Over the weekend the world learned of the Senate Republican’s “opening bid” for the next round of fiscal stimulus in the United States. That number came in at a nice, round $1tn. Now, as large as that number is, it still pales in comparison to the $3.5tn House bill that already passed. Importantly, the Senate’s version of stimulus is rather light on some Democrat “must haves” like state and local aid, for example. That is to say, there is quite a chasm between the Senate and House versions of the next round of stimulus. How might investors interpret this chasm and what is the likely resolution?

It’s clear the authorities are still in “whatever it takes” mode, so a compromise does appear to be the most likely scenario as opposed to a breakdown in talks. This is especially so since unemployment remains high and leading indicators of unemployment like initial claims appear to be ticking up again. It’s also clear the House will not get its $3.5tn wish list. So at what level might we find a middle ground?

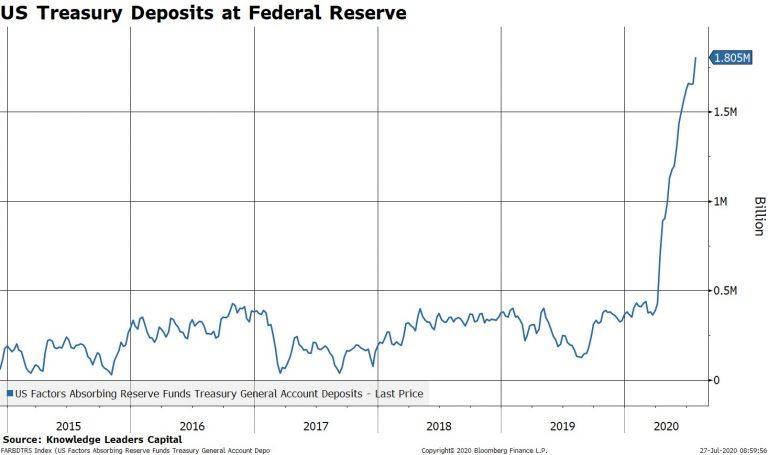

For that, we think the US Treasury Department’s deposits at the Federal Reserve is a good place to start. US Treasury deposits at the Fed is essentially the Treasury’s checking account balance. It’s money that has already been “raised” (AKA printed). It currently stands at $1.8tn vs a normal run rate balance of $400bn on the high side. This implies that $1.4tn is already sitting on the sidelines in the Treasury’s checking account ready to be deployed. In other words, the Treasury has capacity to spend $1.4tn without having to issue more debt. Therefore, this seems like a reasonable dollar amount for the next stimulus package.

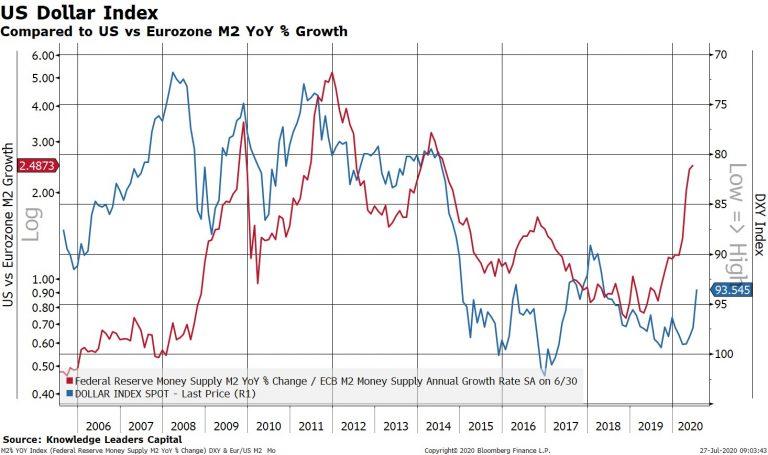

Regardless of the actual number though, what is clear is that deploying that money will increase the money supply even further, even if the velocity (i.e. circulation rate) is still low. That fact is likely to keep the US money supply growing at a faster rate than Eurozone money supply, even with the recent Eurozone stimulus announcement. The relative money supply growth between the US and Eurozone has been a good coincident indicator of the US dollar index, since that index is weighted nearly 60% towards the euro. As of this writing the US dollar index is trading at multi-year lows.

The likely $1tn stimulus plan will also serve to widen the US government’s budget deficit even further, possibly to 20% of GDP. The US budget deficit as a percent of GDP is highly correlated with the level of the US dollar index.

So, we can say with at least a decent level of confidence that the stimulus round in the offing is US dollar bearish. The magnitude of any weakness is a different story and harder to establish ex-ante given the number of variables involved. Of course, the possibility of more than transitory US dollar weakness appears to be growing.

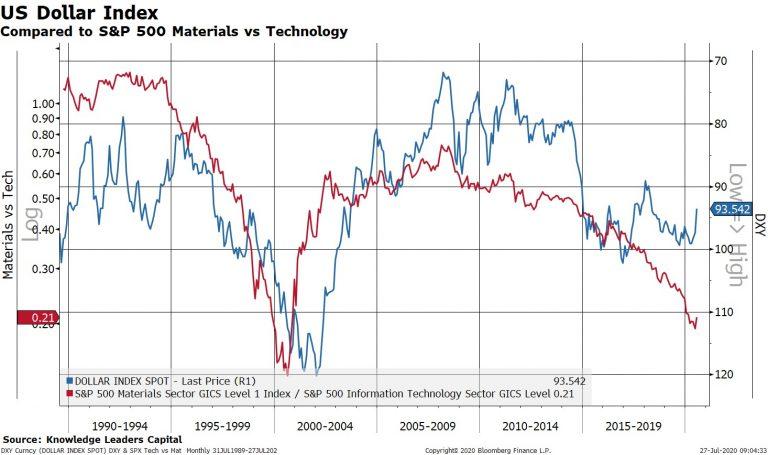

What would it mean for stock market leadership if the US dollar does truly and meaningfully depreciate? It would most likely spell the end of technology leadership and usher in leadership of a different, forgotten group: materials.

The chart above overlays the US dollar index (blue, right, inverted) against the relative performance of materials vs technology (red line, left). A falling US dollar is highly correlated with materials companies outperforming technology companies. We’re seeing a very, very slight turn in the relative performance differential. Is it the beginning of a new trend or yet another false start?

As far as Bank of America is concerned, there are just two themes one needs to know to explain the current "market" (which as the same Bank of America explained last week, is now manipulated to a never before seen extent): the Great Repression and Great Debasement.

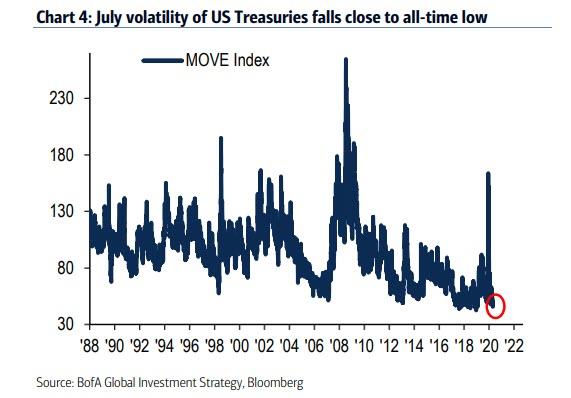

First the Great Repression - also known as "Don't fight the Fed" - which according to BofA CIO Michael Hartnett is the outcome of $8 trillion in central bank asset purchases in just three months in 2020, has crushed interest rates, corporate bond spreads, volatility & bears. The most perfect example of this repression: the US fiscal deficit soared from 7% to 40% of GDP in Q2’20...

... and less than one month later the volatility of US Treasury market fell close to all-time low.

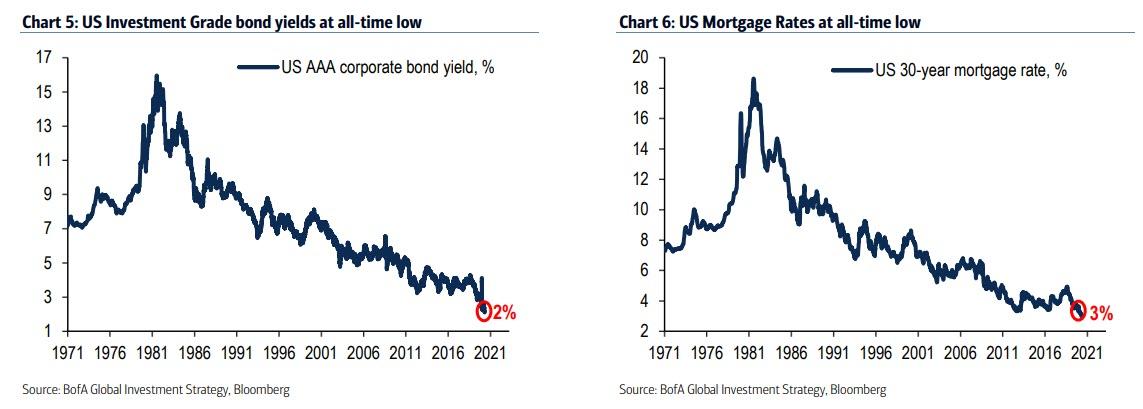

Besides volatility, central bank repression works its magic on yields: case in point Italian & Greek 10-year government bonds which are down to 1%, while US Commercial Mortgage Backed Securities (CMBS) & IG corporate bonds down to 2%, meanwhile the 30-year US mortgage rate just dropped to a record all time low of 3%.

As a result of this unprecedented repression (of reality), the Fed has made everyone a winner:

Fed has made bulls in every asset class a winner…gold, bonds, credit, stocks, real estate all up big since March lows; levered cross-asset risk parity strategy at all-time high.

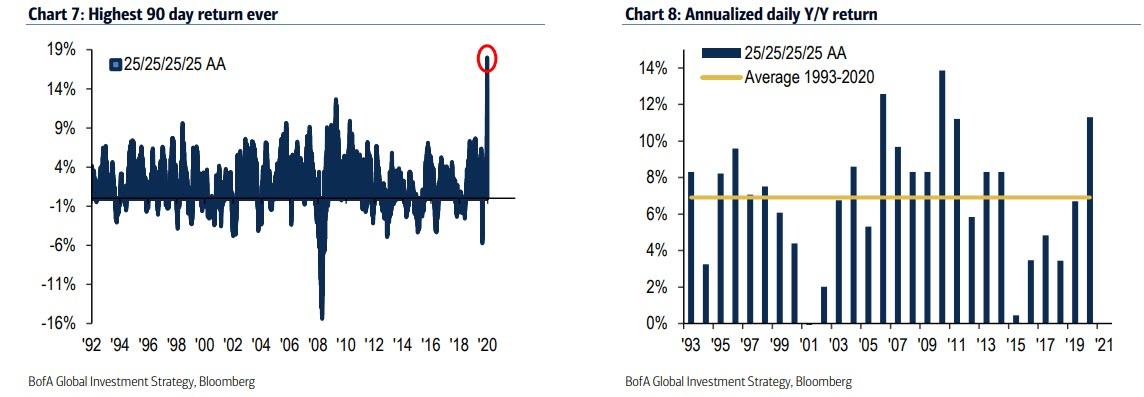

It also means that BofA's recently preferred "All-weather" portfolio consisting of equal parts of all assets, i.e., 25/25/25/25 stocks, bonds, cash, gold, is up a record 18% in the past 90 days (Chart 7), which is "astounding & abnormal" given 7% historic annual average.

This "can't lose" market has also led to fundamental shift in the zeitgeist, as the traditionally bearish narratives of Q2 such as a Democratic sweep, end of globalization, Japanification, narrow “lockdown” leadership of growth stocks is paradoxically morphing into bullish narratives. Here, Hartnett reminds is that "when the only reason to be bearish is there is no reason to be bearish" that's when you sell. And sure enough, recent market moves justify getting defensive: the global equity market cap has round-tripped from $89tn to $62tn back to $87tn, with BofA warning that it is "hard to see financial conditions getting incrementally easier in July/Aug period of “peak policy” stimulus; summer dip in risk assets (e.g. SPX to 3050) likely."

And yet, all good times come to an end - otherwise the Fed would have printed its way to utopia decades ago - and the with Great Repression in full force, it also means that the Fed is currently pursuing a just as Great Debasement.

Echoing something we have also said, namely that with the bond market now nationalized by the Fed and no longer providing any useful inflationary (or deflationary) signals, the only remaining asset class with any sort of discounting qualities is gold...

... Hartnett writes that interest rate repression means "investors can't hedge the inflationary risk of $11tn of fiscal stimulus via "short bonds"…so investors crowding into "short US dollar", "long gold" hedges.

Indeed, US dollar debasement is well underway as the default narrative for US economy with excess debt, insufficient growth, and maxed-out monetary & fiscal stimulus. However, local currency debasement is also underway everywhere else, and so the next market crisis will lead to an even bigger spike in the dollar as global monetary authorities are faced with an even bigger global synthetic short squeeze than the one which sent the USD soaring to all time highs in March.

Which is why shorting the dollar to hedge debasement may be profitable for a while but eventually lead to catastrophic consequences.

That leaves long gold as the only natural hedge to the central bank "all in" bet of kicking the can until something breaks. That something will likely be gold exploding higher first above $2,000... then $2,500... then $3,000 at which point the Fed's control over fiat currencies, as well asthe illusion that there is no inflation, and the financial regime will finally collapse.

As Hartnett condludes, "the correct historical analog is the late-1960s when themes of “smaller world”, “bigger government”, “monetary & fiscal excess” led to positive nominal returns but also inflection up in inflation.

Secular market trend has been deflation (credit & tech) dominating inflation…$100 of EPS in 1995 now $1,500 in tech sector, but just $425 in everything else (Chart 9 and 10);

yet in 2021 GDP in dollar terms forecast to rise $1.3tn in China, $767bn in EU+UK, versus $612bn in US; global fiscal stimulus the other big 2020 trend...supports rotation from deflation to inflation...and traders note semiconductor stocks are already discounting ISM levels of >60 (Chart 11).

Finally, one look at the price of gold - which just closed at an all time high...

... and it becomes clear that it is now just a matter of time before the financial world as we know it, will end.

"The reason that governments don’t like gold is probably for the same reason that kids don’t like chaperones at the senior prom. Because the chaperones are there to keep the kids in line and prevent them from doing things they really shouldn’t be doing. And that’s really what gold does. It’s kind of like a chaperone for government politicians because it keeps them honest. Because if you have real money, and government wants to spend money on programs, it needs to collect that money in taxes. And that generally puts a brake on a lot of programs because the public doesn’t want to pay.

...

Gold stands in the way, because you can print paper out of thin air. But gold can’t be printed into existence; it needs to be mined. And if we’re on a gold standard, and gold is money, then the government needs real money. And since it doesn’t have the ability to make it, it has to collect it in taxes before it can spend it back into circulation.”

Per a July 22 announcement shared with Cointelegraph, the Office of the Comptroller of the Currency (OCC) is granting permission to federally chartered banks to custody cryptocurrency.

This issue has seen much skepticism, given that crypto wallets do not resemble the custody requirements of other sorts of assets. Nonetheless, in its interpretive letter on the subject, the OCC wrote:

“The OCC recognizes that, as the financial markets become increasingly technological, there will likely be increasing need for banks and other service providers to leverage new technology and innovative ways to provide traditional services on behalf of customers.”

In the words of the announcement, the new opinion “applies to national banks and federal savings associations of all sizes.”

Acting Comptroller of the Currency Brian Brooks similarly saw the development as part of modernizing banking in the U.S., saying “From safe-deposit boxes to virtual vaults, we must ensure banks can meet the financial services needs of their customers today,”

The OCC’s letter further specifies that bank “custody” of crypto assets is dependent on their access to the keys to the crypto wallets rather than any sort of physical requirement — a confirmation of Andreas Antonopoulos’ famous line of “not your keys, not your coins.” the OCC specifies:

“That national banks may escrow encryption keys used in connection with digital certificates because a key escrow service is a functional equivalent to physical safekeeping.”

OCC’s heightened crypto engagement under Brooks

Coming from Coinbase’s legal team, Brian Brook’s tenure as Acting Comptroller has seen accelerated onboarding of crypto capabilities in the U.S. financial system. Speaking with Cointelegraph in early June, Brooks hinted at his interest in expanding the right to custody crypto.

One month ago, shortly after our return to twitter from "permanent" banishment, when so much public attention had suddenly shifted to the retail daytrading platform Robinhood, we explained just how it is that Robinhood was so efficient at moving markets, and it had nothing to do with Robinhood or its small but dedicated army of 10-year-old daytrading fanatics. Instead, it had everything to do with various High Frequency Trading platforms buying up the retail orderflow that Robinhood was so generously packaging and reselling to the highest bidder, effectively giving HFTs a risk-free way of making pennies from every trade, which would then propagate like wildfire across various trading venues, massively accentuating every small move thanks to the momentum-ignition capabilities of HFT algos.

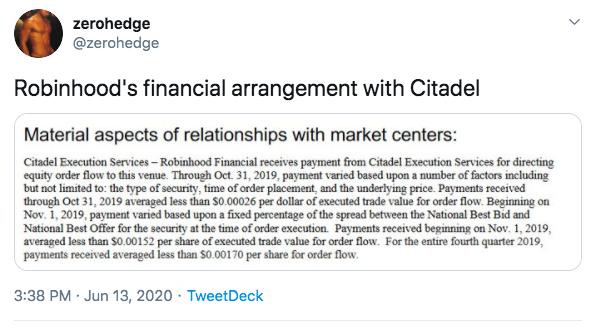

We then also pointed out that Robinhood engages in a practice called payment-for-order-flow...

... for reasons that would become known shortly.

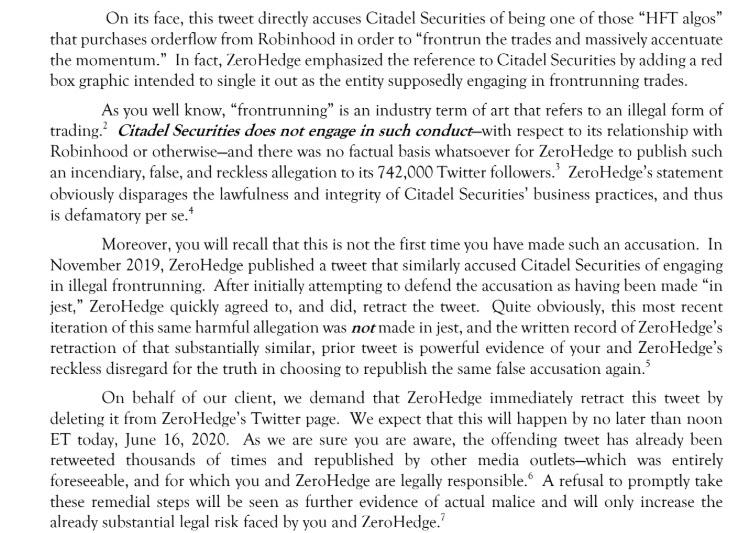

Unfortunately, both of those tweets no longer exist for the simple reason that just days after they were published, we received an angry letter from Citadel's lawyers at Clare Locke threatening to sue us into oblivion if we did not immediately retract and delete said tweets.

Some key phrases of note from the above text:

"Citadel Securites does not engage in such conduct [i.e., frontrunning] and there was no factual basis whatsoever for ZeroHedge to publish such an incendiary, false, and reckless allegation to its 742,000 Twitter followers" [it's 771,000 now].

"ZeroHedge's statement obviously disparages the lawfulness and integrity of Citadel Securities' business pratices."

"Quite obviously, this most recent iteration of this same harmful allegation was not made in jest."

"We demand that ZeroHedge immediately retract this tweet by deleting it from ZeroHedge's Twitter page... A refusal to promptly take down these remedial steps will be seen as further evidence of actual malice and will only increase the already substantial legal risk faced by you and ZeroHedge."

As the letter correctly notes, this was not the first time Citadel Securities (which is majority-owned by Ken Griffin, the billionaire investor, and is the sister firm to Citadel, the hedge fund he runs) threatened legal action against Zero Hedge for accusing the trading giant of frontrunning orders. On November 22, just hours if not minutes after a tweet of a similar nature, we got a similar legal threat from the same law firm. Again, some of the highlights from that particular letter:

"ZeroHedge's statement obviously disparages the lawfulness and integrity of Mr. Griffin and Citadel Securites's business practices, and thus is defamatory per se.[sic]"

"As you well know, "frontrunning" is an unethical and illegal trading practice."

Needless to say, instead of engaging in a legal battle with the world's richest and most powerful trader and his army of lawyers, we decided to simply comply with their demand. That said, dear gentlemen from ClareLocke - we do know very well that frontrunning is an unethical and illegal trading practice. But we wonder: does your client know that?

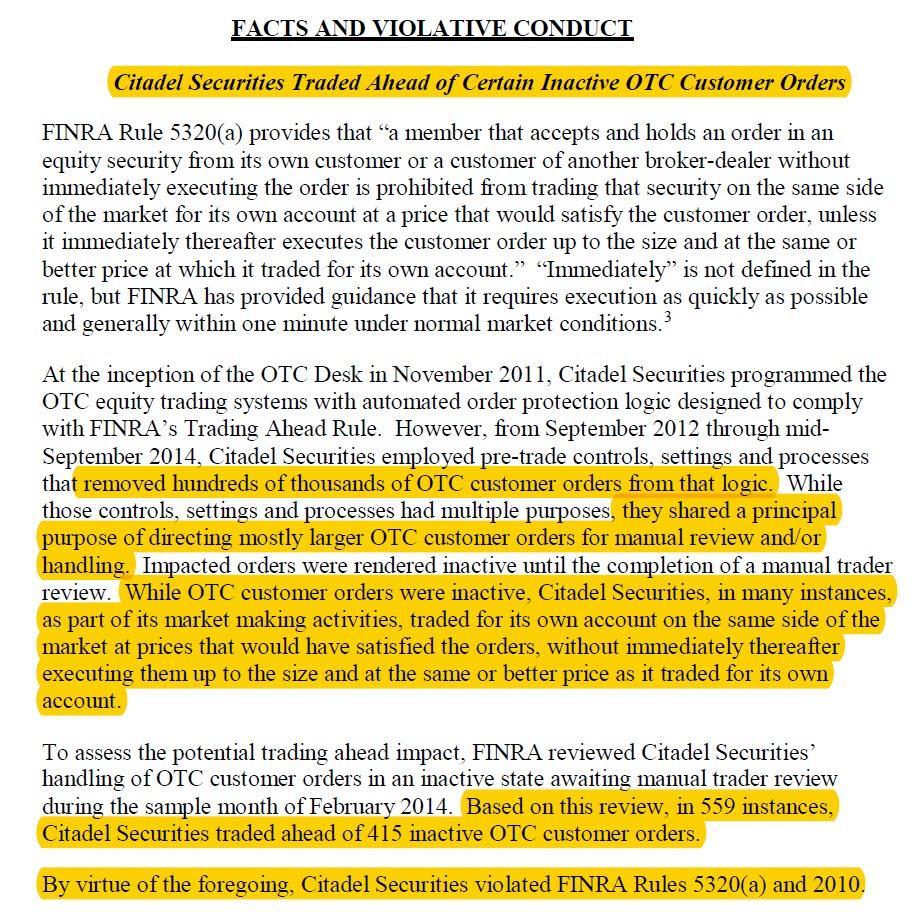

The reason why we ask is very simple. According to a Letter of Acceptance (No. 2014041859401), Waiver and Consent published by financial regulator FINRA, none other than Citadel Securities was censured and fined for engaging in - drumroll - "trading ahead of customer orders."

Now we admit that our financial jargon is a bit rusty these days, but "trading ahead of customer orders" sounds awfully similar to another far more popular world, oh yes, frontrunning!

Jargon aside, some of the other highlighted words we are very familiar with, such as "hundreds of thousands"... and "559 instances" in which Citadel traded ahead of customer orders.

Now, we may be getting a little ahead of ourselves here, but it was Citadel's own lawyers that informed us on more than one occasion that:

"frontrunning" is an unethical and illegal trading practice."

So, what are we to make of this? Could it be that Citadel was engaging in at least 559 instance of what its lawyer called "unethical and illegal trading practice." Surely not: after all the lawyers would surely know very well how ridiculous and laughable their letter and threats would look if it ever emerged that Citadel was indeed frontrunning its customers.

But then we read that Finra censured and fined Citadel $700,000 - or as twitter user @KennethDread puts it 0.70% Basquiats...

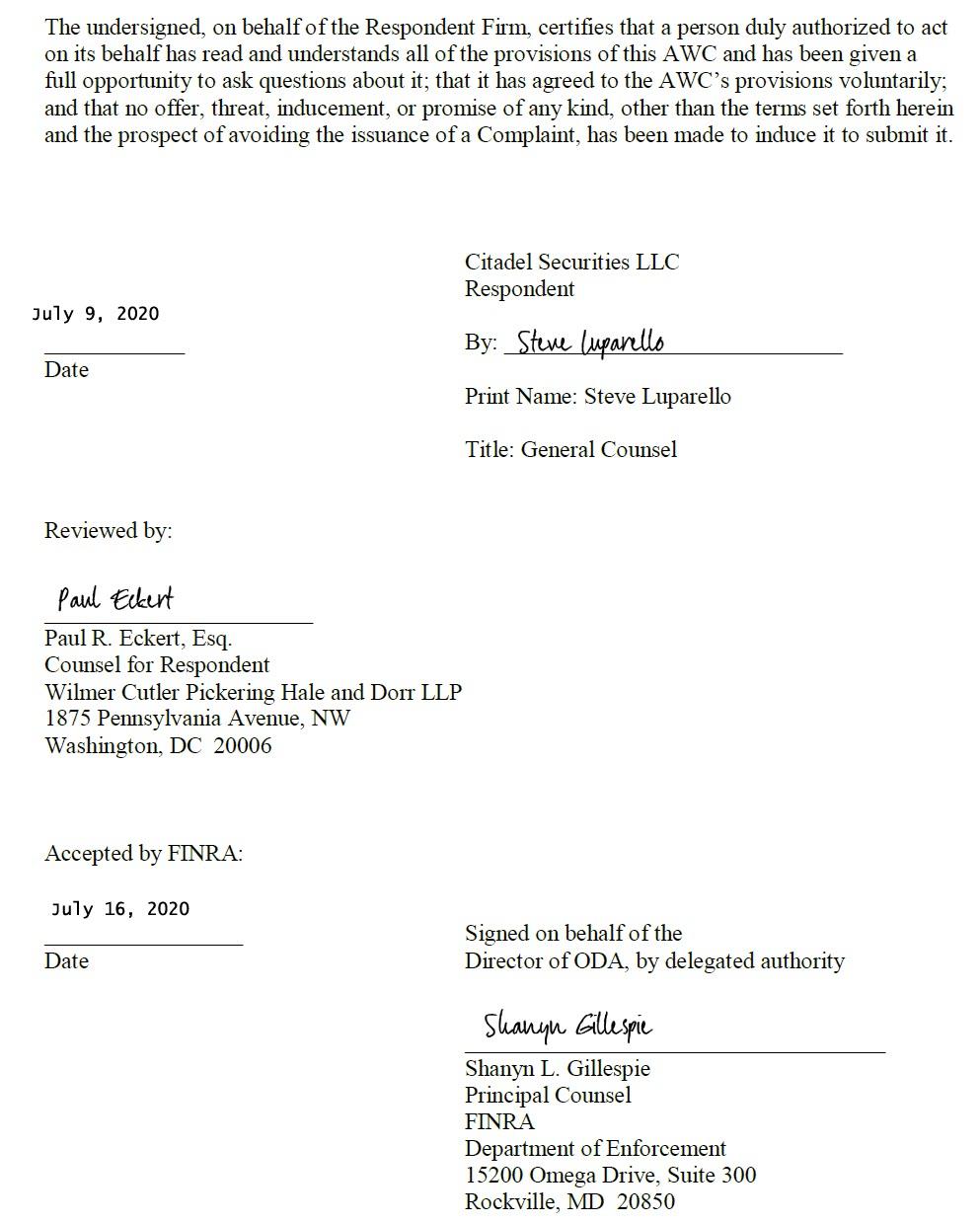

... and it appears that Citadel may indeed have engaged in some of what its own lawyers called "unethical and illegal" trading practice, especially since Citadel Securities' own General Counsel, Steve Luparello signed the Finra AWC:

Well that's... awkward.

And lest someone ignores all of the above - after all it was published in a fringe, tinfoil conspiracy theory website which according to glorious liberal wizards at Wikipedia is somehow both "far right" and "libertarian" at the same time - here is the far more "erudite" Financial Times explaining what happened:

Over a two-year period until September 2014, the market-maker removed hundreds of thousands of large OTC orders from its automated trading processes, according to Finra. That rendered the orders “inactive” and so they had to be handled manually by human traders.

Citadel Securities then “traded for its own account on the same side of the market at prices that would have satisfied the orders,” without immediately filling the inactive orders at the same or better prices as required by Finra rules, the regulator said.

In February 2014, a sample month reviewed by Finra, the market-maker traded ahead in nearly three-quarters of the inactive orders. “Based on this review, in 559 instances, Citadel Securities traded ahead of 415 inactive OTC customer orders,” the regulator said.

Of course, since the action was launched by Finra and not the SEC - probably for a reason - Citadel was allowed to put the whole sordid affair behind it without admitting or denying the claims. Just one glitch: the company was required to make whole any customers affected, not something a market maker does if they legitimately "deny" anything bad actually happened.

The good news is that neither Citadel nor its lawyers can go after us again for merely reporting what Finra already found because on page 11 of the AWC we read the following:

The Firm may not take any action or make or permit to be made any public statement, including in regulatory filings or otherwise, denying, directly or indirectly, any finding in this AWC or create the impression that the AWC is without factual basis.

Which means that going forward, allegations about Citadel frontran its clients - on at least 559 instances no less - are fair game. That said, Citadel did make a statement to the FT:

"We have addressed all of Finra’s concerns and take very seriously our obligations to comply fully with its rules. The issue relates to a limited number of manually handled orders, most of which occurred in 2012-2014."

Which is a succinct way of summarizing precisely what Finra said. Our own request for comments was not returned by the publication time.

But wait, there's more!

Finra also said Citadel Securities fell short of supervisory requirements and failed to display certain OTC customers’ limit orders: instructions to buy or sell at a specific price, or better. As the FT notes, "nearly half of the 467 limit orders reviewed by the regulator in the six years until September 2018 were found to violate Finra’s requirements to display orders. The bulk of the violations were for failing to execute trades against existing quotations in a timely manner, Finra said."

What does the above mean for clients? Well, they are welcome to sue Citadel Securities and get their money back. As Finra writes, "the imposition of a restitution order or any other monetary sanction herein, and the timing of such ordered payments, does not preclude customers from pursuing their own actions to obtain restitution or other remedies."

What does the above mean for Ken Griffin? Well, as noted above, the penalty is about 0.7% of what the CEO recently paid for a Basquiat painting.

It's also clear that the size of the "penalty" will certainly not force Griffin to mortgage one or more of his extensive properties located in New York, London, Chicago, or Palm Beach and countless others cities across the globe:

One thing that is certain is that "trading" clearly pays, even if it means occasionally and purely unaccidentally "removing hundreds of thousands of mostly larger customer orders" from mandatory Trading Ahead and Limit Order Display Rules and customer protections. Surely that happens every day to all of us.

In fact the only confusion we have at this moment is who is more ironically named: Citadel or Robinhood?