Ever taken out cash from an ATM machine and gotten socked with a $3 fee (or worse)? You probably weren't thrilled about that.

Nobody likes those fees. Except banks.

America's three biggest banks -- JPMorgan Chase(JPM), Bank of America(BAC) and Wells Fargo(WFC) -- earned more than $6 billion just from ATM and overdraft fees last year, according to an analysis by SNL Financial and CNNMoney.

That equates to $25 for every adult in the United States.

There's so much frustration over these fees that they have become a presidential campaign issue.

Hillary Clinton called ATM fees "usurious." Bernie Sanders vowed that if he's elected president, he will cap ATM fees at $2.

Consumers now pay over $4, on average, to withdraw their own money from an out-of-network ATM, according to Bankrate.

"In my view, it is unacceptable that Americans are paying a $4 or $5 fee each time they go to the ATM," Sanders said in a recent speech.

Big profits on fees

The outrage comes as Americans are finding out exactly how much banks really profit from those pesky ATM and overdraft fees. For the first time, banks were required to disclose this information publicly in 2015.

While ATM fees get the most attention on the campaign trail, overdraft charges are the most profitable for banks.

America's big three banks made over $5.1 billion last year from overdraft fees alone.

Banks aren't supposed to charge customers overdraft fees when they use an ATM to get cash unless the customer chooses or "opts in" to get the cash despite the fee.

A 2014 Pew study found more than half of the people who overdrew their checking accounts in the past year didn't remember consenting to the overdraft service.

Overdraft fees put people at 'serious risk'

"Consumers who opt in to overdraft coverage put themselves at serious risk when they use their debit card," said Richard Cordray, director of the Consumer Financial Protection Bureau.

The typical overdraft fee is $34, yet a CFPB study found that the majority of overdrafts occur on transactions of $24 or less.

"Consumers really need to look at the fine print," says Christopher Vanderpool, an analyst at research firm SNL Financial.

By law, people can opt out of ATM overdrafts at any time. That way they will not be able to take out money at an ATM if their account balance goes below $0. That said, banks can still levy a fee if someone's balance goes negative because a check is cashed or an automatic payment such as rent goes through and there aren't sufficient funds to cover it.

The CFPB study notes that if someone borrowed $24 for only three days and paid an overdraft fee of $34, that "loan" from the bank would carry a whopping 17,000% annual percentage rate (APR).

Fees are growing

Many large banks like Wells Fargo say they have put a lot of effort into clarifying their overdraft fees and helping customers make smart choices.

"Overdraft behaviors are becoming more managed by our people," said Ricky Brown, president ofBB&T(BBT) bank on an earnings call last year.

But the data for the first three quarters of 2015 doesn't back that up. It shows that overdraft fees grew every single quarter for the big banks.

CNNMoney estimated what the banks would collect on fees in the final three months of 2015. It's often the most profitable time of the year since people are doing more transactions around the holidays. Still, CNNMoney assumed that banks earned the same in the fourth quarter on fees as in the previous quarter.

The result is that JPMorgan took in $1.9 billion from customer overdrafts. Bank of America and Wells Fargo took in $1.6 billion each.

The CFPB is considering whether to implement additional rules on overdrafts.

Fees on the "regular Joe's" bank account made up about 4% of operating revenues for America's biggest banks last year, according to SNL Financial.

David Smith won’t soon forget his 38th-birthday party.

Standing on the grounds of an estate in Kingston, Jamaica, in front of a throng of some 200 investors in his foreign-exchange-trading fund, Smith listened sheepishly as his mentor and hero, Jared Martinez, compared him to Moses leading his flock to the promised land. “I wanted to buy something like the staff that Moses used to carry,” said Martinez, whose remarks have been preserved on video. “David has freed so many people down here,” Martinez told the crowd, referring to Smith’s 10 percent monthly returns. “David, we’d like to say thank you for being our Jamaican Moses.”

Smith, now 46, recalls the moment as fraught with mixed emotions, Bloomberg Marketsreports in its June 2015 issue. The charismatic Martinez, 59, who runs the oldest and largest trading school in the U.S. serving the lightly regulated $400 billion–a-day retail forex market, had grown into a trusted father figure for Smith. Under Martinez’s tutelage, Smith had succeeded in expanding his fund and increasing his personal fortune enough to afford a $2 million seaside mansion and a Learjet. Yet Smith knew he was no Moses. His fund was a fraud.

Three years later, in August 2010, U.S. prosecutors alleged Smith and his co-conspirators laundered more than $200 million of investor money through multiple U.S. bank accounts created by Martinez and two of his sons. Those transactions were the basis of 19 counts of money laundering and conspiracy against Smith, with Martinez and his sons identified as unindicted co-conspirators. Smith was also charged with four counts of fraud.

David Smith, now held in Turks and Caicos, is fighting extradition to the U.S., where he would serve out a 30-year prison sentence.

David Evans

Smith sees himself as a victim—a con man duped by another con man who proved more savvy. Smith met with aBloomberg Markets reporter in January in a detention facility on the Turks and Caicos island of Providenciales, a tourist mecca for beachgoers and snorkelers. He says he admitted guilt as part of aplea bargain with U.S. prosecutors filed in March 2011, expecting to testify against Martinez and his two sons, Isaac, now 31, and Jacob, now 34. He had already been convicted and sentenced to 6½ years in a Turks and Caicos prison and was hoping for leniency.

The Martinez family was never charged and in August 2011, a U.S. federal judge in Orlando sentenced Smith to a concurrent 30-year term. Smith is fighting extradition to the U.S. Martinez’s brokerage was fined $250,000 by the National Futures Association, a self-regulatory group, for failing to investigate Smith’s operation.

“Once I decided I’d plead guilty, there was no holding back,” Smith says, locked up just a few miles from the turquoise waters and seaside villa where he often entertained the Martinez family. “I went all the way. I did everything they asked me to do. I got nothing in return.”

Smith doesn’t deny that he committed a crime. He has confessed to defrauding some 6,000 people out of $220 million when his Ponzi scheme collapsed. He just thinks that if he has to take up residence in a U.S. prison, he should have gotten a reduced sentence in exchange for his cooperation.

Ten years ago, Martinez accepted Smith as a student at his forex-trading school outside Orlando. Martinez then followed Smith to his native Jamaica to sell classes to his investors. In classic Ponzi-scheme fashion, Smith used money from new investors to pay off his existing clients, much of it laundered through Martinez-controlled accounts, according to prosecutors. Smith contends Martinez outsmarted prosecutors by claiming he and his sons had no knowledge that they were laundering money for Smith. Martinez and his two sons declined to comment for this story. “I really felt this man was genuine, that he loved me like a son,” says Smith. “He just threw me under the bus.”

Smith’s plea agreement describes wiring more than $100 million of investor funds from Turks and Caicos to I-Trade FX, a brokerage firm he owned in Florida with the Martinez family. Cash flowed through JPMorgan Chase, Bank of America, and other banks before circling back to the Caribbean. Almost no foreign exchange was traded.

“It was a huge washing machine,” says Assistant U.S. Attorney Bruce Ambrose, who prosecuted Smith for money laundering. Yet he didn’t seek to indict Martinez family members he identified as co-conspirators. Ambrose would not explain why. The U.S. Attorney’s office later issued a statement to Bloomberg Markets saying it stands by its decision not to prosecute the family, saying Smith did not fully cooperate. Moreover, “the statute of limitations has long since expired for charging anyone who may have been involved in criminal activity with Mr. Smith,” it said.

Law enforcement agents from the U.S., Jamaica, and Turks and Caicos say that the Martinez family actively participated in Smith’s criminal enterprise, and they were stunned that U.S. prosecutors never charged the father and sons.

“It was a great case,” says Louis Skenderis, a special agent with the U.S. Department of Homeland Security, who spent three years investigating the family’s role in helping Smith move cash in and out of the U.S. “We brought David to Florida as a witness against the Martinezes, and he agreed to plead guilty as part of the deal.”

“I think David Smith is just a pawn,” says Janice Holness, executive director ofJamaica’s Financial Services Commission, interviewed at her office in Kingston. “Smith is a crook and got what he deserves, but there are bigger fish. He’s taking a fall for these people, including Jared Martinez.”

Smith turned to Martinez, founder of a forex-trading school, after his fund tanked. He says Martinez was like a father to him.

Reed Young

Martinez has said that’s simply not true. “It’s difficult to be falsely accused of anything,” he said in an October 2011 press release, two months after Smith was sentenced. “And it is unfortunate that we were perceived to be guilty by association.”

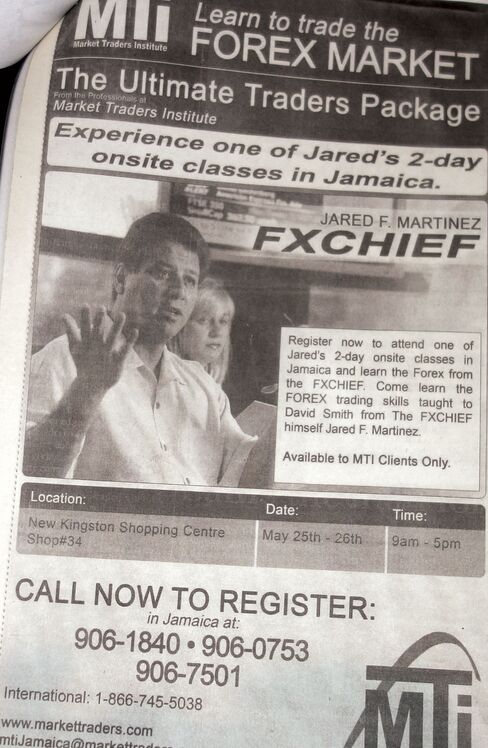

Martinez, whose Florida license plate reads “FX Chief,” says he has earned millions of dollars trading and running forex classes at his Market Traders Institute, which he founded in 1994 and which employs 115 workers. Dozens of telemarketers hawk his classes. He says he’s taught 30,000 students a formula for making consistent profits with MTI’s Ultimate Traders Package, which sells for $7,995. Yet, in an interview withBloomberg Markets last year, Martinez estimated no more than half his customers make back trading what they spend on their MTI tuition.

Martinez also said the retail forex industry is cleaner now than it was a decade ago. “Ten years ago, it was the Wild West,” he said. “Ponzi schemes were running rampant.” (See “The Currency Casino,” December 2014.)

Smith, dressed in blue gym shorts and a baggy gray T-shirt in the Providenciales police station, described how he turned from a legitimate if failed forex trader to a criminal who put all his hopes in one friendship. He grew up in a middle-class family in Kingston, the son of two high school science teachers. When he was 24, Smith took a job as a trader for a financial firm called Jamaica Money Market Brokers. While working there, he also earned a B.S. in business from Nova Southeastern University’s Jamaica campus. Two years later, in 2003, Smith was let go from the firm for what its marketing manager Kerry-Ann Stimpson describes as a breach of the firm’s “core values.” She declined to elaborate.

Smith set up a forex-trading company in 2005 called Olint, short for Overseas Locket International. Olint didn’t start out as a Ponzi scheme, he says. Smith just wasn’t very good at trading. “I lost a lot of money,” he says. “I could have declared losses and given back what was left, but I didn’t want to do that.” Instead, according to his plea agreement, he told clients that Olint accounts were earning returns averaging 10 percent a month. When the word spread, money from middle- and upper-class Jamaican investors poured in.

The losses, though, were piling up. “I stopped trading totally and started looking for education,” Smith says. Searching the Web, he discovered Martinez’s MTI. Smith flew to Orlando in April 2005 to take MTI’s four-day course, which promised to show students how to predict currency-trading patterns with “technical analysis”—reading and interpreting charts of, say, the dollar versus the euro’s past behavior.

When Martinez, who was born on the Blackfeet American Indian reservation in Montana, learned that Smith ran his own investment firm, he and Isaac approached Smith about forming a partnership, Martinez later told regulators. In February 2006, Smith invested $1 million to help fund I-Trade FX, the Martinez family’s new Florida-based forex brokerage.

Smith’s operation in Jamaica, run from a shopping mall storefront in downtown Kingston, was bustling. Olint was organized as an exclusive private club that accepted only new investors referred by members. Early investors received monthly e-mailed statements showing returns as high as 12 percent. To manage withdrawals, Smith says, he would decide returns to be paid each month. He would drag out payments during periods when requests for withdrawals increased. If plenty of new money was coming in, he would lower the return for that month. If withdrawals were rising, he would increase it in an effort to hold on to investors.

In March 2006, Smith’s scheme nearly unraveled. Following a tip by an investment banker, police and agents from Jamaica’s Financial Services Commission executed search warrants at Olint’s office, hauling off documents, cash, and computers, including a Bloomberg terminal. A cease-and-desist order banning Olint from opening new accounts soon followed from the FSC.

Smith invited nervous investors to pull out even though he knew he didn’t have enough to pay everyone. The gambit worked, quashing press reports that Olint was a Ponzi scheme. “The money flew back in,” quickly tripling Olint’s assets, Smith says. “If I’d gotten requests for another $1.1 million, I couldn’t have paid it,” he says.

Advertising in Jamaican newspapers, Martinez invited investors to learn the same forex-trading skills he taught Smith.

No criminal charges were filed against Smith in Jamaica. That might have to do with the money he was spreading around the island in campaign contributions for local politicians—many of whom were also investors. Smith gave away more than $8 million of client money, according to court documents, including $5 million to the Jamaica Labour Party and $2 million to its rival, the Jamaican People’s National Party, which now controls the government. While the JLP says only its candidates received contributions from Smith, the PNP acknowledges receiving direct contributions.

Peter Bunting, the investment banker who brought the case to the attention of the police and who now serves as Jamaica’s national security minister, says Olint investors represented a who’s who of Jamaica, including politicians, businessmen, and judges. “The enmeshment with the official system was very substantial,” Bunting said at his Kingston office in February.

Olint needed to find an alternative to the Jamaican bank accounts that had been used to receive investor deposits, according to Smith’s plea agreement. A week after the cease-and-desist order, Martinez and his son Isaac, who served as president of the brokerage, asked the NFA to license I-Trade FX. The regulator awarded I-Trade a brokerage license in August 2006, and Smith began transferring funds to the firm.

Martinez, meanwhile, began conducting forex-trading seminars in Jamaica, capitalizing on the island’s buzz around Smith and Olint. Dominic Azan, who became MTI’s Jamaica sales manager, still remembers the electricity he felt in the summer of 2006 listening to Martinez onstage, his audience in thrall, as he talked up the trading success of MTI graduates. Azan felt reassured about the $1 million he and his family had invested in Olint— nearly all of which was later lost. “Who didn’t want to be part of it? Here’s the guru, the FX Chief himself, the guy who taught David how to trade,” says Azan, who recalls admiring Martinez’s Breitling watch collection and gleaming Rolls-Royce.

Martinez made the most of his opening: “TURN $2,000 INTO $10,000 in Twenty Days. Learn How!” urged an MTI advertisement in a Jamaican newspaper in September 2006. Students lined up for classes paid for by Smith: Olint paid $1.9 million to MTI for investors’ seminars, according to a report prepared for the Turks and Caicos government by PricewaterhouseCoopers. The result was a faithful following who believed so deeply in Smith and Martinez that they were willing to entrust their life savings to the pair. Smith says there is no doubt Martinez was aware of his scam. “He knew the money wasn’t being traded, and yet I was paying people 10 percent a month,” says Smith. “He knew it was a lie.”

Martinez later testified before the NFA that he was aware of David’s regulatory problems in Jamaica and had had more than 500 conversations about them. Still, he said he found nothing suspicious about Smith before the Ponzi scheme collapsed in 2008. “We did a substantial amount of due diligence,” Martinez told the NFA, which began a probe of I-Trade FX in 2007. He said he never asked to see proof of Smith’s returns. “Some people, especially Jamaicans, they can be very offended by that,” he explained.

Regulators have suggested Martinez should have known better. “Advertised returns of the magnitude Smith claimed are often fraudulent,” the NFA wrote in an April 2009 ruling. “I-Trade should have questioned them.”

Smith fled Jamaica’s regulatory heat in the summer of 2006, relocating 400 miles (644 kilometers) northeast to Turks and Caicos, where he used investors’ money to buy his family’s waterfront home on Providenciales. He also set up two new investment clubs to raise cash, which he wired to I-Trade in Florida.

In March 2007, the Martinez family opened JIJ Investments, a hedge fund incorporated in Florida as “an alternative depository” outside the purview of the NFA, according to Smith’s plea agreement. “Unindicted co-conspirators are the listed directors of the firm,” according to the criminal complaint. JIJ Investments’ directors were Jared, Isaac, and Jacob.

The Martinez family wired $76 million from I-Trade to its JIJ accounts at JPMorgan, Bank of America, and Wachovia Bank, later purchased by Wells Fargo. Each wire transfer was described as money laundering in the criminal complaint against Smith. None of the banks was accused of any wrongdoing.

While Smith operated from Turks and Caicos, the families remained close, according to NFA testimony by Isaac, who often stayed at Smith’s island house. “His kids called me Uncle Isaac,” he said. “I would fly with him on his private jet.” Smith says he and Isaac enjoyed deep-sea fishing for yellowtail snapper. Isaac told the NFA that he never knew about Smith’s illegal activities.

The good times ended in July 2008 when the Turks and Caicos police executed a search warrant at Smith’s home and office in Providenciales. Olint and its victims were the talk of the island.

Dominic’s father, Khaleel Azan, says he and Martinez often dined together. He says he appealed to Martinez in late 2007, when he couldn’t withdraw the family’s $1 million from Olint. “Jared told me, ‘I promise, we have over $100 million from David. I’ll make sure you get your money.’” But the family’s investment was lost.

Chris Walker, an obstetrician in Orlando, says Martinez introduced Smith as 'the best student he's ever had.'

Jeffrey Salter

Chris Walker, an Orlando obstetrician, also lost more than $1 million investing with Olint, and his father, Kenneth Walker, lost $1.5 million—his life savings. Chris Walker met Smith at a forex-trading seminar conducted by Martinez in Jamaica. He recalls Martinez ushering Smith up onto a podium in front of hundreds of attendees, at a hotel in Ocho Rios. “Jared introduced David like the Messiah, as the best student he’s ever had,” says Walker. He says he poured more cash into Olint after the seminar. “Jared is a very effective salesman,” Walker says.

Walker later sued Smith, as well as Martinez and his sons, in Florida state court, alleging fraud, but says he gave up after running out of money. “It boggles my mind why the Martinez family did not get indicted,” he says. “Why aren’t the co-conspirators behind bars?”

Smith was arrested in February 2009. In April 2009, I-Trade was fined $250,000 by the NFA for failing to sufficiently investigate suspicious activity by several customers, including Smith. A month later, I-Trade shut down, though Martinez’s forex school is still in business. In 2010, Isaac, as president and compliance officer of the firm, wasfined an additional $50,000 for failure to supervise. Jacob, meanwhile, was bannedfrom the industry for three years in 2012 and ordered to pay a $150,000 fine should he seek to return to the industry.

Smith didn’t get off so easily. In 2010, he was convicted of Ponzi-related crimes in Turks and Caicos. In March 2011, he pleaded guilty in a federal court in Orlando, resulting in his 30-year prison term.

“I’m really shocked the Martinez family has escaped U.S. prosecution for a massive money-laundering exercise,” says Mark Knighton, the retired head of the Turks and Caicos financial crimes unit, who ran the island’s investigation of Olint. “We certainly had the evidence.”

On Jan. 23, in a surprise to the U.S. Department of Justice, Smith was released two years early from his Turks and Caicos prison cell. He spent that night with his wife, Tracy, and their four children, ages 5 to 13. It was the first time in four years the family had been together. “I am enjoying the moment right now,” he said in a telephone interview amid the excited screams of his kids. “I don’t know when they’re going to come and get me.”

Less than 24 hours later, Smith was taken back into custody at the request of the Justice Department. The U.S. will present its case for extradition at a hearing on Providenciales on June 5. It could be a long time before David Smith goes home again.

On February 25, 1863, President Abraham Lincoln signed the National Banking Act (originally known as the National Currency Act), which for the first time in American history established the federal dollar as the sole currency of the United States. On the law’s 150th anniversary, explore eight surprising facts about American money.

1. The Constitution only authorized the federal government to issue coins, not paper money. Article One of the Constitution granted the federal government the sole power “to coin money” and “regulate the value thereof.” However, it said nothing about paper money. This was largely because the founding fathers had seen the bills issued by the Continental Congress to finance the American Revolution—called “continentals”—become virtually worthless by the end of the war. The implosion of the continental eroded faith in paper currency to such an extent that the Constitutional Convention delegates decided to remain silent on the issue.

2. Prior to the Civil War, banks printed paper money. For America’s first 70 years, private entities, and not the federal government, issued paper money. Notes printed by state-chartered banks, which could be exchanged for gold and silver, were the most common form of paper currency in circulation. From the founding of the United States to the passage of the National Banking Act, some 8,000 different entities issued currency, which created an unwieldy money supply and facilitated rampant counterfeiting. By establishing a single national currency, the National Banking Act eliminated the overwhelming variety of paper money circulating throughout the country and created a system of banks chartered by the federal government rather than by the states. The law also assisted the federal government in financing the Civil War.

3. Foreign coins were once acceptable legal tender in the United States. Before gold and silver were discovered in the West in the mid-1800s, the United States lacked a sufficient quantity of precious metals for minting coins. Thus, a 1793 law permitted Spanish dollars and other foreign coins to be part of the American monetary system. Foreign coins were not banned as legal tender until 1857.

The $100,000 bill, printed between 1934 and 1935.

4. The highest-denomination note ever printed was worth $100,000. The largest bill ever produced by the U.S. Bureau of Engraving and Printing was the $100,000 gold certificate. The currency notes were printed between December 18, 1934, and January 9, 1935, with the portrait of President Woodrow Wilson on the front. Don’t ask your bank teller for a $100,000 bill, though. The notes were never circulated to the public and were used solely for transactions among Federal Reserve banks.

5. You won’t find a president on the highest-denomination bill ever issued to the public. The $10,000 bill is the highest denomination ever circulated by the federal government. In spite of its value, it is adorned not with a portrait of a president but with that of Salmon P. Chase, treasury secretary at the time of the passage of the National Banking Act. Chase later served as chief justice of the Supreme Court. The federal government stopped producing the $10,000 bill in 1969 along with these other high-end denominations: $5,000 (fronted by James Madison), $1,000 (fronted by Grover Cleveland) and $500 (fronted by William McKinley). (Although rare to find in your wallet, $2 bills are still printed periodically.)

Confederate currency featuring George Washington.

6. Two American presidents appeared on Confederate dollars. The Confederacy issued paper money worth approximately $1 billion during the Civil War—more than twice the amount circulated by the United States. While it’s not surprising that Confederate President Jefferson Davis and depictions of slaves at work in fields appeared on some dollar bills, so too did two Southern slave-holding presidents whom Confederates claimed as their own: George Washington (on a $50 and $100 bill) and Andrew Jackson (on a $1,000 bill).

7. Your house may literally have been built with old money. When dollar bills are taken out of circulation or become worn, they are shredded by Federal Reserve banks. In some cases, the federal government has sold the shredded currency to companies that can recycle it and use it for the production of building materials such as roofing shingles or insulation. (The Bureau of Engraving and Printing also sells small souvenir bags of shredded currency that was destroyed during the printing process.)

8. The $10 bill has the shortest lifespan of any denomination. According to the Federal Reserve, the estimated lifespan of a $10 bill is 3.6 years. The estimated lifespans of a $5 and $1 bill are 3.8 years and 4.8 years, respectively. The highest estimated lifespan is for a $100 bill at nearly 18 years. The federal government reports that approximately 4,000 double folds (forward, then backward) are required to tear a note.

David Bowie was known for his ability to reinvent himself. But he also helped inspire a pocket of Wall Street that tries to create money out of weird things like billboard rental income, cellphone tower lease payments and literary or film libraries.

In 1997, Mr. Bowie bundled up nearly 300 of his existing recordings and copyrights into a $55 million security that paid the buyer — Prudential Insurance Company of America — a 7.9 percent annual rate over 10 years, backed by the income from his royalties and record sales, and the licensing of his songs for films or other uses.

The so-called Bowie bonds were among the first in what would become a wave of esoteric asset-backed securities deals based on intellectual property, including a more recent one involving Miramax’s film library(including titles like “Pulp Fiction” and “The English Patient”). Bankers have also come up with securities backed by franchise revenue for the restaurant chains Sonic and Church’s Chicken, among others.

The buyers in these deals, which are negotiated privately by the banks that put the transactions together, tend to be specialized hedge funds or big institutions that can negotiate terms with the bankers. Individual investors never got their hands on a Bowie bond because Prudential never sold any of its stake.

A Prudential spokesman declined to comment.

At the time it was a good deal for Mr. Bowie. He got upfront cash for a decade’s worth of royalty and licensing revenue without having to give up ownership of his songs.

Originally rated A3 by Moody’s Investors Service, Bowie bonds were later downgraded to Baa3, just above junk status. By the early 2000s, Internet file sharing had become a factor, and musicians were generating less income because album sales were declining.

Still, Mr. Bowie’s Wall Street collaboration inspired other celebrities to cash in while the getting was still good. Edward Holland, Brian Holland and Lamont Dozier, the Motown hit songwriters, did a deal, as did James Brown and Rod Stewart. In 2002, DreamWorks SKG entered into a $1 billion deal involving its film catalog.

Most asset-backed securities are secured by income generated from mortgages, credit card loans and auto loans. But mortgage-backed securities gave the sector a bad name during the financial crisis and investors backed off for a while.

Issuance of asset-backed securities dropped 16.6 percent last year, to $184 billion, with a steep drop off in deals backed by credit card loans, according to the Securities Industry and Financial Markets Association.

Deals backed by unusual assets make up about a tenth of the asset-backed security market, appealing to investors who want higher yields and are willing to take on more risk.

“There’s a nonanalytic aspect to these deals that makes them riskier,” says Sylvain Raynes, a founder of R&R Consulting who worked at Moody’s at the time the Bowie bond was being rated.

Wall Street's industry-funded watchdog is ramping up its scrutiny of high-frequency trading firms as efforts to manipulate U.S. markets through the technology grow more sophisticated, the regulator's chief said on Tuesday.

The Financial Industry Regulatory Authority will examine how well high-frequency trading firms are protecting their systems from unscrupulous traders who are trying to manipulate markets, according to a list of its 2016 examination priorities for Wall Street firms, published on Tuesday.

High-frequency trading is an automated strategy that can move billions of dollars worth of trades in a fraction of a second.

FINRA's heightened focus on controls in place at high-frequency trading firms coincides with the growing prevalence of a new and more complex form of spoofing, a type of manipulation that involves faking orders for a security to deceive the market by creating the illusion of demand, said Richard Ketchum, FINRA's chairman and chief executive, in an interview.

The regulator is observing more instances in which traders are using multiple firms to place those orders, Ketchum said. The strategy can make the conduct trickier to track.

Spoofing occurs when traders place orders in markets without intending to execute them. The traders immediately cancel the orders, but other market participants mistakenly believe the price of the security has moved.

Wall Street's industry-funded watchdog is ramping up its scrutiny of high-frequency trading firms as efforts to manipulate U.S. markets through the technology grow more sophisticated, the regulator's chief said on Tuesday.

The Financial Industry Regulatory Authority will examine how well high-frequency trading firms are protecting their systems from unscrupulous traders who are trying to manipulate markets, according to a list of its 2016 examination priorities for Wall Street firms, published on Tuesday.

High-frequency trading is an automated strategy that can move billions of dollars worth of trades in a fraction of a second.

FINRA's heightened focus on controls in place at high-frequency trading firms coincides with the growing prevalence of a new and more complex form of spoofing, a type of manipulation that involves faking orders for a security to deceive the market by creating the illusion of demand, said Richard Ketchum, FINRA's chairman and chief executive, in an interview.

The regulator is observing more instances in which traders are using multiple firms to place those orders, Ketchum said. The strategy can make the conduct trickier to track.

Spoofing occurs when traders place orders in markets without intending to execute them. The traders immediately cancel the orders, but other market participants mistakenly believe the price of the security has moved.

The last time FX brokers, still hurting from the Swiss National Bank's revaluation shocker from last January which forced brand names such as FXCM to seek an urgent bailout, scramble to hike margins was in late June just ahead of the Greek "event risk" weekend, when numerous brokers either hiked margins on EUR positions or went to "close only" mode due to "uncertainty surrounding the Greek debt negotiations... that could lead to high volatility on the market."

So, barely one week into the new year, one which has seen the stock market suffer its worst ever first week of trading, some FX brokers are not taking chances, and in the aftermath of the aggressive plunge in the Yuan (one we warned about a month ago), have decided to minimize client stop-out risk by hiking margins.

Case in point, here is FXCM with a just released warning about upcoming "highly illiquid conditions" leading to a doubling in Yuan margins:

Dear Client,

We believe there is a chance of disruption and highly illiquid conditions in the forex market during the coming weeks (and/or months). Please be aware that market gaps tend to occur over the weekend – that is, currencies trade at prices considerably distant from previous levels.

Please review your account to ensure that you have enough available margin to support any new positions. You may deposit additional funds at www.myfxcm.com or close positions as needed.

Follows the traditional disclaime which FXCM itself probably should have taken to heart one year ago when after the SNB's de-pegging the firm suffered tremendous losses:

Remember that forex trading can result in losses that could exceed your deposited funds and therefore may not be suitable for everyone, so please ensure that you fully understand the high level of risk involved.

The paradox here is that pre-emptive, if correct, warnings such as this one, tend to quickly become self-fulfilling prophecies as other brokers immediately follow suit and likewise increase margin requirements, which helps mitigate total loss potential but just as quickly soaks up liquidity from the market, leading to an even more fragmented market, prone to sudden, and quite dramatic moves.

The full list of FXCM margin increases is shown below; expect every other FX brokerage to promptly jump on the bandwagon.

EES: As explained by this white paper, transactions that include the US Dollar can be subject to US laws and regulations even if done outside the United States. For this reason, certain FX hedge funds do not trade USD pairs. From law firm White & Case:

Means or Instrumentality of Interstate Commerce Many US laws — including the Foreign Corrupt Practices Act (FCPA) in certain circumstances and various antifraud statutes — may establish jurisdiction over a crime whenever it involves the use of any "means or instrumentality of interstate or foreign commerce." The term is broadly defined by US authorities and may cover any communication or movement that crosses state or international borders, including wire transfers, emails, phone calls, mail and travel. Given the reach of US commerce, from free email servers to correspondent banks that clear US dollars for non-US based banks, such a broad definition can significantly increase the reach of US law. Furthermore, according to US authorities, a defendant company or individual need not use the means or instrumentality of interstate commerce themselves — it may be enough for them to have "caused" the use, such as an instruction being sent to one person, who then forwards it to another, through email servers in the United States.

“

Conspiracy Conspiracy law may subject non-US companies or individuals who have not committed an act within the United States to US criminal jurisdiction. Under long established principles of criminal liability, a conspirator may be liable for a coconspirator's acts, as well as for any "reasonably foreseeable" offenses committed by a coconspirator. If the United States can establish jurisdiction over a single conspirator, it may have jurisdiction over all conspirators, whether companies or individuals, wherever they may be found.

In certain circumstances, a conspirator need not have participated in or even known about the underlying criminal offense committed by a coconspirator to be liable. Moreover, unlike conspiracy law in some other countries, under US criminal law, a company can "conspire" with its employees, so corporate crime in the United States may result in a prosecutable conspiracy.

Agent Liability A company or an individual also may be prosecuted under some US laws, if the company or individual is found to have acted as the "agent" of a company or individual that falls under US jurisdiction. For example, a Japanese trading company was recently prosecuted for violating the FCPA's anti-bribery provisions as the "agent" of a US company, even though the trading company did not act within the United States. A company potentially also may be liable for third parties' actions if those third parties acted on the company's behalf and for the company's benefit. Similarly, under the principle of respondeat superior, a company employee who is acting within the scope of his or her employment, and for the benefit of the company, is considered an agent of the company. If they commit a crime connected to their employment, the company may be criminally liable as well.

"Piercing the Veil" A company may be liable for another's conduct under the corporate liability principles of "alter ego" or "piercing the veil". For example, a parent company may be liable for its subsidiary's acts if it can be shown that the subsidiary was acting as the "alter ego" — or under the control of — the parent. If a subsidiary outside the United States is determined to be an "alter ego" of the parent, US authorities may be able to "pierce the veil" of legal separation between the companies, and, if so, the foreign company's actions can be treated as if they were committed by the US company. Once an alter ego relationship is shown to exist, either in general or in a specific instance, the subsidiary's conduct and knowledge may be attributed to the parent.

Following the Money: Money laundering and sanctions US law makes it a criminal offense to engage in or attempt to engage in a financial transaction involving funds that are known to be the proceeds of certain unlawful activities, or to engage in a financial transaction that provides funds for the commission of a crime (such as terrorist financing or sending a bribe payment). This offense is called "money laundering," and non-US corporations and foreign nationals may be subject to prosecution under US federal anti-money laundering statutes if they are involved in the transfer or attempted transfer of illegally obtained funds or funds used to further criminal activity.

Money laundering offenses can be as serious as the underlying offenses they promote. Each financial transaction can be considered a separate offense and is punishable by substantial fines and possible imprisonment. Additionally, funds and other property involved in money laundering may be frozen or seized by US enforcement authorities, or subject to forfeiture.

In prosecuting money laundering offenses, the US Department of Justice takes the position that jurisdiction exists over a financial transaction if the laundering is completed by a US citizen anywhere in the world, or by a foreign national or non-US corporation if the criminal conduct occurs in part in the United States—even if the foreign individual or company never themselves took an action in the United States, or intended for an act to occur there.

This broad jurisdiction can greatly expand the reach of the US money laundering statutes. For example, US corporations and individuals potentially may be prosecuted for money laundering offenses involving financial transactions that occur wholly outside the United States. US courts have held that the financial transaction requirement is satisfied for a wholly foreign transaction if the defendant's conduct "affected" foreign commerce with the US — such as in antitrust matters. Virtually every dollar-denominated transaction potentially implicates US commerce with other nations. While there does need to be an actual US nexus for money laundering laws to apply — the dollars being cleared through a US correspondent bank, for example — and there are dollar-denominated transactions that have no such tie, US enforcement authorities increasingly operate on the assumption (unless convinced otherwise) that they have jurisdiction for such offenses whenever a suspect transaction is denominated in US dollars.

The jurisdiction potentially created by clearing US dollars through a US bank can also significantly extend the reach of US sanctions laws. Sanctions can prohibit or restrict doing business with countries (such as Cuba, Sudan, and Iran), individuals or companies referred to as "specially designated nationals" or "SDNs," which are 'blocked' parties subject to a US asset freeze, and entities placed on the "Sectoral Sanctions Identifications List" (SSI List), as in the case of the Ukraine-related sectoral sanctions. Sanctions regimes typically cover all "US persons," but what qualifies as a US person may change from one sanctions regime to the next, as each set of sanctions varies slightly. Generally, it includes any US citizen or permanent resident and any US company, wherever they are in the world, as well as any person physically in the United States. In addition, in certain instances US sanctions may reach non-US subsidiaries of US companies. This may mean that the clearing of dollars through a US bank may be enough to create US jurisdiction over subject transactions.

The location of funds outside the United States does not necessarily mean they are beyond the reach of US enforcement authorities. Under US law, the proceeds of criminal offenses — including some offenses that occur entirely overseas — may be subject to forfeiture and may be frozen and eventually seized by US authorities through forfeiture actions initiated in US courts. With a judgment of forfeiture issued by a US court in hand, US authorities may be able to freeze not only funds located in US bank accounts, but also funds deposited in foreign bank accounts in view of the increasing cooperation among and between enforcement authorities in different countries.