to requests for comment.

http://www.washingtonpost.com/blogs/post-politics-live/liveblog/live-updates-the-shutdown-4/?hpid=z2#c1e3ada3-dc00-41d8-92cb-327c5c814d82

Wednesday, October 9, 2013

US Treasuries Are "Riskier" Than Italian And Spanish Bonds

In the equity asset management world, the word risk is ubiquitously

interchangeable with the word "volatility" for myriad asset allocation

models that promise mathematical precision way beyond the realms of

possibility in a dynamic world. However, extending that definition of

risk, we thought it worth pointing out that, for the last month, US Treasury bonds have become more volatile (more risky) than Italian and Spanish bonds. Something to ponder for The Fed's new head we suspect...

The 3 month volatility of US Treasuries is now higher than that of Spain and Italy (both of which offer significantly higher yields than the US)...

One can only imagine the automated overweighting that a lower risk, higher return implies for the peripheral European bond markets... but for all those MPT asset allocators out there, when all you have is hammer...

The 3 month volatility of US Treasuries is now higher than that of Spain and Italy (both of which offer significantly higher yields than the US)...

One can only imagine the automated overweighting that a lower risk, higher return implies for the peripheral European bond markets... but for all those MPT asset allocators out there, when all you have is hammer...

Tuesday, October 8, 2013

This is what decline of a superpower looks like

WASHINGTON (MarketWatch) — Foreign policy analysts at home and abroad

have been predicting for years the inevitable decline of American power,

often with a fair amount of schadenfreude and sometimes even with glee.

But now that political dysfunction in Washington is accelerating, the

downsizing of the world’s only remaining superpower, all you hear is

whining.

“The American self-blockade is shocking,” Karl-Georg Wellmann, a

foreign-policy expert for German Chancellor Angela Merkel’s Christian Democratic party, complained to the business daily Handelsblatt. “The position as the West’s leading power will be affected.”

What Does Heart Surgery Really Cost, And Why Is It 70 Times More Expensive In The US?

Indian philanthropist and cardiac surgeon, Devi

Prasad Shetty is obsessed with making heart surgery affordable for

millions of Indians. As Bloomberg notes [4],

Shetty is not a public health official motivated by charity. He’s a

heart surgeon turned businessman who has started a chain of 21 medical

centers around India. By trimming costs, he has cut the price of artery-clearing coronary bypass surgery to 95,000 rupees ($1,583), half of what it was 20 years ago, and wants to get the price down to $800 within a decade. The same procedure costs $106,385 at Ohio’s Cleveland Clinic. Of course, this will come as no surprise after we showed the incredible spread of the price of an appendectomy [5]. “It shows that costs can be substantially contained,” notes the World Heart Federation, "it’s possible to deliver very high quality cardiac care at a relatively low cost." But, for Americans of course, when you have government footing the cost (and deficit spending), who cares?

Via WaPo, [6]

[7]

[7]

Via Bloomberg [4],

Via WaPo, [6]

[7]

[7]Via Bloomberg [4],

...

“It shows that costs can be substantially contained,” said Srinath Reddy, president of the Geneva-based World Heart Federation, of Shetty’s approach. “It’s possible to deliver very high quality cardiac care at a relatively low cost.”

Medical experts like Reddy are watching closely, eager to see if Shetty’s driven cost-cutting can point the way for hospitals to boost revenue on a wider scale by making life-saving heart operations more accessible to potentially millions of people in India and other developing countries.

“The current price of everything that you see in health care is predominantly opportunistic pricing and the outcome of inefficiency,” Shetty, 60, said in an interview in his office in Bangalore, where he started his chain of hospitals, with the opening of his flagship center, Narayana Hrudayalaya Health City, in 2001.

...

In the future, Shetty sees costs coming down further as more Asian electronics companies enter the market for CT scanners, MRIs and catheterization labs -- bringing down prices. As India trains more diploma holders in specialties such as anesthesiology, gynecology, ophthalmology and radiology, Narayana will be able to hire from a larger, less expensive talent pool.

One positive unforeseen outcome may be that many of the cost-saving approaches could be duplicated in developed economies, especially in the U.S. under health reform.

“Global health-care costs are rising rapidly and as countries move toward universal health coverage, they will have to face the challenge of providing health care at a fairly affordable cost,” said the World Heart Federation’s Reddy, a New Delhi-based cardiologist who is also president of the Public Health Foundation of India.

NSA's Utah Spy Supercenter Crippled By Power Surges

Long before Edward Snowden's whistleblowing revelations hit the world

and the Obama administration's approval ratings like a ton of bricks,

we ran a story in March 2012 which exposed the NSA's unprecedented domestic espionage project, codenamed Stellar Wind,

and specifically the $1.4+ billion data center spy facility located in

Bluffdale, Utah, which spans more than one million square feet, uses 65

megawatts of energy (enough to power a city of more than 20,000), and

can store exabytes or even zettabytes of data (a zettabyte is 100

million times larger than all the printed material in the Library of

Congress), consisting of every single electronic communication in the

world, whether captured with a warrant or not. Yet despite all signs to

the contrary, Uber-general Keith Alexander and his spy army are only human, and as the WSJ reports, the NSA's Bluffdale data center - whose interior may not be modeled for the bridge of the Starship Enterprise - has been hobbled by chronic electrical surges as a result of at least 10 electrical meltdowns in the past 13 months.

The facility above is where everyone's back up phone records and emails are stored.

Such meltdowns have prevented the NSA from using computers at its new Utah data-storage center which then supposedly means that not every single US conversation using electronic media or airwaves in the past year has been saved for posterity and the amusement of the NSA's superspooks.

This being the NSA, of course, not even a blown fuse is quite the same as it would be in the normal world: "One project official described the electrical troubles—so-called arc fault failures—as "a flash of lightning inside a 2-foot box." These failures create fiery explosions, melt metal and cause circuits to fail, the official said. The causes remain under investigation, and there is disagreement whether proposed fixes will work, according to officials and project documents. One Utah project official said the NSA planned this week to turn on some of its computers there."

More from the WSJ on this latest example of what even the most organized and efficient of government agencies ends up with when left to its non-private sector resources:

So for those who have no choice but to live in a totalitarian banana republic, may we suggest at least laughing about it. We present the Domestic Surveillance Directorate.

The facility above is where everyone's back up phone records and emails are stored.

Such meltdowns have prevented the NSA from using computers at its new Utah data-storage center which then supposedly means that not every single US conversation using electronic media or airwaves in the past year has been saved for posterity and the amusement of the NSA's superspooks.

This being the NSA, of course, not even a blown fuse is quite the same as it would be in the normal world: "One project official described the electrical troubles—so-called arc fault failures—as "a flash of lightning inside a 2-foot box." These failures create fiery explosions, melt metal and cause circuits to fail, the official said. The causes remain under investigation, and there is disagreement whether proposed fixes will work, according to officials and project documents. One Utah project official said the NSA planned this week to turn on some of its computers there."

More from the WSJ on this latest example of what even the most organized and efficient of government agencies ends up with when left to its non-private sector resources:

Tsk tsk: this is what happens when you use taxpayer dollars to pay the lowest bidder - you can't even build an efficient totalitarian superstate!Without a reliable electrical system to run computers and keep them cool, the NSA's global surveillance data systems can't function. The NSA chose Bluffdale, Utah, to house the data center largely because of the abundance of cheap electricity. It continuously uses 65 megawatts, which could power a small city of at least 20,000, at a cost of more than $1 million a month, according to project officials and documents.

Utah is the largest of several new NSA data centers, including a nearly $900 million facility at its Fort Meade, Md., headquarters and a smaller one in San Antonio. The first of four data facilities at the Utah center was originally scheduled to open in October 2012, according to project documents. The data-center delays show that the NSA's ability to use its powerful capabilities is undercut by logistical headaches. Documents and interviews paint a picture of a project that cut corners to speed building.

Backup generators have failed numerous tests, according to project documents, and officials disagree about whether the cause is understood. There are also disagreements among government officials and contractors over the adequacy of the electrical control systems, a project official said, and the cooling systems also remain untested.

The Army Corps of Engineers is overseeing the data center's construction. Chief of Construction Operations, Norbert Suter said, "the cause of the electrical issues was identified by the team, and is currently being corrected by the contractor." He said the Corps would ensure the center is "completely reliable" before handing it over to the NSA.

But another government assessment concluded the contractor's proposed solutions fall short and the causes of eight of the failures haven't been conclusively determined. "We did not find any indication that the proposed equipment modification measures will be effective in preventing future incidents," said a report last week by special investigators from the Army Corps of Engineers known as a Tiger Team.

The architectural firm KlingStubbins designed the electrical system. The firm is a subcontractor to a joint venture of three companies: Balfour Beatty Construction, DPR Construction and Big-D Construction Corp. A KlingStubbins official referred questions to the Army Corps of Engineers.

Wait, we know: it's the Syrians.The first arc fault failure at the Utah plant was on Aug. 9, 2012, according to project documents. Since then, the center has had nine more failures, most recently on Sept. 25. Each incident caused as much as $100,000 in damage, according to a project official. It took six months for investigators to determine the causes of two of the failures. In the months that followed, the contractors employed more than 30 independent experts that conducted 160 tests over 50,000 man-hours, according to project documents.

This summer, the Army Corps of Engineers dispatched its Tiger Team, officials said. In an initial report, the team said the cause of the failures remained unknown in all but two instances. The team said the government has incomplete information about the design of the electrical system that could pose new problems if settings need to change on circuit breakers. The report concluded that efforts to "fast track" the Utah project bypassed regular quality controls in design and construction.

Contractors have started installing devices that insulate the power system from a failure and would reduce damage to the electrical machinery. But the fix wouldn't prevent the failures, according to project documents and current and former officials.

Contractor representatives wrote last month to NSA officials to acknowledge the failures and describe their plan to ensure there is reliable electricity for computers. The representatives said they didn't know the true source of the failures but proposed remedies they believed would work. With those measures and others in place, they said, they had "high confidence that the electrical systems will perform as required by the contract."

A couple of weeks later, on Sept. 23, the contractors reported they had uncovered the "root cause" of the electrical failures, citing a "consensus" among 30 investigators, which didn't include government officials. Their proposed solution was the same device they had already begun installing.

So for those who have no choice but to live in a totalitarian banana republic, may we suggest at least laughing about it. We present the Domestic Surveillance Directorate.

Monday, October 7, 2013

Julian Robertson Warns "We Are In A Bubble Market" And Yellen Is "Way Too Easy Money"

"Steve Jobs was really a pretty terrible man... and I just don't believe bad guys do well in the long run,"

is the subtle way the billionaire fund managed describes the ex Apple

CEO before shifting his view to the broader market. A spell-bound Maria

Bartiromo was looking for any silver lining when Julian Robertson

responded ominously, "we're in the middle of a kind of bubble

market," and when they "prick the bubble, there will probably be a

pretty bad reaction." With views on The Fed's easy-money,

Twitter, and market frothiness, Robertson is a breath of truthy fresh

air that we suspect will not be back on the money-honey's show anytime

soon...

On Steve Jobs:

On Steve Jobs:

On The Market:"I came to the conclusion that it was unlikely that a man as really awful as I think that Steve Jobs was, could possibly create a great company for the long term.

I just don't believe bad guys do well in the long run," Robertson said.

On The Fed:...the broader market is "fully valued" and otherwise appears a little frothy.

"I think we're in the middle of a kind of bubble market, where it's going to take something bubble-like to happen to prick the bubble and will probably have pretty bad reaction to the breaking of the bubble," Robertson said.

"Probably will not [happen] right now and somehow I think we'll wallow through the political and fiscal crisis we have in front of us and then we'll sort of see what happens."

...he would not prefer Vice Chair Janet Yellen because he thinks she's "way too easy money."

Now the Chinese are wagging their fingers at Obama

October 7, 2013

Sovereign Valley Farm, Pencahue, Chile

“Diminishing Superpower”

This was the headline streaking across the weekend edition of the Jakarta Globe, one of the largest newspapers in Indonesia.

The photo beneath was of Barack Obama, his lips pursed and eyes steeled as if he was fighting back tears. Or perhaps staring off into the fiscal abyss.

The subheadline read: “Obama’s APEC absence symbolic of US waning influence in Asia.”

The article goes on to describe how the President’s conspicuous absence from this weekend’s summit of the Asia Pacific Economic Cooperation (a multinational trade bloc in the Asia/Pacific region) highlights the decline of the US as the world’s superpower.

It’s so obvious to everyone else that the US is in terminal decline.

(Granted, the Indonesians are a bit miffed given that they went to the trouble of closing the brand new airport in Bali for four days, partly because of the anticipated arrival of Air Force One… and then the President didn’t bother showing up.)

Russian President Vladimir Putin and Chinese President Xi Jinping stepped up in Obama’s stead, taking the world’s stage in yet another clear sign of where the real economic power and leadership is.

Putin himself was even nominated for the Nobel Peace Prize… for preventing a former Nobel Peace Prize recipient (Barack Obama) from starting a war Syria.

Meanwhile, China’s vice Finance Minister Zhu Guangyao has been wagging his finger at the US Treasury Department, warning that “the clock is ticking” and that Obama should “take decisive and credible steps to avoid a default on its Treasury bonds.”

All this comes at a time when the US has been caught red handed spying on the rest of the world, including its own people… and its allies. This prompted the Brazilian President Dilma Rousseff to cancel an official visit to the United States this month.

It’s amazing when you step back and look at the big picture.

The Russians are preventing a US military invasion. The Chinese actually have to step in and say something publicly to ensure that the US government pays its bills. The Brazilians are too disgusted to even visit Washington DC.

What a completely different world we live in, even compared to just 10 or 15 years ago.

Think back to the late 90s. The US really was the pinnacle of civilization. The government was beginning to pay down its debt. America’s reputation was unblemished. And to most foreigners, the US economy was the envy of the world.

What’s happening today would have been unthinkable back then. But it just goes to show how quickly things can unravel.

It’s tremendously important that the reputation of the US government is sinking to an all-time low internationally.

Remember, the reason that the US Federal Reserve can print trillions of dollars is because the rest of the world has for decades been willing to accept dollars for international transactions and sovereign reserves.

Nearly every government and central bank on the planet has a big pile of dollars stashed away.

The US government seems to think that this arrangement will last forever, and that their actions are without consequence. Nothing is further from the truth.

As the US government’s international reputation craters after one embarrassing episode after another, other nations are beginning to no longer trust the US, whether it comes to spying or managing a sound currency.

This puts the US dollar at even greater risk of quickly losing global reserve domination, and along with it, the ability to print money without damning ramifications.

As history has shown so many times before, this is exactly how the end begins.

Sovereign Valley Farm, Pencahue, Chile

“Diminishing Superpower”

This was the headline streaking across the weekend edition of the Jakarta Globe, one of the largest newspapers in Indonesia.

The photo beneath was of Barack Obama, his lips pursed and eyes steeled as if he was fighting back tears. Or perhaps staring off into the fiscal abyss.

The subheadline read: “Obama’s APEC absence symbolic of US waning influence in Asia.”

The article goes on to describe how the President’s conspicuous absence from this weekend’s summit of the Asia Pacific Economic Cooperation (a multinational trade bloc in the Asia/Pacific region) highlights the decline of the US as the world’s superpower.

It’s so obvious to everyone else that the US is in terminal decline.

(Granted, the Indonesians are a bit miffed given that they went to the trouble of closing the brand new airport in Bali for four days, partly because of the anticipated arrival of Air Force One… and then the President didn’t bother showing up.)

Russian President Vladimir Putin and Chinese President Xi Jinping stepped up in Obama’s stead, taking the world’s stage in yet another clear sign of where the real economic power and leadership is.

Putin himself was even nominated for the Nobel Peace Prize… for preventing a former Nobel Peace Prize recipient (Barack Obama) from starting a war Syria.

Meanwhile, China’s vice Finance Minister Zhu Guangyao has been wagging his finger at the US Treasury Department, warning that “the clock is ticking” and that Obama should “take decisive and credible steps to avoid a default on its Treasury bonds.”

All this comes at a time when the US has been caught red handed spying on the rest of the world, including its own people… and its allies. This prompted the Brazilian President Dilma Rousseff to cancel an official visit to the United States this month.

It’s amazing when you step back and look at the big picture.

The Russians are preventing a US military invasion. The Chinese actually have to step in and say something publicly to ensure that the US government pays its bills. The Brazilians are too disgusted to even visit Washington DC.

What a completely different world we live in, even compared to just 10 or 15 years ago.

Think back to the late 90s. The US really was the pinnacle of civilization. The government was beginning to pay down its debt. America’s reputation was unblemished. And to most foreigners, the US economy was the envy of the world.

What’s happening today would have been unthinkable back then. But it just goes to show how quickly things can unravel.

It’s tremendously important that the reputation of the US government is sinking to an all-time low internationally.

Remember, the reason that the US Federal Reserve can print trillions of dollars is because the rest of the world has for decades been willing to accept dollars for international transactions and sovereign reserves.

Nearly every government and central bank on the planet has a big pile of dollars stashed away.

The US government seems to think that this arrangement will last forever, and that their actions are without consequence. Nothing is further from the truth.

As the US government’s international reputation craters after one embarrassing episode after another, other nations are beginning to no longer trust the US, whether it comes to spying or managing a sound currency.

This puts the US dollar at even greater risk of quickly losing global reserve domination, and along with it, the ability to print money without damning ramifications.

As history has shown so many times before, this is exactly how the end begins.

Related posts:

Fed Magically Creates $180 Billion In Student And Car Loans Out Of Thin Air

Normally, we would report the change in total

consumer debt (revolving and non-revolving) in this space, but today we

will pass, for the simple reason that the number is the merely the

latest entrant in a long series of absolutely made up garbage.

It appears that in the "quiet period" of data releases, when the BLS

realized its "non-critical", pre-update 8MHz 8086-based machines are

unable to boot up the random number generator spreadsheets known as

"economic data", Ben Bernanke decided to quietly slip a modest revision

to the monthly consumer credit data. A modest revision, which amounts to a whopping $180 billion cumulative increase in non-revolving credit beginning in January 2006.

So add that to the GDP [12], to Personal Income [13], to Household Net Worth [14], to the BLS' JOLTS "data [15]", and of course, to last year's repeat revision of consumer credit data [16], as a data set, which while present, is absolutely meaningless following recent arbitrary revisions which meant all prior data contained therein was just as irrelevant.

To summarize: for whatever reason, the Fed decided to recast its entire non-revolving credit data series starting in January 2006, and has magically created $188 billion in student loan and car debt that previously "did not exist."

Old vs Revised series shown below.

[17]

[17]

For those who still opt to live in the Matrix and be treated like mushrooms, demanding to know just what the "new" fabricated, made up series implies, here it is: total consumer credit rose by$13.6 billion driven entirely by non-revolving credit, or $14.5 billion of the total, while revolving credit has now dripped for three months in a row as households continue to pay down their credit cards, better known as deleverage. In other words: using Uncle Sam as a charge card for cars and university courses, for everything else there is paying down debt.

[18]

[18]

Finally, perhaps the most amusing implication of today's revision, is the longer term chart of non-revolving credit. As the St Louis Fed chart below shows, we are about to go beyond exponential and purely asymptotic.

[19]

So add that to the GDP [12], to Personal Income [13], to Household Net Worth [14], to the BLS' JOLTS "data [15]", and of course, to last year's repeat revision of consumer credit data [16], as a data set, which while present, is absolutely meaningless following recent arbitrary revisions which meant all prior data contained therein was just as irrelevant.

To summarize: for whatever reason, the Fed decided to recast its entire non-revolving credit data series starting in January 2006, and has magically created $188 billion in student loan and car debt that previously "did not exist."

Old vs Revised series shown below.

[17]

[17]For those who still opt to live in the Matrix and be treated like mushrooms, demanding to know just what the "new" fabricated, made up series implies, here it is: total consumer credit rose by$13.6 billion driven entirely by non-revolving credit, or $14.5 billion of the total, while revolving credit has now dripped for three months in a row as households continue to pay down their credit cards, better known as deleverage. In other words: using Uncle Sam as a charge card for cars and university courses, for everything else there is paying down debt.

[18]

[18]Finally, perhaps the most amusing implication of today's revision, is the longer term chart of non-revolving credit. As the St Louis Fed chart below shows, we are about to go beyond exponential and purely asymptotic.

[19]

Stocks Slump Most In 6 Weeks As VIX Spikes Most In Over 3 Months

Weakness at the open last night extended lower during Europe's early

session - testing the 11-month trendline levels for the S&P 500. As

the US day session opened we bounced gloriously on the shoulders of

JPY-driven mania (and absolutely and utterly no news) but as usual that

lasted only as long as POMO and the markets stumbled along for the rest

of the day - until IB raised margins and then the high volume dump

started. All equity indices dived and VIX surged by its most in over 3 months above 19%.

Away from the schizophrenia in stocks, FX markets were quiet after an

early eruption in vol (USD -0.25% on the day); Treasury yields were

1-3bps lower (but off their best levels); Silver spiked near the open

(as did Gold) and held gains. Stocks close at their lows with an ugly dump.

Did IB just burst the bubble?

The S&P 500 closed below its 50DMA (down 10 of last 13 days) and is 3.5% off its all-time highs with the biggest 1-day drop in 6 weeks...

Bonds and Precious Metals outperforming post Shutdown (red line)...

VIX jumped its most in almost 4 months but was leading stocks lower earlier in the day. S&P futures are extending losses from the cash close.

Remember we are very close to that 11-month trendline break here...

The IB margin hike appeared to drive FX carry traders crazy and USDJPY collapsed (with JPY surging back below 97 to 7 week highs against the USD) - Abe will not be happy...

Charts: Bloomberg

Bonus Chart - Still think fundamentals (and not marginal leverage) drives stocks? Think again...

Did IB just burst the bubble?

The S&P 500 closed below its 50DMA (down 10 of last 13 days) and is 3.5% off its all-time highs with the biggest 1-day drop in 6 weeks...

Bonds and Precious Metals outperforming post Shutdown (red line)...

VIX jumped its most in almost 4 months but was leading stocks lower earlier in the day. S&P futures are extending losses from the cash close.

Remember we are very close to that 11-month trendline break here...

The IB margin hike appeared to drive FX carry traders crazy and USDJPY collapsed (with JPY surging back below 97 to 7 week highs against the USD) - Abe will not be happy...

Charts: Bloomberg

Bonus Chart - Still think fundamentals (and not marginal leverage) drives stocks? Think again...

The Reason For The Selloff: Microcap Traders Punk'd With 100% Interactive Brokers Margin Hike

The massive outperformance of the smallest and

most trashy companies over the past year, month, week, day etc...

stalled this afternoon. No news; no macro data; no change in the

situation in DC. So what was it? We suspect the answer lies in the all-time record levels of margin that we recently discussed holding up the US equity market. [6] Interactive

Brokers, it would appear, have seen the light and over the next week or

so will be increasing maintenance margin to 100% - effectively squeezing the leveraged momentum chasing muppets out of the market (or at the very least halving their risk-taking abilities [7]).

[8]

[8]

As we warned previously,

Margin Debt still contrarian bearish

[9]

[9]

Using closing basis monthly data, peaks in NYSE margin debt preceded peaks in the S&P 500 in 2007 and 2000. The March 2000 peak in NYSE margin debt of $278.5m preceded the August 2000 monthly closing price peak in the S&P 500 at 1517.68. The July 2007 margin debt peak of $381.4m preceded the October 2007 monthly closing price peak of 1549.38 for the S&P 500. Margin debt reached a record high of $384.4m in April and the S&P 500 continued to rally into July, August, and September. This is a similar set up to 2007 and 2000.

Bonus Chart - Margin debt: the long-term overlay

[10]

[10]

Going back to January 1959, margin debt and the S&P 500 have moved together for the most part. But leverage is a double edge sword and can exacerbate sell-offs, leading to deeper than expected market pullbacks.

Still think the "market" is driven by earnings or fundamentals? or just leverage and marginal credit expansion (shadow banking repo... etc.)?

[8]

[8]As we warned previously,

Margin Debt still contrarian bearish

[9]Using closing basis monthly data, peaks in NYSE margin debt preceded peaks in the S&P 500 in 2007 and 2000. The March 2000 peak in NYSE margin debt of $278.5m preceded the August 2000 monthly closing price peak in the S&P 500 at 1517.68. The July 2007 margin debt peak of $381.4m preceded the October 2007 monthly closing price peak of 1549.38 for the S&P 500. Margin debt reached a record high of $384.4m in April and the S&P 500 continued to rally into July, August, and September. This is a similar set up to 2007 and 2000.

Bonus Chart - Margin debt: the long-term overlay

[10]Going back to January 1959, margin debt and the S&P 500 have moved together for the most part. But leverage is a double edge sword and can exacerbate sell-offs, leading to deeper than expected market pullbacks.

Still think the "market" is driven by earnings or fundamentals? or just leverage and marginal credit expansion (shadow banking repo... etc.)?

Where Washington Should Go for Money: Havens

As the US government shutdown enters its 7th day

today it looks as if we shouldn’t be holding our breath unless we want

to go blue in the face in the hope that there might be a compromise or

somebody might actually cave in. Talk about sticking to your guns. The

Republicans won’t come out of it any better than Obama [16] will

in standing their ground and refusing to negotiate over all of this as

hundreds of thousands get laid off. So, they might have voted back pay.

But, will they also be voting that the rent and the mortgage payments

and the utility bills and the groceries also be paid at the end of the

month? Very doubtful. No point closing the gate after the horse has

bolted at all, is it Washington? If only they stopped wasting the

people’s money in their stand-off that is holding the US economy to

hostage. Getting rid of them all and starting afresh wouldn’t be a bad

idea after all. To those that might retort that the ones that follow

will be just as bad, should have faith that new brooms might be big

enough to sweep away the debris and make a thorough clear out in

politics these days.

Alternatively, if Washington is looking for money, then they could start looking where the real greenbacks are going, apart from being thrown out of the helicopter [17] to the people down below at the banks, it should be added with haste.

The top 20 US companies listed in Fortune 50 have set aside some $743 billion in profits in accounts located in offshore tax havens [19]. According to Nerdwallet Taxes that would bring in about$119 billion extra for the Treasury if the money were in the US in accounts.

Tax-haven talk only gets little more than a few Twitter comments that fall into oblivion or a televised debate at 3 a.m. in the morning that nobody watches. The companies with the offshore accounts have the politicians tied to them, since they are the ones that will make and break their political careers. Hardly going to bite the hand that feeds you, are you?

The US budget deficit stands at $642 billion. That could be reduced if the guys in Washington had the gumption to stand up and be counted and get the companies to pay taxes here in the US.

That money is offshore today and not in the USA. It is of no benefit to the country whatsoever being overseas, improving just the financial status of the companies and not the US economy. Certainly, the US budget deficit is far from their worries. But it amounts to 10% of Gross Domestic Product of the USA that is sitting somewhere in offshore profits for companies. That’s more than there should be at a time like this. In economic times of prosperity maybe it’s acceptable to do this sort of thing (but even that’s debatable).

Alternatively, if Washington is looking for money, then they could start looking where the real greenbacks are going, apart from being thrown out of the helicopter [17] to the people down below at the banks, it should be added with haste.

[18]

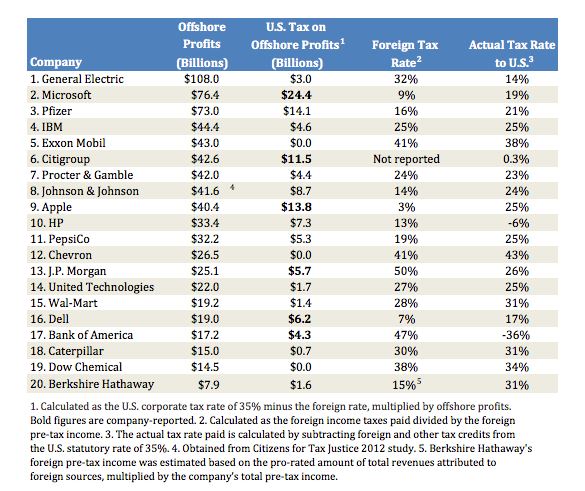

Washington: Offshore Profits?

Top 20 US Companies

The real money is in the havens, but none of the lawmakers or the politicians would ever dare mention that word for fear of alienating the few bucks that are left here in the USA.The top 20 US companies listed in Fortune 50 have set aside some $743 billion in profits in accounts located in offshore tax havens [19]. According to Nerdwallet Taxes that would bring in about$119 billion extra for the Treasury if the money were in the US in accounts.

Tax-haven talk only gets little more than a few Twitter comments that fall into oblivion or a televised debate at 3 a.m. in the morning that nobody watches. The companies with the offshore accounts have the politicians tied to them, since they are the ones that will make and break their political careers. Hardly going to bite the hand that feeds you, are you?

The US budget deficit stands at $642 billion. That could be reduced if the guys in Washington had the gumption to stand up and be counted and get the companies to pay taxes here in the US.

- 88% of the companies listed on the Fortune-50 list use tax havens to avoid paying taxes in their home country.

- 68% of offshore profits are generated by the top 10 companies on Fortune 50.

- General Electric for example has $108 billion in foreign earnings.

- Coming back to the US would bring in at least $3 billion in income tax for the US.

- Microsoft earns $76.4 offshore.

- Estimates show that it might pay anything around $24 billion in income tax to the Internal Revenue Service in the USA.

- Pfizer would end up paying $14.1 billion in tax to the IRS on its $73 billion in offshore profits.

- IBM pays $3 billion to foreign governments in taxation.

- It earns $44 billion in offshore profits and would end up paying an estimated $5 billion in the US.

[20]

Fortune 50 Companies Tax Havens

That money is offshore today and not in the USA. It is of no benefit to the country whatsoever being overseas, improving just the financial status of the companies and not the US economy. Certainly, the US budget deficit is far from their worries. But it amounts to 10% of Gross Domestic Product of the USA that is sitting somewhere in offshore profits for companies. That’s more than there should be at a time like this. In economic times of prosperity maybe it’s acceptable to do this sort of thing (but even that’s debatable).

- It’s not just the companies either; it’s private individuals and the world’s rich that have an estimated stash of $21 trillion hidden away in offshore accounts.

- By comparison, this is by far the greatest worry concerning the flight of capital from our home economies towards tax havens.

- That’s the conservative figure, since some estimate that it could be worth up to $32 trillion.

- That’s obviously more than the GDP of the USA and Japan added together.

- It’s only some 10 million people that have that money hidden away too.

- It’s not the shady banks and the wheeler-dealers of the finance world that have that money in their accounts either.

- It’s the bone fide banks of the world.

- The top banks such as Crédit Suisse and Goldman Sachs.

How long will those in Washington allow companies to sit on their stash of greenbacks while the country is running a deficit thus is in the trillions and they act as if it’s just a few bucks?

World's One-Time Largest FX Hedge Fund On Verge Of Shutdown

There is a reason why John Taylor of FX Concepts, founded in 1981 and

which once upon a time was the world's largest FX hedge fund, has kept a

very quiet profile lately despite his often bombastic prognostications

in 2011 and 2012: the firm may be on the verge of shut down following a

recent surge in redemptions resulting from woeful performance in the

past three years. FX Week reports that

AUM at FX Concepts "have continued to fall and the fund's chief

strategist confirms the board's ideas haven't worked so far." It adds

that the hedge fund is in "dangerous territory after the departure of

several major clients and falling assets under management, prompting the

firm's board to rethink its strategy, officials have confirmed." As a

result of a surge in redemptions, assets under management have declined

from a peak of $14.2 billion in 2007 to less than $1 billion this year,

having been at $4.5 billion in early 2012.

Earlier this year, FX Concepts saw the exit of two major clients – the Pennsylvania Public School Employees' Retirement System and the Bayerische Versorgungskammer pension fund – but further clients are understood to have left in recent weeks.

The culprit: the same affliction that is currently impairing all other hedge funds in a centrally-planned market - underperformance. FX Concepts' flagship multi-strategy fund is down 11.35% this year through August. It was down 14.47% in 2011 and down 3.11% in 2012. Overall, the fund's annualized returns since January 2002 are a paltry 3.74%, CNBC reports.

It also fell 14.47 percent in 2011 and lost 3.11 percent in 2012. The fund produced net annualized returns of 3.74 percent from January 2002 through this August.

FX Week adds:

The good news: the circus that are capital markets under Ben Bernanke is about to get that much funnier.

http://www.zerohedge.com/news/2013-10-07/worlds-one-time-largest-fx-hedge-fund-verge-shutdown

Earlier this year, FX Concepts saw the exit of two major clients – the Pennsylvania Public School Employees' Retirement System and the Bayerische Versorgungskammer pension fund – but further clients are understood to have left in recent weeks.

The culprit: the same affliction that is currently impairing all other hedge funds in a centrally-planned market - underperformance. FX Concepts' flagship multi-strategy fund is down 11.35% this year through August. It was down 14.47% in 2011 and down 3.11% in 2012. Overall, the fund's annualized returns since January 2002 are a paltry 3.74%, CNBC reports.

It also fell 14.47 percent in 2011 and lost 3.11 percent in 2012. The fund produced net annualized returns of 3.74 percent from January 2002 through this August.

FX Week adds:

But while Savage is hopeful that a rebound may take place and the firm will bounce back, the firm's fate may have been all but sealed when one of its last remaining large institutional clients, the San Fran Employees' Retirement System, voted on September 11 to pull its funds. CNBC's Lawrence Delevingne reports:"FX Concepts has lost a number of investors. We're still an ongoing business, but there is clearly a lot of pressure on us to rethink our strategy and come up with a way out. The performance of our headline fund has been very frustrating this year," says Bob Savage, chief strategist at FX Concepts in New York.

Savage, who joined FX Concepts a year ago after selling his research business to the firm, declined to name the latest client to leave, but confirmed that a number of major clients have been closing out their positions with FX Concepts. "We're winding down some positions in the headline fund in an organised and professional fashion," he says.

The sad but inevitable conclusion follows:"The Board approved reducing its currency overlay program target to zero percent," Huish said in an email to CNBC.com. "There is no intention at this time to redeploy the currency overlay mandate to any new currency managers."

San Francisco had more than $450 million with New York-based FX Concepts, a majority of the $661 million the firm reported managing overall in its latest Securities and Exchange Commission filing.

That redemption may have been fatal.

Sadly as more and more HFT algos move from the barren wasteland that is now stocks to dominate FX trading, yet another old-school, carbon-based investor is pulling out, meaning all those ridiculous moves we have grown to know and loathe in stocks land are about to dominate FX. The only problem is that 1000 pip moves in FX are not quite as easy to undo as a flash crash taking down any one individual stock, ETF or index to 0 or alternatively sending it to infinity.According to two people familiar with the situation, FX Concepts is in the process of liquidating its hedge funds and laid off most employees in recent weeks.

The good news: the circus that are capital markets under Ben Bernanke is about to get that much funnier.

http://www.zerohedge.com/news/2013-10-07/worlds-one-time-largest-fx-hedge-fund-verge-shutdown

Sunday, October 6, 2013

Germany’s Merkel Is Key to Currency-Trading Levy

German Chancellor Angela Merkel’s

choice of coalition partner will play a key role in deciding how far

the foreign-exchange market is burdened by a proposed

financial-transactions tax in 11 European Union states.

Merkel, who last year backed a European Commission plan for a broad-based tax on trades in stocks, bonds, derivatives and other assets, is due to start talks on forming a government with the opposition Social Democrats today. The SPD has pledged to make the delayed levy a high priority if a coalition with Merkel’s Christian Democratic bloc emerges. Currency traders are seeking an exemption from the tax, saying it would reduce liquidity and push up costs for companies and pension funds.

“Merkel is the key player and I think we’ll see Germany pushing their agenda and the other countries probably following suit,” Mark Persoff, a financial services tax partner at Ernst & Young LLP, said at the Bloomberg FX13 summit in London two days ago. “The impact on the foreign-exchange markets will obviously depend very closely on the political agreement on what the shape and scope of the FTT will be.”

The tax may increase some trading costs by as much as 4,700 percent, according to the London-based currency unit of the Global Financial Markets Association, which represents 22 firms responsible for 90 percent of the turnover in the $5.3 trillion-a-day foreign-exchange market.

Under the proposals, a levy of 10 basis points would be applied to stock and bond trades and 1 basis point on derivative transactions, with some exemptions for primary-market sales and trades with the European Central Bank.

While foreign-exchange trading for immediate delivery, so-called spot transactions, would be excluded from the levy to avoid restricting the movement of capital, the commission has not extended this exemption to other forms of currency trade. The tax, which is still under development, may be applied to forwards, swaps, non-deliverable forward contracts and options that make up two-thirds of the market.

The tax would typically increase transaction costs for currency-market participants by between 300 percent and 700 percent for corporates, and 700 percent to 1,500 percent for pension fund managers, the GFMA said. It based its estimates on a simulation of the proposed tax using last year’s currency activity by 15 end users, both within and outside the tax zone, and with annual transaction values varying between $4 billion and $400 billion. It assumed currency transaction costs to be the difference between an offer to buy a currency and an offer to sell it.

The EU Commission, the architect of the levy, says it may generate as much as 35 billion euros ($47 billion) annually. Implementing the tax was delayed six months to mid-2014 after its EU proponents failed to agree on which products to exclude.

Merkel’s Christian Democratic bloc needs a coalition partner to govern in Germany after falling short of an absolute majority as it won Sept. 22 elections with the highest share of the vote since 1990. Initial talks on a possible union with the Greens will be held on Oct. 10, Merkel’s party spokesman said on Oct. 2.

The proposals are a threat to the euro-area recovery because they may cramp businesses’ ability to hedge currency-market positions and act as a levy on trade into and out of the euro area, the GFMA says. Deutsche Bank estimates a direct cost of as much as 2.4 billion euros per year to importers and exporters in Germany, the region’s largest economy.

Lawyers for the Council of the European Union, which represents the executives of EU member states, say the tax plan goes too far and would discriminate against countries that don’t participate, according to an EU document. The legal service of the European Commission, which proposed the levy, stands by the plan and will offer a rebuttal, Emer Traynor, a spokeswoman for EU Tax Commissioner Algirdas Semeta, said on Sept. 10.

The FTT may not generate any revenue for the EU because of the damage to financial markets, ECB Governing Council member Christian Noyer said in May.

“The politicians, with the greatest of respect, need a little more education,” said Gavin Wells, chief executive officer of LCH.Clearnet Group Ltd.’s ForexClear service. “They’ve tried to raise money in a way that they don’t see the repercussions of.”

http://www.bloomberg.com/news/print/2013-10-03/merkel-is-key-to-currency-trading-levy-hsbc-says-is-terrifying.html

Merkel, who last year backed a European Commission plan for a broad-based tax on trades in stocks, bonds, derivatives and other assets, is due to start talks on forming a government with the opposition Social Democrats today. The SPD has pledged to make the delayed levy a high priority if a coalition with Merkel’s Christian Democratic bloc emerges. Currency traders are seeking an exemption from the tax, saying it would reduce liquidity and push up costs for companies and pension funds.

“Merkel is the key player and I think we’ll see Germany pushing their agenda and the other countries probably following suit,” Mark Persoff, a financial services tax partner at Ernst & Young LLP, said at the Bloomberg FX13 summit in London two days ago. “The impact on the foreign-exchange markets will obviously depend very closely on the political agreement on what the shape and scope of the FTT will be.”

The tax may increase some trading costs by as much as 4,700 percent, according to the London-based currency unit of the Global Financial Markets Association, which represents 22 firms responsible for 90 percent of the turnover in the $5.3 trillion-a-day foreign-exchange market.

Staggering, Terrifying

“The numbers are staggering,” Mark Johnson, global head of foreign-exchange cash trading at HSBC Holdings Plc, said at the event. Were the tax applied to currency derivatives called swaps, “the prospect of what it would do to people’s ability to fund is terrifying,” he said.Under the proposals, a levy of 10 basis points would be applied to stock and bond trades and 1 basis point on derivative transactions, with some exemptions for primary-market sales and trades with the European Central Bank.

While foreign-exchange trading for immediate delivery, so-called spot transactions, would be excluded from the levy to avoid restricting the movement of capital, the commission has not extended this exemption to other forms of currency trade. The tax, which is still under development, may be applied to forwards, swaps, non-deliverable forward contracts and options that make up two-thirds of the market.

The tax would typically increase transaction costs for currency-market participants by between 300 percent and 700 percent for corporates, and 700 percent to 1,500 percent for pension fund managers, the GFMA said. It based its estimates on a simulation of the proposed tax using last year’s currency activity by 15 end users, both within and outside the tax zone, and with annual transaction values varying between $4 billion and $400 billion. It assumed currency transaction costs to be the difference between an offer to buy a currency and an offer to sell it.

‘What Benefit?’

“It’s another piece of regulation that throws sand into a very efficient, well-oiled process,” said Edward Davey, managing director for strategic planning and development at CLS Bank, the operator of the world’s largest currency-trading settlement system. “You introduce new risks as well as incremental costs, and to what benefit?”The EU Commission, the architect of the levy, says it may generate as much as 35 billion euros ($47 billion) annually. Implementing the tax was delayed six months to mid-2014 after its EU proponents failed to agree on which products to exclude.

Merkel’s Christian Democratic bloc needs a coalition partner to govern in Germany after falling short of an absolute majority as it won Sept. 22 elections with the highest share of the vote since 1990. Initial talks on a possible union with the Greens will be held on Oct. 10, Merkel’s party spokesman said on Oct. 2.

‘Rational Action’

“Politics rather than rational action is crucial in this and one has to follow the politics extremely closely over the next few months,” said Oliver Harvey, a strategist at Deutsche Bank AG (DBK) in London. “The comments that come out from the next German government and the French government will begin to give us a very good idea of what sort of products will be covered.”The proposals are a threat to the euro-area recovery because they may cramp businesses’ ability to hedge currency-market positions and act as a levy on trade into and out of the euro area, the GFMA says. Deutsche Bank estimates a direct cost of as much as 2.4 billion euros per year to importers and exporters in Germany, the region’s largest economy.

Lawyers for the Council of the European Union, which represents the executives of EU member states, say the tax plan goes too far and would discriminate against countries that don’t participate, according to an EU document. The legal service of the European Commission, which proposed the levy, stands by the plan and will offer a rebuttal, Emer Traynor, a spokeswoman for EU Tax Commissioner Algirdas Semeta, said on Sept. 10.

Revenue Generation

The 11 nations planning to apply a common FTT are: Austria, Belgium, Estonia, France, Germany, Greece, Italy, Portugal, Slovenia and Slovakia and Spain, according to the commission’s website. The U.K, Denmark and Luxembourg and Sweden rejected the plan.The FTT may not generate any revenue for the EU because of the damage to financial markets, ECB Governing Council member Christian Noyer said in May.

“The politicians, with the greatest of respect, need a little more education,” said Gavin Wells, chief executive officer of LCH.Clearnet Group Ltd.’s ForexClear service. “They’ve tried to raise money in a way that they don’t see the repercussions of.”

http://www.bloomberg.com/news/print/2013-10-03/merkel-is-key-to-currency-trading-levy-hsbc-says-is-terrifying.html

Subscribe to:

Posts (Atom)