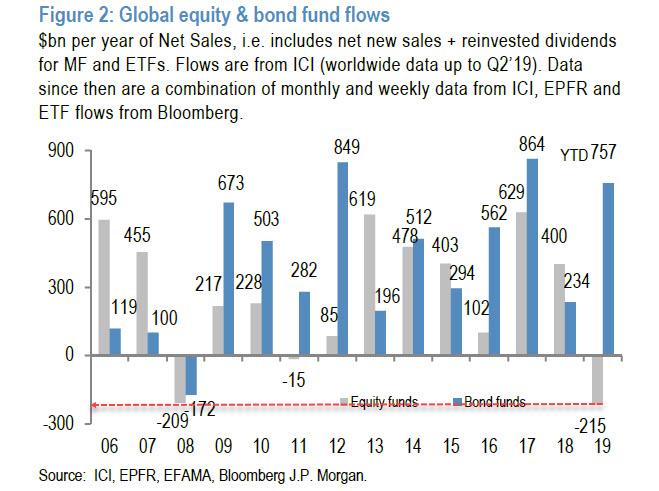

Back in 2019 we posted on several occasions that a "conundrum" had emerged in the stock market: with equities hitting new all time highs, especially in the last quarter after the Fed relaunched QE to bailout a bunch of basis trading hedge funds under the pretext of saving the repo market, equity outflows soared to all time highs...

... as investors fled risk assets realizing that the market was unsustainable high and artificially propped up by the Fed (as a reminder 2019 saw zero earnings growth and all the equity upside was thanks to multiple expansion).

Fast forward to early May when the "conundrum" made a triumphal return, because as BofA reported even as stocks were soaring, investors once again fled into cash, allocating tens of billions to money markets...

... and while investors also rushed to allocate fund to "risk free" bonds, now that the Fed is buying corporate bond ETFs and also debt from such "middle class" stalwarts as Apple and Berkshire, they were once again aggressively selling stock fund ETFs.

In the ensuing two months, the conundrum has persisted even if there was one small change: the funds flowing into money markets have reversed, and according to the latest EPFR fund flows data, the last week of June saw $28.8bn pulled out out of cash, which according to BofA's Michael Hartnett was the largest MMF redemption since Dec 19. That said, even with the latest outflow from money market funds, more than $1.1 trillion in cash has gone into money markets.

Yet what continues to confound professional investors who continue to recommend stocks based on "fundamentals" when the only thing that matters any more is how many trillions the Fed will injects into stocks, is that funds continue to flow into bonds ($15.3bn last week), new money continues to be allocated to gold (42BN in the last week), yet equity funds continue to see relentless outflows, with another $7.1bn pulled out of stocks last week even as stocks appears to be on a relentless upswing.

In fact, a look at fund flows among various asset classes, shows that stocks are the only class that has suffered pretty much constant outflows, while new capital has been allocated to gold, bonds (both IG and HY), and most of all cash.

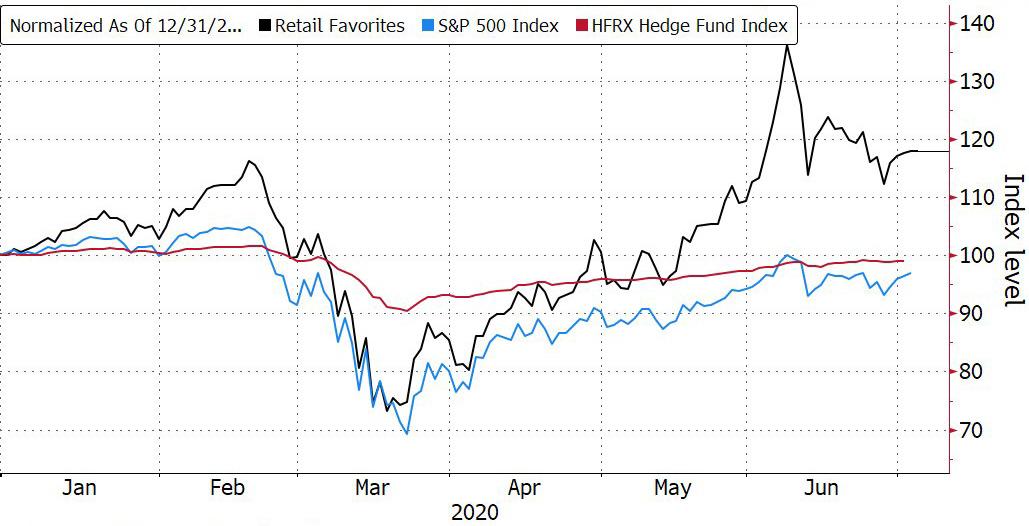

But wait, it's not just the 2019 conundrum that is at play here. Yes, it is true that last year investors were just as aggressively selling equity funds (while the strong buyback bid helped levitate most assets), a situation that has re-emerged in recent weeks, but in 2019 we didn't have the Robin Hood effects, where millions of Gen-Zers and millennials were willingly "investing" their stimulus checks in ultra-high beta stocks and anything that had plunged, even if it was bankrupt companies.

So how is the current situation different? The answer comes courtesy of Goldman's head of hedge fund sales, Tony Pasquariello, who writes that while in total retail investors are dumping stocks, that is not true for all retail investors, where a very clear generational divide has emerged.

Here are his latest observations:

The bifurcation continues within the retail community: an older generation continues to make sales via mutual funds and ETFs (link); a younger generation continue to trade stocks like it’s 1999 (“free trades, jackpot dreams lure small investors to options”).At some point, the $64,000 question is... Where are we in the retail cycle? Having lived through the late 90’s, I tend to think the recent euphoria can persist a bit longer.

In other words, even Goldman now sees the ghost of the dot com bubble re-emerge, as older Americans scramble to liquidate stock by selling to their very own children.

As for Goldman's assessment that the euphoria can persist a "bit" longer, we take the over - with Powell now having gone all in, staking not only the Fed's reputation and the entire capitalist way of life, including the dollar as a global reserve currency on pushing stocks even higher, this may be the one time when retail investors not only outperform hedge funds - and the S&P500 - as they have been for much of 2020...

... but also the baby boomers who can't sell stock fast enough to their own children.

Or then again, maybe this time won't be different